The Trump campaign has made “drill everywhere” one of its main campaign slogans, implying that it will radically weaken environmental and other restrictions on oil drilling. This is supposed to be good for both the economy, since it would in principle mean lower gas and energy prices more generally, but also the oil industry since it won’t have to worry about government regulations in deciding where and how to drill. Increased oil production would be bad news for the environment since it likely means more local contamination, but more importantly, it will increase greenhouse gas emissions which will accelerate global warming.

The bizarre aspect to this story is that somehow lower oil prices is supposed to be a good thing for the oil industry. Predicting oil prices is not an easy thing to do, and as a practical matter the U.S. is already producing oil at record levels, so “drill everywhere” may not mean much additional oil production. But if the campaign’s promise comes true, and oil prices do fall sharply, that is not likely to be good news for the industry.

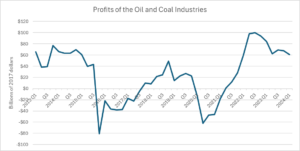

The figure below shows the combined profits for the oil and coal industry (the bulk of this oil) since 2013. The numbers are in 2017 dollars, so they are adjusted for inflation.

Source: NIPA Table 6.16D, Line 25.

As can be seen, profits fell from over $60 billion in 2014 to massive losses in 2016 and 2017. Profits recovered modestly in 2018 and 2019 but were still less than half the levels of 2014. The industry again took large losses with the pandemic shutdowns in 2020. Profits recovered in 2021, soaring to record highs in 2022 following Russia’s invasion of Ukraine. In more recent quarters profits have fallen back to roughly their 2014 levels.

This pattern closely tracks oil prices. Oil was selling for over $100 a barrel at the start of 2014. Prices fell sharply in the second half of the year, bottoming out at $44 a barrel in the middle of 2015. After briefly leveling off, they plunged again at the end of the year, bottoming out at less than $30 a barrel in early 2016. Prices then edged up staying mostly over $60 a barrel until the pandemic hit.

The pandemic shutdowns sent prices to record lows. They then recovered with the economy, before soaring to peaks of more than $120 a barrel following the invasion of Ukraine. Prices have since fallen back to the $70-$80 a barrel range, which is comparable to pre-pandemic prices after adjusting for inflation.

Again, the future path of oil prices is not easy to predict, but there does seem a contradiction between the idea that allowing the industry to drill everywhere will both be a profits bonanza and also mean cheap gas for consumers. If a large increase in U.S. production does send oil prices sharply lower, the oil industry is not likely to be very happy.

The Trump campaign has made “drill everywhere” one of its main campaign slogans, implying that it will radically weaken environmental and other restrictions on oil drilling. This is supposed to be good for both the economy, since it would in principle mean lower gas and energy prices more generally, but also the oil industry since it won’t have to worry about government regulations in deciding where and how to drill. Increased oil production would be bad news for the environment since it likely means more local contamination, but more importantly, it will increase greenhouse gas emissions which will accelerate global warming.

The bizarre aspect to this story is that somehow lower oil prices is supposed to be a good thing for the oil industry. Predicting oil prices is not an easy thing to do, and as a practical matter the U.S. is already producing oil at record levels, so “drill everywhere” may not mean much additional oil production. But if the campaign’s promise comes true, and oil prices do fall sharply, that is not likely to be good news for the industry.

The figure below shows the combined profits for the oil and coal industry (the bulk of this oil) since 2013. The numbers are in 2017 dollars, so they are adjusted for inflation.

Source: NIPA Table 6.16D, Line 25.

As can be seen, profits fell from over $60 billion in 2014 to massive losses in 2016 and 2017. Profits recovered modestly in 2018 and 2019 but were still less than half the levels of 2014. The industry again took large losses with the pandemic shutdowns in 2020. Profits recovered in 2021, soaring to record highs in 2022 following Russia’s invasion of Ukraine. In more recent quarters profits have fallen back to roughly their 2014 levels.

This pattern closely tracks oil prices. Oil was selling for over $100 a barrel at the start of 2014. Prices fell sharply in the second half of the year, bottoming out at $44 a barrel in the middle of 2015. After briefly leveling off, they plunged again at the end of the year, bottoming out at less than $30 a barrel in early 2016. Prices then edged up staying mostly over $60 a barrel until the pandemic hit.

The pandemic shutdowns sent prices to record lows. They then recovered with the economy, before soaring to peaks of more than $120 a barrel following the invasion of Ukraine. Prices have since fallen back to the $70-$80 a barrel range, which is comparable to pre-pandemic prices after adjusting for inflation.

Again, the future path of oil prices is not easy to predict, but there does seem a contradiction between the idea that allowing the industry to drill everywhere will both be a profits bonanza and also mean cheap gas for consumers. If a large increase in U.S. production does send oil prices sharply lower, the oil industry is not likely to be very happy.

Read More Leer más Join the discussion Participa en la discusión

Most of us might consider it good news that companies are being forced to roll back their pandemic price increases. Many major consumer product companies took advantage of the pandemic-induced supply chain crisis to raise their prices in excess of their cost increases to fatten their profit margins. This is what University of Massachusetts economist Isabella Weber identified as “sellers’ inflation.”

Following NPR, the NYT decided it is really bad news for the economy that companies like McDonald’s, which saw its profits rise by more than 30 percent during the pandemic, are being forced to roll back price increases. Unless someone believes that the pandemic rise in profit shares should persist indefinitely, these sorts of price reductions are exactly what we should want to see as the economy normalizes in a post-pandemic era.

The piece is also misleading in pushing other evidence of supposedly hard-pressed consumers. It tells us that, “household debt has swelled.” But its source, the New York Fed, shows that consumer debt rose at just a 2.4 percent annual rate in the second quarter, considerably slower than the 3.6 percent rise in disposable income in the quarter.

Rather than being unusual, this rise in consumer debt is very normal. Consumer debt almost always rises, unless the economy is in a recession.

The article also misleads readers by making a statistical fluke into a crisis. It reports:

“Pandemic-era savings have dwindled. In June, Americans saved just 3.4 percent of their after-tax income, compared with 4.8 percent a year earlier.”

In fact, the drop in the saving rate is easily explained by a statistical quirk. There is a large gap between GDP measured on the output side and GDP measured on the income side. This gap, which in principle should be zero (they are measuring the same thing), expanded to 2.3 percent of GDP in the first quarter, the most recent quarter for which we have data.

It is not clear which side is closer to the mark, but regardless of which side has the larger measurement error, the saving rate will rise. In short, there is no evidence of a real fall in the saving rate.

This should be treated as yet another entry in the “bad economy” series where major media outlets are determined to push stories of a bad economy even when they are not grounded in reality.

Most of us might consider it good news that companies are being forced to roll back their pandemic price increases. Many major consumer product companies took advantage of the pandemic-induced supply chain crisis to raise their prices in excess of their cost increases to fatten their profit margins. This is what University of Massachusetts economist Isabella Weber identified as “sellers’ inflation.”

Following NPR, the NYT decided it is really bad news for the economy that companies like McDonald’s, which saw its profits rise by more than 30 percent during the pandemic, are being forced to roll back price increases. Unless someone believes that the pandemic rise in profit shares should persist indefinitely, these sorts of price reductions are exactly what we should want to see as the economy normalizes in a post-pandemic era.

The piece is also misleading in pushing other evidence of supposedly hard-pressed consumers. It tells us that, “household debt has swelled.” But its source, the New York Fed, shows that consumer debt rose at just a 2.4 percent annual rate in the second quarter, considerably slower than the 3.6 percent rise in disposable income in the quarter.

Rather than being unusual, this rise in consumer debt is very normal. Consumer debt almost always rises, unless the economy is in a recession.

The article also misleads readers by making a statistical fluke into a crisis. It reports:

“Pandemic-era savings have dwindled. In June, Americans saved just 3.4 percent of their after-tax income, compared with 4.8 percent a year earlier.”

In fact, the drop in the saving rate is easily explained by a statistical quirk. There is a large gap between GDP measured on the output side and GDP measured on the income side. This gap, which in principle should be zero (they are measuring the same thing), expanded to 2.3 percent of GDP in the first quarter, the most recent quarter for which we have data.

It is not clear which side is closer to the mark, but regardless of which side has the larger measurement error, the saving rate will rise. In short, there is no evidence of a real fall in the saving rate.

This should be treated as yet another entry in the “bad economy” series where major media outlets are determined to push stories of a bad economy even when they are not grounded in reality.

Read More Leer más Join the discussion Participa en la discusión

CNN’s coverage of the economy under President Biden has been unrelentingly negative, even as we have seen the longest stretch of below 4.0 percent unemployment in more than 70 years, the fastest pace of real wage growth for low-paid workers in decades, the highest measure of job satisfaction ever, and a huge surge in new business openings. Today it pontificated on who should get blamed for an economic slump that has not happened.

It ran a piece headlined “Here’s who to blame — and who not to blame — for the slumping U.S. economy.” On the blame side, it tells us overspending by politicians (no names) is responsible. On the who not to blame side, we’re told it is the Fed, because it has to do clean-up duty.

The division of blame can be questioned. As many of us have argued, the Fed could have started lowering rates earlier this year or even last year and still seen inflation moving towards its 2.0 percent target.

More importantly, we are not currently seeing a slump. The second quarter’s growth was considerably higher than what most economists view as the sustainable pace for the US economy. Early projections for the third quarter show growth coming in strong again, a 2.9 percent rate as of August 7th.

CNN has for some reason chosen to highlight a slump that does not exist. It is of course possible that the US economy could go into recession. The July jobs report was weaker than most of us expected, but the economy still added 114,000 jobs and the employment to population ratio for prime-age workers (ages 25 to 54) hit its highest level in more than two decades. These are not typical features of a recession.

It is a bit strange that a major news outlet is devoting space to allocate blame for a slump that does not yet exist.

CNN’s coverage of the economy under President Biden has been unrelentingly negative, even as we have seen the longest stretch of below 4.0 percent unemployment in more than 70 years, the fastest pace of real wage growth for low-paid workers in decades, the highest measure of job satisfaction ever, and a huge surge in new business openings. Today it pontificated on who should get blamed for an economic slump that has not happened.

It ran a piece headlined “Here’s who to blame — and who not to blame — for the slumping U.S. economy.” On the blame side, it tells us overspending by politicians (no names) is responsible. On the who not to blame side, we’re told it is the Fed, because it has to do clean-up duty.

The division of blame can be questioned. As many of us have argued, the Fed could have started lowering rates earlier this year or even last year and still seen inflation moving towards its 2.0 percent target.

More importantly, we are not currently seeing a slump. The second quarter’s growth was considerably higher than what most economists view as the sustainable pace for the US economy. Early projections for the third quarter show growth coming in strong again, a 2.9 percent rate as of August 7th.

CNN has for some reason chosen to highlight a slump that does not exist. It is of course possible that the US economy could go into recession. The July jobs report was weaker than most of us expected, but the economy still added 114,000 jobs and the employment to population ratio for prime-age workers (ages 25 to 54) hit its highest level in more than two decades. These are not typical features of a recession.

It is a bit strange that a major news outlet is devoting space to allocate blame for a slump that does not yet exist.

Read More Leer más Join the discussion Participa en la discusión

The effort to bring back manufacturing jobs has been a major theme in the 2024 election. Both parties say they consider this a high priority for the next administration. However, there is a notable difference in that the Biden-Harris administration has actively supported an increase in unionization, while the Republicans have indicated, at best, neutrality if not outright hostility towards unions.

This distinction is important in the context of manufacturing jobs. Many people seem to assume that manufacturing jobs are automatically good jobs, paying more than non manufacturing jobs.

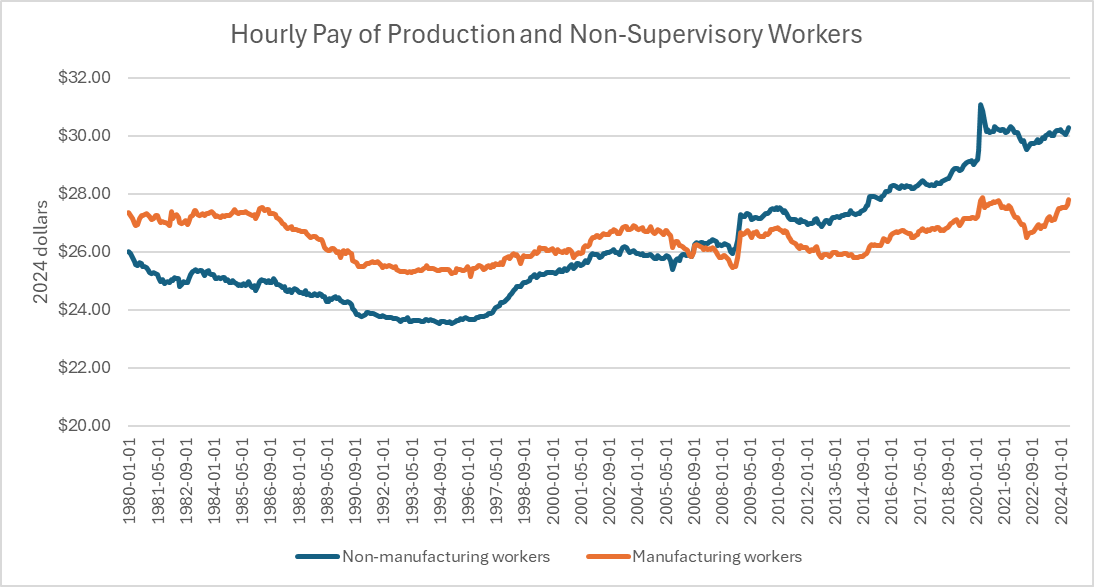

While that was true four decades ago, before the massive job loss of manufacturing jobs due to trade, it is not clear this is still the case. The figure below shows the average hourly pay, in 2024 dollars, for production and non supervisory workers in manufacturing and elsewhere in the private sector.[1]

Source: Bureau of Labor Statistics and author’s calculations.

As can be seen, workers in manufacturing had a substantial edge in pay at the start of this period, earning a premium of more than 5.0 percent over their counterparts in other industries. However, this flipped in 2006, and since then pay for non manufacturing workers has outpaced pay for workers in manufacturing. In the most recent data, non manufacturing workers get almost 9.0 percent more in hourly pay than workers in manufacturing.

To be clear, this is not a comprehensive comparison of relative pay. A full comparison would have to incorporate benefits and also adjust for differences in the workforce, such as education and location. An analysis done by Larry Mishel at the Economic Policy Institute in 2018 found that there was still a substantial premium for manufacturing workers over the years 2010-2016 when controlling for these factors. A more recent analysis from the Federal Reserve Board found that this premium had disappeared altogether, even when controlling for these factors.

While further research may produce different results, there is little doubt that the manufacturing premium has been sharply reduced, if not eliminated altogether, over the last four decades. The main reason for the decline in the premium is not a secret. There has been a huge drop in the percentage of manufacturing workers who are unionized.

In 1980, 32.3 percent of manufacturing workers were union members. This compares to a unionization rate of 15.0 percent for the rest of the private sectors. By comparison, in 2023 just 7.9 percent of manufacturing workers were union members, only slightly higher than the 5.9 percent rate for the private sector as a whole.

The implication of the loss of the wage premium coupled with the decline in unionization rates is that there is little reason to believe that an increase in the number of manufacturing jobs will mean more good jobs unless they are also unionized. It is not the factories that make these jobs good jobs, it is the unions.

[1] The category of production and non supervisory workers includes roughly 80 percent of the workforce. It excludes managers and highly paid professionals, so changes in pay at the top end will not have much impact on these data.

The effort to bring back manufacturing jobs has been a major theme in the 2024 election. Both parties say they consider this a high priority for the next administration. However, there is a notable difference in that the Biden-Harris administration has actively supported an increase in unionization, while the Republicans have indicated, at best, neutrality if not outright hostility towards unions.

This distinction is important in the context of manufacturing jobs. Many people seem to assume that manufacturing jobs are automatically good jobs, paying more than non manufacturing jobs.

While that was true four decades ago, before the massive job loss of manufacturing jobs due to trade, it is not clear this is still the case. The figure below shows the average hourly pay, in 2024 dollars, for production and non supervisory workers in manufacturing and elsewhere in the private sector.[1]

Source: Bureau of Labor Statistics and author’s calculations.

As can be seen, workers in manufacturing had a substantial edge in pay at the start of this period, earning a premium of more than 5.0 percent over their counterparts in other industries. However, this flipped in 2006, and since then pay for non manufacturing workers has outpaced pay for workers in manufacturing. In the most recent data, non manufacturing workers get almost 9.0 percent more in hourly pay than workers in manufacturing.

To be clear, this is not a comprehensive comparison of relative pay. A full comparison would have to incorporate benefits and also adjust for differences in the workforce, such as education and location. An analysis done by Larry Mishel at the Economic Policy Institute in 2018 found that there was still a substantial premium for manufacturing workers over the years 2010-2016 when controlling for these factors. A more recent analysis from the Federal Reserve Board found that this premium had disappeared altogether, even when controlling for these factors.

While further research may produce different results, there is little doubt that the manufacturing premium has been sharply reduced, if not eliminated altogether, over the last four decades. The main reason for the decline in the premium is not a secret. There has been a huge drop in the percentage of manufacturing workers who are unionized.

In 1980, 32.3 percent of manufacturing workers were union members. This compares to a unionization rate of 15.0 percent for the rest of the private sectors. By comparison, in 2023 just 7.9 percent of manufacturing workers were union members, only slightly higher than the 5.9 percent rate for the private sector as a whole.

The implication of the loss of the wage premium coupled with the decline in unionization rates is that there is little reason to believe that an increase in the number of manufacturing jobs will mean more good jobs unless they are also unionized. It is not the factories that make these jobs good jobs, it is the unions.

[1] The category of production and non supervisory workers includes roughly 80 percent of the workforce. It excludes managers and highly paid professionals, so changes in pay at the top end will not have much impact on these data.

Read More Leer más Join the discussion Participa en la discusión

After arguing for over a year that it was time for the Fed to start lowering rates to avoid an economic slowdown, I feel a need to give a bit of pushback against all the folks who are now rushing to agree with me. To be clear, I absolutely think the Fed should lower rates, and the sooner the better (a between meetings reduction would be fine by me), but the talk of an economic collapse and impending recession are more than a bit over the top.

First, let’s catch a breath and look at the actual numbers. The unemployment rate for July was 4.3 percent (4.25 percent going to the next decimal). That is still low by historical standards, but it is up by nearly a percentage point from the 3.4 percent rate hit last April. More importantly, it is up from a rate of 3.7 percent in January. An increase in the unemployment rate of 0.6 percentage points in six months is definitely cause for concern.

But there is reason to believe that weather may have played some role in this increase. While a note from BLS said that there was no clear evidence of a weather effect from Hurricane Beryl in response rates, that doesn’t mean that the hurricane had no effect on the data. Most obviously, 461,000 people reported that they had a job but were unable to work due to the weather. That compares to 83,000 in June and 55,000 in July 2023.

Another 1,089,000 reported they worked fewer hours than normal. That compares to 206,000 in June and 164,000 last July. In a similar vein, the number of people who reported being on temporary layoff increased by 249,000 in July, accounting for more than 70 percent of the reported rise in unemployment. This would support the view that the hurricane played a considerable role in the rise in unemployment in July.

It’s also worth noting that not everything in the household survey for July was not bad. Most importantly, the employment to population ratio (EPOP) for prime-age workers (ages 25 to 54) actually rose 0.1 percentage points in the month to 80.9 percent, tying the peak for the recovery. We don’t usually see EPOPs for this group of workers rising in a recession.

The data from the establishment survey is also mixed rather than uniformly bad. The 114,000 jobs created for the month are low compared to what we have been seeing, but it’s not clear that it is much lower than what we should be expecting. The last economic projections from the Congressional Budget Office before the pandemic showed job growth of just 250,000 a year from 2023 to 2025, as the retirement of the baby boomers was expected to sharply limit job growth.

Even the projections from June of this year show the economy adding just 1.8 million jobs, or 150,000 a month, between the second quarter of this year and the second quarter of 2025. The July figure is obviously somewhat below this number, but the 170,000 average for the last three months is comfortably above it.

These qualifications of the bad news in the July report should not be taken as questioning whether the labor market is weakening. It clearly is, and that is supported by a large amount of other data, such as the drop in the job opening, hiring, and quit rates in the JOLTS data. We also have private data sources such as Indeed and ADP that tell a similar story. And, we know that wage growth has slowed almost back to the pre-pandemic pace in the Average Hourly Earnings series, the Employment Cost Index, and the Indeed Wage Tracker.

A Weaker Labor Market Is Not a Recession

However, it is important to distinguish between saying we see a weaker labor market and we are on the cusp of a recession. The economy is still creating jobs at a respectable pace, even if it may not be rapid enough to keep the unemployment rate from rising. It is especially worth noting that the two most cyclical sectors, construction and manufacturing, are still adding jobs, although very slowly in the latter case. In prior recessions, these sectors began losing jobs before the official start of the recession.

The two sectors together lost 110,000 jobs in the six months prior to the 1990 recession, 237,000 jobs in the six months before the 2001 recession, and 360,000 jobs in the six months leading up to the Great Recession. In the last six months, these sectors have added 133,000 jobs. If we are on the edge of a recession, it clearly is going to look very different from prior recessions.

It is also worth noting that this is not just an issue of correlation. There is a logic whereby job loss in these sectors led to a recession. These sectors tend to pay more than the overall average, both at an hourly rate (this is less true today for manufacturing, as the wage premium has been seriously eroded) and also because these jobs have considerably longer average workweeks.

When there is substantial job loss in these sectors, it translates into less purchasing power in the economy, leading to the sort of cascading effect that gives us recessions. We are clearly not on this path at present.

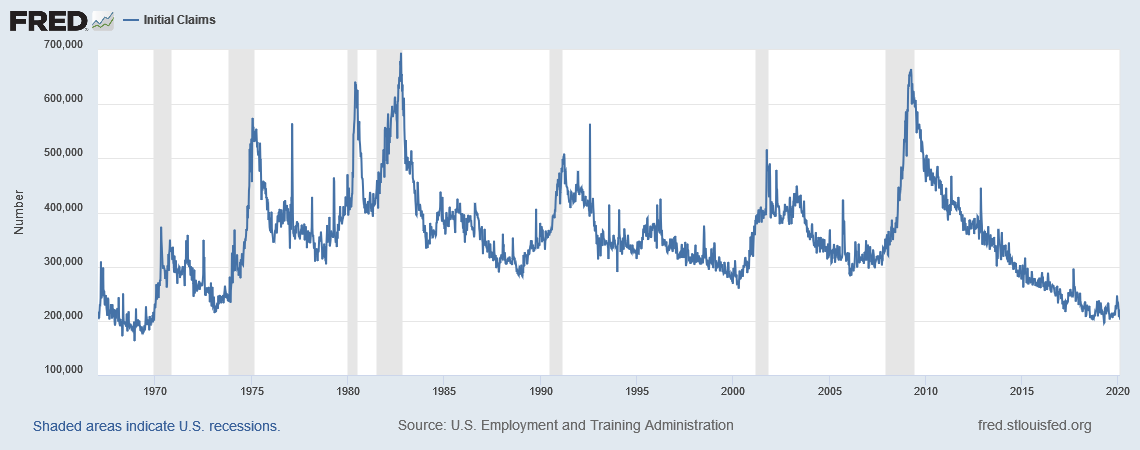

We also can look at weekly filings for unemployment insurance. These always rise sharply before the start of a recession, as shown below. (I have not included the pandemic recession because it would wreck the scale of the graph.)

There has been a modest rise in the number of weekly claims since the lows hit in 2022, but the most recent four-week average of 238,000 is still low by historical levels and even below levels hit last summer. In short, it is hard to look at these data and see an economy on the brink of recession.

The Fed Should Still Lower

As Fed Chair Powell has repeatedly noted, the Fed has a dual mandate for stable prices and full employment. It seems as though the Fed has maintained a single-minded focus on the price stability part of the mandate for the last year, even as inflation has slowed sharply and the labor market has weakened. At this point, it is hard to justify a 5.25 percent federal funds rate.

Expectations of inflation are now slightly above 2.0 percent, which means that the real federal funds rate is over 3.0 percent. That is seriously contractionary. Through most of the period prior to the pandemic, the real rate was close to zero and often negative.

An excessively contractionary policy from the Fed may not push us into recession any time soon, but it could mean hundreds of thousands of people are being denied jobs due to a weak labor market. And millions of people who might otherwise leave jobs for better ones, or push for higher pay at their current job, are being denied this opportunity. And high mortgage rates continue to take a huge toll on the housing market.

We don’t have to start yelling that the sky is falling. None of the data supports that story. But the labor market is clearly weaker than it has to be, and the Fed can help to turn it around with an aggressive set of rate cuts in the second half of this year.

After arguing for over a year that it was time for the Fed to start lowering rates to avoid an economic slowdown, I feel a need to give a bit of pushback against all the folks who are now rushing to agree with me. To be clear, I absolutely think the Fed should lower rates, and the sooner the better (a between meetings reduction would be fine by me), but the talk of an economic collapse and impending recession are more than a bit over the top.

First, let’s catch a breath and look at the actual numbers. The unemployment rate for July was 4.3 percent (4.25 percent going to the next decimal). That is still low by historical standards, but it is up by nearly a percentage point from the 3.4 percent rate hit last April. More importantly, it is up from a rate of 3.7 percent in January. An increase in the unemployment rate of 0.6 percentage points in six months is definitely cause for concern.

But there is reason to believe that weather may have played some role in this increase. While a note from BLS said that there was no clear evidence of a weather effect from Hurricane Beryl in response rates, that doesn’t mean that the hurricane had no effect on the data. Most obviously, 461,000 people reported that they had a job but were unable to work due to the weather. That compares to 83,000 in June and 55,000 in July 2023.

Another 1,089,000 reported they worked fewer hours than normal. That compares to 206,000 in June and 164,000 last July. In a similar vein, the number of people who reported being on temporary layoff increased by 249,000 in July, accounting for more than 70 percent of the reported rise in unemployment. This would support the view that the hurricane played a considerable role in the rise in unemployment in July.

It’s also worth noting that not everything in the household survey for July was not bad. Most importantly, the employment to population ratio (EPOP) for prime-age workers (ages 25 to 54) actually rose 0.1 percentage points in the month to 80.9 percent, tying the peak for the recovery. We don’t usually see EPOPs for this group of workers rising in a recession.

The data from the establishment survey is also mixed rather than uniformly bad. The 114,000 jobs created for the month are low compared to what we have been seeing, but it’s not clear that it is much lower than what we should be expecting. The last economic projections from the Congressional Budget Office before the pandemic showed job growth of just 250,000 a year from 2023 to 2025, as the retirement of the baby boomers was expected to sharply limit job growth.

Even the projections from June of this year show the economy adding just 1.8 million jobs, or 150,000 a month, between the second quarter of this year and the second quarter of 2025. The July figure is obviously somewhat below this number, but the 170,000 average for the last three months is comfortably above it.

These qualifications of the bad news in the July report should not be taken as questioning whether the labor market is weakening. It clearly is, and that is supported by a large amount of other data, such as the drop in the job opening, hiring, and quit rates in the JOLTS data. We also have private data sources such as Indeed and ADP that tell a similar story. And, we know that wage growth has slowed almost back to the pre-pandemic pace in the Average Hourly Earnings series, the Employment Cost Index, and the Indeed Wage Tracker.

A Weaker Labor Market Is Not a Recession

However, it is important to distinguish between saying we see a weaker labor market and we are on the cusp of a recession. The economy is still creating jobs at a respectable pace, even if it may not be rapid enough to keep the unemployment rate from rising. It is especially worth noting that the two most cyclical sectors, construction and manufacturing, are still adding jobs, although very slowly in the latter case. In prior recessions, these sectors began losing jobs before the official start of the recession.

The two sectors together lost 110,000 jobs in the six months prior to the 1990 recession, 237,000 jobs in the six months before the 2001 recession, and 360,000 jobs in the six months leading up to the Great Recession. In the last six months, these sectors have added 133,000 jobs. If we are on the edge of a recession, it clearly is going to look very different from prior recessions.

It is also worth noting that this is not just an issue of correlation. There is a logic whereby job loss in these sectors led to a recession. These sectors tend to pay more than the overall average, both at an hourly rate (this is less true today for manufacturing, as the wage premium has been seriously eroded) and also because these jobs have considerably longer average workweeks.

When there is substantial job loss in these sectors, it translates into less purchasing power in the economy, leading to the sort of cascading effect that gives us recessions. We are clearly not on this path at present.

We also can look at weekly filings for unemployment insurance. These always rise sharply before the start of a recession, as shown below. (I have not included the pandemic recession because it would wreck the scale of the graph.)

There has been a modest rise in the number of weekly claims since the lows hit in 2022, but the most recent four-week average of 238,000 is still low by historical levels and even below levels hit last summer. In short, it is hard to look at these data and see an economy on the brink of recession.

The Fed Should Still Lower

As Fed Chair Powell has repeatedly noted, the Fed has a dual mandate for stable prices and full employment. It seems as though the Fed has maintained a single-minded focus on the price stability part of the mandate for the last year, even as inflation has slowed sharply and the labor market has weakened. At this point, it is hard to justify a 5.25 percent federal funds rate.

Expectations of inflation are now slightly above 2.0 percent, which means that the real federal funds rate is over 3.0 percent. That is seriously contractionary. Through most of the period prior to the pandemic, the real rate was close to zero and often negative.

An excessively contractionary policy from the Fed may not push us into recession any time soon, but it could mean hundreds of thousands of people are being denied jobs due to a weak labor market. And millions of people who might otherwise leave jobs for better ones, or push for higher pay at their current job, are being denied this opportunity. And high mortgage rates continue to take a huge toll on the housing market.

We don’t have to start yelling that the sky is falling. None of the data supports that story. But the labor market is clearly weaker than it has to be, and the Fed can help to turn it around with an aggressive set of rate cuts in the second half of this year.

Read More Leer más Join the discussion Participa en la discusión

The network ran the second piece in three days blaming a weak economy for the fact that restaurants can’t sustain their inflated pandemic profit margins. The basic story here is that many restaurant chains took advantage of the supply chain crisis to increase their profit margins.

To be clear, this means that they raised their prices by more than their costs. This is what University of Massachusetts economist Isabella Weber called “sellers’ inflation.” More commonly it is known as “greedflation.”

We can argue over the exact mechanism, but the basic point is pretty clear in the data. The profit share of national income increased at the expense of wages.

In the case of the restaurant sector, after seeing a big jump in profits during the pandemic, many of the big chains now appear to be losing customers and are feeling pressure to cut prices. Rather than presenting this as a positive development, NPR is presenting it as evidence of a weak economy where consumers can no longer afford to eat out.

Their piece on Thursday presented this as a widespread problem. In addition to McDonald’s, which is discussed in a piece on Monday, it also talked about Starbucks, Dennys, and a number of other chains, all of which are apparently seeing a drop in sales.

As noted in my earlier piece, profits at McDonald’s are up more than 30 percent since the pandemic. Starbucks profits have risen from $18.4 billion in the four quarters ending in the fourth quarter of 2019 to $25.2 billion in the most recent 12 months, a 37 percent increase. Cumulative inflation over this period was just over 20 percent.

These chains would be happy to keep their profit margins, but apparently, the conditions of competition are preventing them from doing so and now they are lowering their prices. Most people would probably view this as a positive story. It means lower prices for consumers or at least lower inflation.

Incredibly, NPR literally never mentioned profit margins in either piece. It presented this news as a bad economy story where people no longer have the money to eat out.

It seems that no matter what the economy does, much of the media is determined to present a bad economy story. That is pretty incredible when we just had the longest stretch of low unemployment in 70 years and real wages are rising at a healthy pace, in spite of the disruptions created by the pandemic and Russia’s invasion of Ukraine.

The network ran the second piece in three days blaming a weak economy for the fact that restaurants can’t sustain their inflated pandemic profit margins. The basic story here is that many restaurant chains took advantage of the supply chain crisis to increase their profit margins.

To be clear, this means that they raised their prices by more than their costs. This is what University of Massachusetts economist Isabella Weber called “sellers’ inflation.” More commonly it is known as “greedflation.”

We can argue over the exact mechanism, but the basic point is pretty clear in the data. The profit share of national income increased at the expense of wages.

In the case of the restaurant sector, after seeing a big jump in profits during the pandemic, many of the big chains now appear to be losing customers and are feeling pressure to cut prices. Rather than presenting this as a positive development, NPR is presenting it as evidence of a weak economy where consumers can no longer afford to eat out.

Their piece on Thursday presented this as a widespread problem. In addition to McDonald’s, which is discussed in a piece on Monday, it also talked about Starbucks, Dennys, and a number of other chains, all of which are apparently seeing a drop in sales.

As noted in my earlier piece, profits at McDonald’s are up more than 30 percent since the pandemic. Starbucks profits have risen from $18.4 billion in the four quarters ending in the fourth quarter of 2019 to $25.2 billion in the most recent 12 months, a 37 percent increase. Cumulative inflation over this period was just over 20 percent.

These chains would be happy to keep their profit margins, but apparently, the conditions of competition are preventing them from doing so and now they are lowering their prices. Most people would probably view this as a positive story. It means lower prices for consumers or at least lower inflation.

Incredibly, NPR literally never mentioned profit margins in either piece. It presented this news as a bad economy story where people no longer have the money to eat out.

It seems that no matter what the economy does, much of the media is determined to present a bad economy story. That is pretty incredible when we just had the longest stretch of low unemployment in 70 years and real wages are rising at a healthy pace, in spite of the disruptions created by the pandemic and Russia’s invasion of Ukraine.

Read More Leer más Join the discussion Participa en la discusión

That’s what Trump would be saying if we had the exact same economy, and every Republican and politician in the country would be repeating some variant of that line. The media would be filled with stories commenting on how the strong economy will make it difficult for the Democrats to win in November.

But that’s not what we’re seeing now. Instead, the media are constantly telling us about the bad economy, even when they have to misrepresent the data in fundamental ways to make their case.

For example, the Washington Post had a piece last week telling us in its subhead that homelessness was at a record high. The focus was that increasingly the homeless are people with jobs. Bloomberg News Service told us things were bad because the number of multiple jobholders hit a record high, although not as a share of employment. That figure hit a peak in 2019, at the top of the pre-pandemic Trump economy. And for its July 4th economy piece the New York Times deliberately found an atypical worker to tell us that people at the bottom have it tough.

Ordinarily, I am happy to see the media highlight the situation of the people who are struggling in this country. We could and should do far better in ensuring that people have the necessities of life. I have also written endlessly on how the rules of the economy have been deliberately rigged to redistribute income from ordinary workers to those at the top.

This rigging is most visible with trade policy where we have quite explicitly had a policy of putting manufacturing workers in direct competition with low-paid workers in the developing world. This had the predicted and actual effect of lowering their pay. Since manufacturing has historically been a source of high-paying jobs for workers without college degrees, this trade policy lowered the relative pay of non college-educated workers more generally.

Contrary to what is widely claimed, this policy was not free trade. We did virtually nothing to reduce the barriers that protect the most highly paid professionals, such as doctors and dentists, from foreign competition. We also used these trade deals to make government-granted patent and copyright monopolies longer and stronger. These monopolies redistribute over $1 trillion a year to people at the top end of the income distribution.

Given this reality, I appreciate it when the media point out that many people are not doing well in the economy. The problem with reporting in recent years is that when we actually have taken huge steps to reverse the rise in inequality over the last half-century. For some reason, the media now seem to be endlessly focused on highlighting the negative, even when it has to turn reality on its head to make its case.

Turning Reality on Its Head

Starting with the Washington Post piece, the homeless situation in this country is a disaster, but this is not a new disaster. While the Post tells us homelessness is at a record high its data only go back to 2007, so we don’t have a long comparison period.

Also, the notion of a record high is a bit dubious. The number of people without housing was reported at 653,100 at the start of 2023. It was 647,000 back in 2007. The US population was roughly 11 percent smaller in 2007, so measured as a share of the population, the homeless were 0.21 percent in 2007. They were 0.19 percent of the population at the start of 2023.

Other aspects of the piece were also misleading. Its focus is a big spike from January 2022 to January 2023. That is a bad story, but it is likely that much of the explanation for this rise was the ending of a number of programs, such as expanded Child Tax Credit, rental assistance, and an eviction moratorium, that were part of the Biden administration’s recovery package. In that case, the culprit wasn’t just bad things happening to people, but the ending of social programs that made their lives better.

It would have been useful to make this point. We can have policies that reduce homelessness if there is the political will to implement them.

The piece correctly notes that the main problem is rising rents. This is true, but it is largely the result of a plunge in construction following the collapse of the housing bubble in 2008, which has persisted to the present. Rents have consistently outpaced overall inflation through this 16-year period, although they seem to be slowing sharply now.

There was a spike in rents during the pandemic, which is not mentioned in this piece, due to a huge increase in people working from home and looking for more space. It might have been useful to include this fact if the point was to explain the underlying problem.

It’s also worth noting that the phenomenon of working people being homeless is not new. The piece presents several instances of workers newly finding themselves without housing, but the Post could have written the same piece in 2019 if it had wanted to since there were plenty of workers who were homeless that year as well.

Multiple Jobholding as Evidence of a Bad Economy

The idea that people holding multiple jobs as evidence of a bad economy is a recurring theme in reporting on the Biden economy. It is truly bizarre, since it can also be evidence that people who want to work more hours now have the opportunity to do so. The fact that the number of multiple jobholders rose in the recovery from the Great Recession and peaked as a share of total employment at the business cycle in 2019, would seem to support that view.

It’s also worth noting that 36 percent of multiple jobholders report that they are working remotely. Since the opportunities for remote work have hugely expanded since the pandemic, many current multiple jobholders are likely taking advantage of opportunities that had not previously existed.

The Washington Post and Marketplace Radio even invented a new category to measure economic misery, the number of people holding two full-time jobs. An important fact undermining this story is that this number also seems to be cyclical, with the share rising with the upturn in the last business cycle. The all-time peak was in 2000 at the peak of the late 1990s boom.

Seeking Out an Atypical Worker to Tell an Independence Day Bad Economy Story

I always thought that the people highlighted in news stories were supposed to be representative of a larger group of people. The New York Times showed me otherwise.

It found a low-wage worker, who it acknowledged was atypical, to highlight in a piece headlined, “America’s divided summer economy is coming to an airport or hotel near you.” To emphasize the Times’ agenda in this article the subhead was “The gulf between higher- and low-income consumers has been widening for years, but it is expected to show up clearly in this travel season.”

The problem with this story is that the reality is the exact opposite. As noted earlier, wages for workers at the bottom end of the wage distribution have been rising faster than for those higher up.

Nonetheless, there will always be many people who do worse than the average for workers at any point in the wage distribution and the NYT found one.

“Lashonda Barber, an airport worker in Charlotte, N.C., is among those feeling the pinch. She will spend her summer on planes, but she won’t be leaving the airport for vacation.

“Ms. Barber, 42, makes $19 per hour, 40 hours per week, driving a trash truck that cleans up after international flights. It is a difficult position: The tarmac is sweltering in the Southern summer sun; the rubbish bags are heavy. And while it’s poised to be a busy summer, Ms. Barber’s job is increasingly failing to pay the bills. Both prices and her home taxes are up notably, but she is making just $1 an hour more than she was when she started the gig five years ago.”

A typical worker at Ms. Barber’s point in the income distribution saw an increase in their nominal wage (before adjusting for inflation) of 30.4 percent over the last five years. This means that if she were a representative low-wage worker she would have seen a pay hike of around $5.40 an hour rather than the $1.00 increase reported in the article.

Incredibly, the piece even acknowledges this fact.

“While that is not the standard experience — overall, wages for lower-income people have grown faster than inflation since at least late 2022 — it is a reminder that behind the averages, some people are falling behind.”

So the NYT deliberately sought out an atypical person so it could tell a bad economy story.

Are There Any Good Economy Stories?

As even Larry Summers now concedes (Summers had been a harsh critic of the Biden administration’s recovery package), the US recovery from the pandemic has been remarkable, far better than any other wealthy country. Given this reality, it seems that there would be many opportunities for the media to highlight people benefitting from the strong recovery.

We saw the unemployment rate for Black workers and Black teens hit an all-time low. While the unemployment rate for both was still higher than for white workers (we haven’t eliminated discrimination) millions of people benefitted from the drop in unemployment. The same applies to Hispanic American workers who saw their unemployment rate tie the previous low.

The relatively rapid wage growth at the lower end of the wage distribution should mean that many people have seen improvements in their living standards. To be clear, someone earning $20 an hour, who had been earning $15 an hour five years ago, is not doing great by any measure, but they have seen a substantial gain in real wages.

We also had a record number of people quit jobs and take new ones in the tight labor market of 2022 and the start of 2023. Presumably many of these workers have found jobs they like better and offer greater opportunities for advancement.

We also had record numbers of new businesses being formed, with a disproportionate share being owned by woman and other underrepresented groups. That story has also been largely absent from reporting on the economy.

The US has a huge economy with almost 160 million workers. It is always possible to find people who are doing poorly. That will be true even in the best of times. It is always possible to find people who are doing well in the worst of times.

When the economic data overwhelmingly suggest a strong economy, where people are mostly doing quite well even as we struggle to overcome the effects of a once-in-a-century pandemic, the media have overwhelmingly chosen to highlight the bad stories. We can argue about motives, but we have seen stories where reality literally had to be turned on its head to tell a bad economy story. That is not good reporting.

That’s what Trump would be saying if we had the exact same economy, and every Republican and politician in the country would be repeating some variant of that line. The media would be filled with stories commenting on how the strong economy will make it difficult for the Democrats to win in November.

But that’s not what we’re seeing now. Instead, the media are constantly telling us about the bad economy, even when they have to misrepresent the data in fundamental ways to make their case.

For example, the Washington Post had a piece last week telling us in its subhead that homelessness was at a record high. The focus was that increasingly the homeless are people with jobs. Bloomberg News Service told us things were bad because the number of multiple jobholders hit a record high, although not as a share of employment. That figure hit a peak in 2019, at the top of the pre-pandemic Trump economy. And for its July 4th economy piece the New York Times deliberately found an atypical worker to tell us that people at the bottom have it tough.

Ordinarily, I am happy to see the media highlight the situation of the people who are struggling in this country. We could and should do far better in ensuring that people have the necessities of life. I have also written endlessly on how the rules of the economy have been deliberately rigged to redistribute income from ordinary workers to those at the top.

This rigging is most visible with trade policy where we have quite explicitly had a policy of putting manufacturing workers in direct competition with low-paid workers in the developing world. This had the predicted and actual effect of lowering their pay. Since manufacturing has historically been a source of high-paying jobs for workers without college degrees, this trade policy lowered the relative pay of non college-educated workers more generally.

Contrary to what is widely claimed, this policy was not free trade. We did virtually nothing to reduce the barriers that protect the most highly paid professionals, such as doctors and dentists, from foreign competition. We also used these trade deals to make government-granted patent and copyright monopolies longer and stronger. These monopolies redistribute over $1 trillion a year to people at the top end of the income distribution.

Given this reality, I appreciate it when the media point out that many people are not doing well in the economy. The problem with reporting in recent years is that when we actually have taken huge steps to reverse the rise in inequality over the last half-century. For some reason, the media now seem to be endlessly focused on highlighting the negative, even when it has to turn reality on its head to make its case.

Turning Reality on Its Head

Starting with the Washington Post piece, the homeless situation in this country is a disaster, but this is not a new disaster. While the Post tells us homelessness is at a record high its data only go back to 2007, so we don’t have a long comparison period.

Also, the notion of a record high is a bit dubious. The number of people without housing was reported at 653,100 at the start of 2023. It was 647,000 back in 2007. The US population was roughly 11 percent smaller in 2007, so measured as a share of the population, the homeless were 0.21 percent in 2007. They were 0.19 percent of the population at the start of 2023.

Other aspects of the piece were also misleading. Its focus is a big spike from January 2022 to January 2023. That is a bad story, but it is likely that much of the explanation for this rise was the ending of a number of programs, such as expanded Child Tax Credit, rental assistance, and an eviction moratorium, that were part of the Biden administration’s recovery package. In that case, the culprit wasn’t just bad things happening to people, but the ending of social programs that made their lives better.

It would have been useful to make this point. We can have policies that reduce homelessness if there is the political will to implement them.

The piece correctly notes that the main problem is rising rents. This is true, but it is largely the result of a plunge in construction following the collapse of the housing bubble in 2008, which has persisted to the present. Rents have consistently outpaced overall inflation through this 16-year period, although they seem to be slowing sharply now.

There was a spike in rents during the pandemic, which is not mentioned in this piece, due to a huge increase in people working from home and looking for more space. It might have been useful to include this fact if the point was to explain the underlying problem.

It’s also worth noting that the phenomenon of working people being homeless is not new. The piece presents several instances of workers newly finding themselves without housing, but the Post could have written the same piece in 2019 if it had wanted to since there were plenty of workers who were homeless that year as well.

Multiple Jobholding as Evidence of a Bad Economy

The idea that people holding multiple jobs as evidence of a bad economy is a recurring theme in reporting on the Biden economy. It is truly bizarre, since it can also be evidence that people who want to work more hours now have the opportunity to do so. The fact that the number of multiple jobholders rose in the recovery from the Great Recession and peaked as a share of total employment at the business cycle in 2019, would seem to support that view.

It’s also worth noting that 36 percent of multiple jobholders report that they are working remotely. Since the opportunities for remote work have hugely expanded since the pandemic, many current multiple jobholders are likely taking advantage of opportunities that had not previously existed.

The Washington Post and Marketplace Radio even invented a new category to measure economic misery, the number of people holding two full-time jobs. An important fact undermining this story is that this number also seems to be cyclical, with the share rising with the upturn in the last business cycle. The all-time peak was in 2000 at the peak of the late 1990s boom.

Seeking Out an Atypical Worker to Tell an Independence Day Bad Economy Story

I always thought that the people highlighted in news stories were supposed to be representative of a larger group of people. The New York Times showed me otherwise.

It found a low-wage worker, who it acknowledged was atypical, to highlight in a piece headlined, “America’s divided summer economy is coming to an airport or hotel near you.” To emphasize the Times’ agenda in this article the subhead was “The gulf between higher- and low-income consumers has been widening for years, but it is expected to show up clearly in this travel season.”

The problem with this story is that the reality is the exact opposite. As noted earlier, wages for workers at the bottom end of the wage distribution have been rising faster than for those higher up.

Nonetheless, there will always be many people who do worse than the average for workers at any point in the wage distribution and the NYT found one.

“Lashonda Barber, an airport worker in Charlotte, N.C., is among those feeling the pinch. She will spend her summer on planes, but she won’t be leaving the airport for vacation.

“Ms. Barber, 42, makes $19 per hour, 40 hours per week, driving a trash truck that cleans up after international flights. It is a difficult position: The tarmac is sweltering in the Southern summer sun; the rubbish bags are heavy. And while it’s poised to be a busy summer, Ms. Barber’s job is increasingly failing to pay the bills. Both prices and her home taxes are up notably, but she is making just $1 an hour more than she was when she started the gig five years ago.”

A typical worker at Ms. Barber’s point in the income distribution saw an increase in their nominal wage (before adjusting for inflation) of 30.4 percent over the last five years. This means that if she were a representative low-wage worker she would have seen a pay hike of around $5.40 an hour rather than the $1.00 increase reported in the article.

Incredibly, the piece even acknowledges this fact.

“While that is not the standard experience — overall, wages for lower-income people have grown faster than inflation since at least late 2022 — it is a reminder that behind the averages, some people are falling behind.”

So the NYT deliberately sought out an atypical person so it could tell a bad economy story.

Are There Any Good Economy Stories?

As even Larry Summers now concedes (Summers had been a harsh critic of the Biden administration’s recovery package), the US recovery from the pandemic has been remarkable, far better than any other wealthy country. Given this reality, it seems that there would be many opportunities for the media to highlight people benefitting from the strong recovery.

We saw the unemployment rate for Black workers and Black teens hit an all-time low. While the unemployment rate for both was still higher than for white workers (we haven’t eliminated discrimination) millions of people benefitted from the drop in unemployment. The same applies to Hispanic American workers who saw their unemployment rate tie the previous low.

The relatively rapid wage growth at the lower end of the wage distribution should mean that many people have seen improvements in their living standards. To be clear, someone earning $20 an hour, who had been earning $15 an hour five years ago, is not doing great by any measure, but they have seen a substantial gain in real wages.

We also had a record number of people quit jobs and take new ones in the tight labor market of 2022 and the start of 2023. Presumably many of these workers have found jobs they like better and offer greater opportunities for advancement.

We also had record numbers of new businesses being formed, with a disproportionate share being owned by woman and other underrepresented groups. That story has also been largely absent from reporting on the economy.

The US has a huge economy with almost 160 million workers. It is always possible to find people who are doing poorly. That will be true even in the best of times. It is always possible to find people who are doing well in the worst of times.

When the economic data overwhelmingly suggest a strong economy, where people are mostly doing quite well even as we struggle to overcome the effects of a once-in-a-century pandemic, the media have overwhelmingly chosen to highlight the bad stories. We can argue about motives, but we have seen stories where reality literally had to be turned on its head to tell a bad economy story. That is not good reporting.

Read More Leer más Join the discussion Participa en la discusión

I am not joking. A piece on All Things Considered carries the headline on NPR’s website “McDonald’s is losing customers to inflation.” The gist of the piece is that the economy is so bad that people can no longer afford to eat at McDonald’s. Now the company is being forced to lower its prices.

Incredibly, the piece never once mentions the company’s profits. They went from $11.18 billion in the year ending in December 2019, before the pandemic, to $14.69 billion in the year ending in March, an increase of more than 31 percent. That compares to an overall inflation rate of 21 percent over this period.

Rather than being a victim of inflation, McDonald’s was a cause of inflation. The company took advantage of the high demand and supply chain shortages to jack up its profit margins. Now, apparently competitive conditions in the fast-food industry are returning to something like their pre-pandemic state, and the company is being forced to accept more normal profit margins.

Instead of reporting this as a positive development for consumers, NPR presents it as yet one more bad economy story. It would be nice if we could get some reporting from the real world instead of having reporters who insist on writing pieces from the “bad economy storybook” even when they have no connection to reality.

I am not joking. A piece on All Things Considered carries the headline on NPR’s website “McDonald’s is losing customers to inflation.” The gist of the piece is that the economy is so bad that people can no longer afford to eat at McDonald’s. Now the company is being forced to lower its prices.

Incredibly, the piece never once mentions the company’s profits. They went from $11.18 billion in the year ending in December 2019, before the pandemic, to $14.69 billion in the year ending in March, an increase of more than 31 percent. That compares to an overall inflation rate of 21 percent over this period.

Rather than being a victim of inflation, McDonald’s was a cause of inflation. The company took advantage of the high demand and supply chain shortages to jack up its profit margins. Now, apparently competitive conditions in the fast-food industry are returning to something like their pre-pandemic state, and the company is being forced to accept more normal profit margins.

Instead of reporting this as a positive development for consumers, NPR presents it as yet one more bad economy story. It would be nice if we could get some reporting from the real world instead of having reporters who insist on writing pieces from the “bad economy storybook” even when they have no connection to reality.

Read More Leer más Join the discussion Participa en la discusión

Economists go on endless diatribes against tariffs and quotas as costly policies that raise prices to consumers and slow economic growth. There is considerable truth to this story, even if economists and politicians often exaggerate their case to push favored policies. While virtually all economists will go to their graves touting the evils of protectionism they almost all ignore the most costly forms of protectionism: government-granted patent and copyright monopolies.

Most tariffs raise the price of the protected items by somewhere in the range of 10–25 percent. By contrast, patent and copyright monopolies often raise the price of protected items by 1000 percent or even 10,000 percent. Many high-priced drugs that enjoy patent monopolies or related protections can sell for tens of thousands of dollars. Their generic versions might sell for $30 or $40 a prescription.

There is a similar story for copyrights. Items that could be transferred at near zero cost over the Internet can instead sell for hundreds or even thousands of dollars. This is most evident with costly software, but also true for recorded music and video material, video games, and a variety of other material subject to copyright protections.

There is a clear rationale for patent and copyright monopolies, these monopolies provide an incentive for innovation and creative work. But every type of protectionism has a rationale. Having a rationale doesn’t prevent a trade tariff or quota from being a protectionist policy.

The point here is that these government-granted monopolies are huge interventions in the market. They are arguably justified, but it is close to nuts just to assert they are the free market. (Alternative mechanisms are discussed here and in chapter 5 of Rigged [it’s free]).

It is understandable that people on the right, who generally support policies that redistribute income upward, would try to hide patent and copyright monopolies as just the natural working of the market. It is absolutely mindboggling that many on the left also perpetuate this blatant misrepresentation of reality.

Anyhow, let’s get the playing field set. Granting these monopolies is a choice by governments, they can set different policies. In the case of Artificial Intelligence (AI), the New York Times reports that it seems as though China is rapidly catching up, and possibly even taking the lead, by pursuing open-source policies rather than relying on patents, copyrights, and related protection.

The idea of open-source with reference to AI is that all the coding is freely available to anyone to review and build upon. Understandably, this could be a more effective way to advance the technology since breakthroughs could quickly be built upon by others working in the same area. Also, researchers could learn from failures as well and avoid pursuing similar dead-ends. (This would be a great approach to drug or vaccine development.)

The other obvious development is that the finished product is very cheap. The developer may seek to recover costs by charging servicing fees and/or relying on direct government support. Either way, end users will not be prevented from being able to take advantage of a useful product by its high price.

Anyhow, given all the hype in the business world around AI it would certainly be ironic if Chinese firms surged past their leading U.S. competitors because they relied on an open-source process whereas our firms relied on old-fashioned protectionism. Who knows, maybe even the “free trader” economists would notice one day.

Economists go on endless diatribes against tariffs and quotas as costly policies that raise prices to consumers and slow economic growth. There is considerable truth to this story, even if economists and politicians often exaggerate their case to push favored policies. While virtually all economists will go to their graves touting the evils of protectionism they almost all ignore the most costly forms of protectionism: government-granted patent and copyright monopolies.

Most tariffs raise the price of the protected items by somewhere in the range of 10–25 percent. By contrast, patent and copyright monopolies often raise the price of protected items by 1000 percent or even 10,000 percent. Many high-priced drugs that enjoy patent monopolies or related protections can sell for tens of thousands of dollars. Their generic versions might sell for $30 or $40 a prescription.

There is a similar story for copyrights. Items that could be transferred at near zero cost over the Internet can instead sell for hundreds or even thousands of dollars. This is most evident with costly software, but also true for recorded music and video material, video games, and a variety of other material subject to copyright protections.

There is a clear rationale for patent and copyright monopolies, these monopolies provide an incentive for innovation and creative work. But every type of protectionism has a rationale. Having a rationale doesn’t prevent a trade tariff or quota from being a protectionist policy.

The point here is that these government-granted monopolies are huge interventions in the market. They are arguably justified, but it is close to nuts just to assert they are the free market. (Alternative mechanisms are discussed here and in chapter 5 of Rigged [it’s free]).

It is understandable that people on the right, who generally support policies that redistribute income upward, would try to hide patent and copyright monopolies as just the natural working of the market. It is absolutely mindboggling that many on the left also perpetuate this blatant misrepresentation of reality.

Anyhow, let’s get the playing field set. Granting these monopolies is a choice by governments, they can set different policies. In the case of Artificial Intelligence (AI), the New York Times reports that it seems as though China is rapidly catching up, and possibly even taking the lead, by pursuing open-source policies rather than relying on patents, copyrights, and related protection.

The idea of open-source with reference to AI is that all the coding is freely available to anyone to review and build upon. Understandably, this could be a more effective way to advance the technology since breakthroughs could quickly be built upon by others working in the same area. Also, researchers could learn from failures as well and avoid pursuing similar dead-ends. (This would be a great approach to drug or vaccine development.)

The other obvious development is that the finished product is very cheap. The developer may seek to recover costs by charging servicing fees and/or relying on direct government support. Either way, end users will not be prevented from being able to take advantage of a useful product by its high price.

Anyhow, given all the hype in the business world around AI it would certainly be ironic if Chinese firms surged past their leading U.S. competitors because they relied on an open-source process whereas our firms relied on old-fashioned protectionism. Who knows, maybe even the “free trader” economists would notice one day.

Read More Leer más Join the discussion Participa en la discusión

Seriously, they probably don’t want readers to walk away with that impression, but that is the implication of the piece they did complaining about people working multiple jobs. The piece told readers:

“A record number of Americans worked more than one job last year, and multiple-job holders as a percentage of the total workforce recently matched the highest share since 2019. That was largely driven by women, who worked multiple jobs at the highest rate since the 1990s in December.”

Multiple job holding is not necessarily a sign of a bad labor market. The share of multiple jobholders peaked before the pandemic in 2019 when the recovery was at its peak. Furthermore, as the article itself notes, people might hold multiple jobs because of increased opportunities, not economic hardship.

For example, 36 percent of multiple job holders report that they do telework. The opportunity to do telework was much more limited before the pandemic. Likely, many of these multiple job holders would not be working at multiple jobs if they didn’t have the opportunity to work from home.

The piece does find people who report experiencing economic hardship, but in an economy with 160 million workers, there will also be millions experiencing economic hardship. For some reason, Bloomberg has chosen to seek out these people out and highlight their situations.

By contrast, millions of people work in hotels and restaurants. Their average hourly wage has risen by almost 31 percent since the start of the pandemic in 2020, far above the 21 percent increase in prices over this period. Surely many of these people are doing considerably better now than in 2020.

For some reason, Bloomberg and most of the rest of the media have decided to ignore these and other moderate-income workers who have seen their situation substantially improve as a result of the strong labor market of the last two and half years.

Seriously, they probably don’t want readers to walk away with that impression, but that is the implication of the piece they did complaining about people working multiple jobs. The piece told readers:

“A record number of Americans worked more than one job last year, and multiple-job holders as a percentage of the total workforce recently matched the highest share since 2019. That was largely driven by women, who worked multiple jobs at the highest rate since the 1990s in December.”

Multiple job holding is not necessarily a sign of a bad labor market. The share of multiple jobholders peaked before the pandemic in 2019 when the recovery was at its peak. Furthermore, as the article itself notes, people might hold multiple jobs because of increased opportunities, not economic hardship.

For example, 36 percent of multiple job holders report that they do telework. The opportunity to do telework was much more limited before the pandemic. Likely, many of these multiple job holders would not be working at multiple jobs if they didn’t have the opportunity to work from home.

The piece does find people who report experiencing economic hardship, but in an economy with 160 million workers, there will also be millions experiencing economic hardship. For some reason, Bloomberg has chosen to seek out these people out and highlight their situations.

By contrast, millions of people work in hotels and restaurants. Their average hourly wage has risen by almost 31 percent since the start of the pandemic in 2020, far above the 21 percent increase in prices over this period. Surely many of these people are doing considerably better now than in 2020.

For some reason, Bloomberg and most of the rest of the media have decided to ignore these and other moderate-income workers who have seen their situation substantially improve as a result of the strong labor market of the last two and half years.

Read More Leer más Join the discussion Participa en la discusión