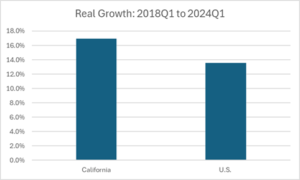

Donald Trump seems very confused about the state of California’s economic health. He gave a press conference Friday in which he implied that California’s economy was collapsing.

This is not true. California has a considerably higher per capita income than the rest of the country. It’s currently ranked 5th. Its economy is also growing considerably more rapidly than the rest of the country.

Since the first quarter of 2018, its economy grew 17.0 percent compared to 13.5 percent for the country as a whole.

Source: Bureau of Economic Analysis.

In fact, this comparison understates the gap somewhat. California accounts for more than 10 percent of the U.S. economy, which means that the U.S. economy outside of California grew by just a bit more than 13.0 percent over this period.

Of course, growth is not the only thing, but it is an important metric. And by most other measures, California is doing better than the average state in the country. It does have a serious shortage of housing due largely to zoning issues. Its Democratic governor is trying to address this problem and Vice-President Harris has as well, during her presidency. It doesn’t seem as though Donald Trump has noticed.

I guess it is unreasonable to expect a reality TV show star like Donald Trump to know about economics.

Donald Trump seems very confused about the state of California’s economic health. He gave a press conference Friday in which he implied that California’s economy was collapsing.

This is not true. California has a considerably higher per capita income than the rest of the country. It’s currently ranked 5th. Its economy is also growing considerably more rapidly than the rest of the country.

Since the first quarter of 2018, its economy grew 17.0 percent compared to 13.5 percent for the country as a whole.

Source: Bureau of Economic Analysis.

In fact, this comparison understates the gap somewhat. California accounts for more than 10 percent of the U.S. economy, which means that the U.S. economy outside of California grew by just a bit more than 13.0 percent over this period.

Of course, growth is not the only thing, but it is an important metric. And by most other measures, California is doing better than the average state in the country. It does have a serious shortage of housing due largely to zoning issues. Its Democratic governor is trying to address this problem and Vice-President Harris has as well, during her presidency. It doesn’t seem as though Donald Trump has noticed.

I guess it is unreasonable to expect a reality TV show star like Donald Trump to know about economics.

Read More Leer más Join the discussion Participa en la discusión

The New York Times had a piece noting that, while we don’t see evidence of an increase in layoffs, we have seen a downturn in hiring which has been associated with a 0.8 percentage point rise in the unemployment rate since April of last year. The piece notes that the monthly rate of job creation has slowed to just 115,000 in the last three months, down from 451,000 in the same months two years ago.

It is worth noting that we are hitting the peak retirement years for the baby boom cohort. The youngest turn 60 this year, while the oldest are 78. In 2020, before the pandemic, the Congressional Budget Office (CBO) projected we would be creating just 20,000 jobs a month in 2024.

As a result of larger than expected immigration, we have been creating far more jobs than had been projected. With immigration now having slowed sharply, it is not clear how many jobs need to be created monthly to prevent the unemployment rate from rising. It is not clear that the June to August pace is too slow.

The New York Times had a piece noting that, while we don’t see evidence of an increase in layoffs, we have seen a downturn in hiring which has been associated with a 0.8 percentage point rise in the unemployment rate since April of last year. The piece notes that the monthly rate of job creation has slowed to just 115,000 in the last three months, down from 451,000 in the same months two years ago.

It is worth noting that we are hitting the peak retirement years for the baby boom cohort. The youngest turn 60 this year, while the oldest are 78. In 2020, before the pandemic, the Congressional Budget Office (CBO) projected we would be creating just 20,000 jobs a month in 2024.

As a result of larger than expected immigration, we have been creating far more jobs than had been projected. With immigration now having slowed sharply, it is not clear how many jobs need to be created monthly to prevent the unemployment rate from rising. It is not clear that the June to August pace is too slow.

Read More Leer más Join the discussion Participa en la discusión

In 1980 Ronald Reagan brought the term “misery index” into political debates. The concept is simple, it’s the sum of the unemployment rate and inflation rate over the last year. It’s not obvious that these two numbers should have the same importance, and they certainly are not the only measures that matter in evaluating the economy, but they do provide an interesting snapshot.

Anyhow, Reagan could point to a misery index that was over 20 percent as the election approached. The inflation rate was in the double-digits and unemployment was still high as a result of a steep but short recession in the spring. The high level for the misery index was a theme Reagan hit on repeatedly in the campaign.

The misery index has largely faded from use over the last four decades, but it is still interesting to see what this simple snapshot shows. Here’s the picture since 1960.

Source: Bureau of Labor Statistics and author’s calculations.

As can be seen, the index for 2024 is near the low point for this sixty-four-year period. (I used the data through August for both inflation and unemployment.) At 6.8 percent, it is 0.2 percentage points higher than it was in 2016 and 0.5 percentage points higher than in 1964, the low point for the period.[1]

In fact, there is a decent chance that it will end up being lower than the 2016 measure by election day. Inflation is clearly headed lower, driven by slower rental inflation and also a recent drop in gas prices. It is likely that the CPI will show a year-over-year inflation rate that is at least 0.2 percentage points lower than the 2.6 percent rate reported through August. If the unemployment rate doesn’t rise, this would leave us tied with the 2016 measure for the second-lowest misery index during this period.

At least by the Reagan index measure, the Biden-Harris economy looks pretty good.

[1] I have used October as the reference month, even though the unemployment data sometimes would not be available by election day and the CPI never would be. The logic is that voters actually experience October unemployment and inflation by election day, even if they haven’t seen the report on these measures from the Bureau of Labor Statistics.

In 1980 Ronald Reagan brought the term “misery index” into political debates. The concept is simple, it’s the sum of the unemployment rate and inflation rate over the last year. It’s not obvious that these two numbers should have the same importance, and they certainly are not the only measures that matter in evaluating the economy, but they do provide an interesting snapshot.

Anyhow, Reagan could point to a misery index that was over 20 percent as the election approached. The inflation rate was in the double-digits and unemployment was still high as a result of a steep but short recession in the spring. The high level for the misery index was a theme Reagan hit on repeatedly in the campaign.

The misery index has largely faded from use over the last four decades, but it is still interesting to see what this simple snapshot shows. Here’s the picture since 1960.

Source: Bureau of Labor Statistics and author’s calculations.

As can be seen, the index for 2024 is near the low point for this sixty-four-year period. (I used the data through August for both inflation and unemployment.) At 6.8 percent, it is 0.2 percentage points higher than it was in 2016 and 0.5 percentage points higher than in 1964, the low point for the period.[1]

In fact, there is a decent chance that it will end up being lower than the 2016 measure by election day. Inflation is clearly headed lower, driven by slower rental inflation and also a recent drop in gas prices. It is likely that the CPI will show a year-over-year inflation rate that is at least 0.2 percentage points lower than the 2.6 percent rate reported through August. If the unemployment rate doesn’t rise, this would leave us tied with the 2016 measure for the second-lowest misery index during this period.

At least by the Reagan index measure, the Biden-Harris economy looks pretty good.

[1] I have used October as the reference month, even though the unemployment data sometimes would not be available by election day and the CPI never would be. The logic is that voters actually experience October unemployment and inflation by election day, even if they haven’t seen the report on these measures from the Bureau of Labor Statistics.

Read More Leer más Join the discussion Participa en la discusión

The New York Times ran a column, by Duke University law professor Jedidiah Briton-Purdy, telling Vice-President Harris how she can turn around her deficit in public opinion polling on the economy. The gist of the piece is that most people are hurting now, but Harris can turn things around by adopting a more populist agenda.

It would be great to see Harris push a more populist agenda. I have written extensively on how the economy has been rigged to redistribute income upward, so I totally support Harris pushing more progressive policies. However, the extent to which anyone will hear a progressive message is open to question. The most fundamental problem is that people now believe a story about the economy that is almost completely at odds with reality.

Contrary to what Briton-Purdy tells us, most people are not hurting now, or at least not more than they did in the past, like before the pandemic when Donald Trump was president. Back then most people said the economy was good.

Somehow, when all the data tell us that most people are doing better off, especially those in the lower end of the income distribution, we have a continual drumbeat in the media about the economy being awful. And it is not just data on wages and prices, we see people behaving as though they are doing pretty well.

For example, air travel was at record highs this summer. At its peak, boardings were close to 3 million a day. That is not the one percent. We have a similar story with car travel, which also hit record highs this summer, with 70 million people hitting the road on the holidays, also not the one percent.

Purchases of restaurant meals are up by 10.5 percent compared with the pre-pandemic rate, after adjusting for inflation. Purchases of meals at fast-food restaurants, also adjusted for inflation, are up by 19.4 percent. Inflation-adjusted spending at sporting events is up by 12.2 percent.

This list can be extended at considerable length, but the point is that people are not acting as though they are suffering. We do have tens of millions of people struggling to get by, and many of them are not getting by, but that was true in 2019 when the prevailing story was the great economy.

When we have a prevailing economic story that is literally 180 degrees at odds with the economic reality, it is worth asking how we can envision Vice-President Harris getting her economic message out to the electorate, if she were to push the themes advocated by Briton-Purdy. The media have bent or even invented data to tell a bad economy story throughout the Biden-Harris administration.

Since the media have used their power to convince the public of a bad economy story that is 180 degrees at odds with reality, what chance will Harris have of getting out her message on the economy in a coherent way? That seems pretty unlikely in the seven weeks left until the election unless we envision that the media will completely change their policies on covering the Democrats.

To be clear, I don’t know what Harris can best say in the current media environment, but any discussion that does not recognize that Harris’s message will not be directly transmitted to the voters is unrealistic. Instead, it will be mediated by news organizations that have been insistent on painting a negative picture of the economy regardless of the facts.

I wish the Democrats had spent more time combatting the misinformation about the economy that major media outlets spewed endlessly for the last three and a half years, but it’s kind of late now. Harris can put worthwhile proposals on the table, which she already has, and hope that they reach the public. But her best hope is that a majority of voters will be unwilling to put a lying, corrupt, incompetent, buffoon back in the White House. I guess we’ll see.

The New York Times ran a column, by Duke University law professor Jedidiah Briton-Purdy, telling Vice-President Harris how she can turn around her deficit in public opinion polling on the economy. The gist of the piece is that most people are hurting now, but Harris can turn things around by adopting a more populist agenda.

It would be great to see Harris push a more populist agenda. I have written extensively on how the economy has been rigged to redistribute income upward, so I totally support Harris pushing more progressive policies. However, the extent to which anyone will hear a progressive message is open to question. The most fundamental problem is that people now believe a story about the economy that is almost completely at odds with reality.

Contrary to what Briton-Purdy tells us, most people are not hurting now, or at least not more than they did in the past, like before the pandemic when Donald Trump was president. Back then most people said the economy was good.

Somehow, when all the data tell us that most people are doing better off, especially those in the lower end of the income distribution, we have a continual drumbeat in the media about the economy being awful. And it is not just data on wages and prices, we see people behaving as though they are doing pretty well.

For example, air travel was at record highs this summer. At its peak, boardings were close to 3 million a day. That is not the one percent. We have a similar story with car travel, which also hit record highs this summer, with 70 million people hitting the road on the holidays, also not the one percent.

Purchases of restaurant meals are up by 10.5 percent compared with the pre-pandemic rate, after adjusting for inflation. Purchases of meals at fast-food restaurants, also adjusted for inflation, are up by 19.4 percent. Inflation-adjusted spending at sporting events is up by 12.2 percent.

This list can be extended at considerable length, but the point is that people are not acting as though they are suffering. We do have tens of millions of people struggling to get by, and many of them are not getting by, but that was true in 2019 when the prevailing story was the great economy.

When we have a prevailing economic story that is literally 180 degrees at odds with the economic reality, it is worth asking how we can envision Vice-President Harris getting her economic message out to the electorate, if she were to push the themes advocated by Briton-Purdy. The media have bent or even invented data to tell a bad economy story throughout the Biden-Harris administration.

Since the media have used their power to convince the public of a bad economy story that is 180 degrees at odds with reality, what chance will Harris have of getting out her message on the economy in a coherent way? That seems pretty unlikely in the seven weeks left until the election unless we envision that the media will completely change their policies on covering the Democrats.

To be clear, I don’t know what Harris can best say in the current media environment, but any discussion that does not recognize that Harris’s message will not be directly transmitted to the voters is unrealistic. Instead, it will be mediated by news organizations that have been insistent on painting a negative picture of the economy regardless of the facts.

I wish the Democrats had spent more time combatting the misinformation about the economy that major media outlets spewed endlessly for the last three and a half years, but it’s kind of late now. Harris can put worthwhile proposals on the table, which she already has, and hope that they reach the public. But her best hope is that a majority of voters will be unwilling to put a lying, corrupt, incompetent, buffoon back in the White House. I guess we’ll see.

Read More Leer más Join the discussion Participa en la discusión

The Census released new data on median household income today showing a large jump, after adjusting for inflation. The Washington Post wrote about the reported rise, but told readers:

“After inflation, median household income rose to $80,610 last year, up from $77,540 in 2022 but less than the $81,210 families brought home in 2019.”

The problem is with the comparison to 2019, the last year before the pandemic. There was a large problem of non-response to the survey for 2019, which was fielded in the middle of the pandemic shutdown in the spring of 2020. The Census Bureau wrote about this problem when it released the 2019 data in the fall of 2020.

Their analysis found that when correcting for non-response bias, income was 2.8 percent lower than the number reported. If we adjust the reported number for 2019 for this bias, it would put median income for 2019 at $78,936, almost $1,700, or 2.0 percent, below the level reported for 2023.

In other words, the Post’s failure to accurately report on 2019 income numbers by adjusting for a well-known error in the data, led the paper to tell people the economy is worse under Biden than Trump by this measure, when the reality is the opposite. Income is higher, in spite of the impact of the pandemic in 2023 than in 2019.

Addendum

It has been pointed out to me that there continues to be an issue of non-response bias in the years since the pandemic, which is likely still leading to an overstatement of income of around 1.5 percent. As a result, while the gap between Census reported and adjusted income was unusually large for the 2019 year, it is still substantial for the 2023 gap. The larger gap in 2019 likely means that the adjusted income for 2023 is higher than it was for 2019, but not by as much as I indicated above.

The Census released new data on median household income today showing a large jump, after adjusting for inflation. The Washington Post wrote about the reported rise, but told readers:

“After inflation, median household income rose to $80,610 last year, up from $77,540 in 2022 but less than the $81,210 families brought home in 2019.”

The problem is with the comparison to 2019, the last year before the pandemic. There was a large problem of non-response to the survey for 2019, which was fielded in the middle of the pandemic shutdown in the spring of 2020. The Census Bureau wrote about this problem when it released the 2019 data in the fall of 2020.

Their analysis found that when correcting for non-response bias, income was 2.8 percent lower than the number reported. If we adjust the reported number for 2019 for this bias, it would put median income for 2019 at $78,936, almost $1,700, or 2.0 percent, below the level reported for 2023.

In other words, the Post’s failure to accurately report on 2019 income numbers by adjusting for a well-known error in the data, led the paper to tell people the economy is worse under Biden than Trump by this measure, when the reality is the opposite. Income is higher, in spite of the impact of the pandemic in 2023 than in 2019.

Addendum

It has been pointed out to me that there continues to be an issue of non-response bias in the years since the pandemic, which is likely still leading to an overstatement of income of around 1.5 percent. As a result, while the gap between Census reported and adjusted income was unusually large for the 2019 year, it is still substantial for the 2023 gap. The larger gap in 2019 likely means that the adjusted income for 2023 is higher than it was for 2019, but not by as much as I indicated above.

Read More Leer más Join the discussion Participa en la discusión

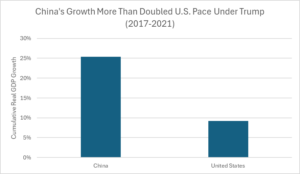

Donald Trump seems to get very confused when talking about economics. The U.S. did have respectable growth under his administration, but it was not especially good by any standard metric. We also were very far from being the fastest growing economy in the world.

Contrary to what Trump seems to believe, China’s economic growth hugely outpaced U.S. growth under his watch. China’s economy grew by a cumulative total of 25.4 percent in the years from 2017 to 2021, compared to just 9.3 percent for the United States.

Source: International Monetary Fund.

As a share of world GDP (purchasing power parity), China went from 16.15 percent at the start of the period to 18.42 percent at the end. By contrast, the U.S. share fell slightly from 15.98 percent in 2017 to 15.87 percent in 2021.

Donald Trump seems to get very confused when talking about economics. The U.S. did have respectable growth under his administration, but it was not especially good by any standard metric. We also were very far from being the fastest growing economy in the world.

Contrary to what Trump seems to believe, China’s economic growth hugely outpaced U.S. growth under his watch. China’s economy grew by a cumulative total of 25.4 percent in the years from 2017 to 2021, compared to just 9.3 percent for the United States.

Source: International Monetary Fund.

As a share of world GDP (purchasing power parity), China went from 16.15 percent at the start of the period to 18.42 percent at the end. By contrast, the U.S. share fell slightly from 15.98 percent in 2017 to 15.87 percent in 2021.

Read More Leer más Join the discussion Participa en la discusión

Kevin Erdmann argued in a Washington Post column on Thursday that the main problem with U.S. housing policy is over-restrictive lending rules from Fannie Mae and Freddie Mac. While there may be some issues with current policy being overly restrictive, that does not explain the collapse of the housing prices in 2007-2009, nor the current inadequate supply of housing.

The Atlanta example Erdmann uses in his piece is very helpful in making these points. Erdmann says there was no bubble in Atlanta’s house prices and therefore there was nothing to burst. He attributes the sharp decline in house prices in 2007-2009, and especially in the bottom tier of the housing market, to tighter credit requirements from Fannie and Freddie.

However, the data do support the case that there was a housing bubble building in the decade prior to 2007, especially in the lower tier of the housing market. Here’s the inflation-adjusted Case-Schiller index for the lower tier of the housing market (bottom third) from 1992 to the present.

As can be seen, there is a sharp rise in the index from 1996 to the middle of 2005. At that point the index levels off and then starts falling rapidly in 2007. In the price run-up, inflation-adjusted house prices for the bottom third of the market rose by 38.8 percent. This contrasts with rents in Atlanta, which rose at almost exactly the same rate as overall inflation.

This had been the general pattern for house prices in the period before the housing bubble. Nationwide house prices rose roughly in step with the rate of inflation from 1896 to 1996. There were enormous divergences across regions, with prices hugely outpacing inflation in places like New York and San Francisco, while falling far behind inflation in Detroit, St. Louis and many small cities and towns.

Erdmann points out that house prices in the lower tier of housing fell much more than the price of more expensive houses in Atlanta in the crash. This is true, but house prices at the higher end rose by much less in the bubble. Prices in the top tier rose by 27 percent in real terms over the period from 1996 to the peak in 2005.

This was still a bubble, given the trend in rents, but considerably smaller than the one in the lower tier in Atlanta. For that reason it is not surprising that there would have been a sharper fall in house prices in the bottom tier.

The other point worth noting in this graph is that house prices for the bottom tier of housing in Atlanta had largely recovered their bubble peaks just before the pandemic. Since the pandemic, real house prices for the bottom tier have actually exceeded their bubble peaks. This is true for the higher tiers as well.

This suggests that builders have serious incentive to be building lots of housing in Atlanta and elsewhere, but for some reason they are not. The tightening of credit standards by Fannie and Freddie cannot explain this failure to build more housing, since that should be reflected in house prices, which it clearly is not.

There is one other point worth noting about Erdmann’s point on Fannie and Freddie credit standards. The average credit score has risen substantially over the last two decades. This means that using a fixed credit score as a cutoff would imply a smaller share of potential borrowers are being excluded. It also would have been helpful if Erdmann had included data on mortgage issuance in the 1990s before credit standards had been relaxed and the bubble had begun to build.

In any case, this point is secondary. If excessively high credit standards were the factor that was really clogging the housing market, we should not be seeing real house prices at above their bubble peaks. These prices give builders plenty of incentive to build, but for some reason they are not constructing housing at anything like the bubble pace, or even the pre-bubble pace.

Kevin Erdmann argued in a Washington Post column on Thursday that the main problem with U.S. housing policy is over-restrictive lending rules from Fannie Mae and Freddie Mac. While there may be some issues with current policy being overly restrictive, that does not explain the collapse of the housing prices in 2007-2009, nor the current inadequate supply of housing.

The Atlanta example Erdmann uses in his piece is very helpful in making these points. Erdmann says there was no bubble in Atlanta’s house prices and therefore there was nothing to burst. He attributes the sharp decline in house prices in 2007-2009, and especially in the bottom tier of the housing market, to tighter credit requirements from Fannie and Freddie.

However, the data do support the case that there was a housing bubble building in the decade prior to 2007, especially in the lower tier of the housing market. Here’s the inflation-adjusted Case-Schiller index for the lower tier of the housing market (bottom third) from 1992 to the present.

As can be seen, there is a sharp rise in the index from 1996 to the middle of 2005. At that point the index levels off and then starts falling rapidly in 2007. In the price run-up, inflation-adjusted house prices for the bottom third of the market rose by 38.8 percent. This contrasts with rents in Atlanta, which rose at almost exactly the same rate as overall inflation.

This had been the general pattern for house prices in the period before the housing bubble. Nationwide house prices rose roughly in step with the rate of inflation from 1896 to 1996. There were enormous divergences across regions, with prices hugely outpacing inflation in places like New York and San Francisco, while falling far behind inflation in Detroit, St. Louis and many small cities and towns.

Erdmann points out that house prices in the lower tier of housing fell much more than the price of more expensive houses in Atlanta in the crash. This is true, but house prices at the higher end rose by much less in the bubble. Prices in the top tier rose by 27 percent in real terms over the period from 1996 to the peak in 2005.

This was still a bubble, given the trend in rents, but considerably smaller than the one in the lower tier in Atlanta. For that reason it is not surprising that there would have been a sharper fall in house prices in the bottom tier.

The other point worth noting in this graph is that house prices for the bottom tier of housing in Atlanta had largely recovered their bubble peaks just before the pandemic. Since the pandemic, real house prices for the bottom tier have actually exceeded their bubble peaks. This is true for the higher tiers as well.

This suggests that builders have serious incentive to be building lots of housing in Atlanta and elsewhere, but for some reason they are not. The tightening of credit standards by Fannie and Freddie cannot explain this failure to build more housing, since that should be reflected in house prices, which it clearly is not.

There is one other point worth noting about Erdmann’s point on Fannie and Freddie credit standards. The average credit score has risen substantially over the last two decades. This means that using a fixed credit score as a cutoff would imply a smaller share of potential borrowers are being excluded. It also would have been helpful if Erdmann had included data on mortgage issuance in the 1990s before credit standards had been relaxed and the bubble had begun to build.

In any case, this point is secondary. If excessively high credit standards were the factor that was really clogging the housing market, we should not be seeing real house prices at above their bubble peaks. These prices give builders plenty of incentive to build, but for some reason they are not constructing housing at anything like the bubble pace, or even the pre-bubble pace.

Read More Leer más Join the discussion Participa en la discusión

In reporting on Donald Trump’s plan to put Elon Musk in charge of a commission to ferret out waste in government, it probably would have been worth noting that there is already an agency dedicated to this purpose. The Government Accountability Office (GAO) has been in existence for over 100 years. It is non-partisan and has extensive experience in uncovering government waste.

It also would have been worth noting that having efforts to uncover massive waste is an old joke in Washington politics. Jimmy Carter claimed he would eliminate waste with his zero-based budgeting when he took office in 1977. It was quickly abandoned as too chaotic.

Bill Clinton had an effort under his administration when he put Vice-President Al Gore in charge of “reinventing government.” It may not have accomplished much but kept Al Gore out of trouble.

In addition to mentioning some of this history, it also is worth noting that there would be an extraordinary conflict of interest created by putting someone with many large government contracts and subsidies in charge of an effort to examine government efficiency. This conflict of interest problem is especially large since Trump is committing to getting rid of most of the top civil service officials, which would presumably include the leadership of the GAO. This means that the non-partisan agency created to prevent government corruption will in effect be blocked from policing Trump and Musk’s efforts to “improve” government efficiency.

In reporting on Donald Trump’s plan to put Elon Musk in charge of a commission to ferret out waste in government, it probably would have been worth noting that there is already an agency dedicated to this purpose. The Government Accountability Office (GAO) has been in existence for over 100 years. It is non-partisan and has extensive experience in uncovering government waste.

It also would have been worth noting that having efforts to uncover massive waste is an old joke in Washington politics. Jimmy Carter claimed he would eliminate waste with his zero-based budgeting when he took office in 1977. It was quickly abandoned as too chaotic.

Bill Clinton had an effort under his administration when he put Vice-President Al Gore in charge of “reinventing government.” It may not have accomplished much but kept Al Gore out of trouble.

In addition to mentioning some of this history, it also is worth noting that there would be an extraordinary conflict of interest created by putting someone with many large government contracts and subsidies in charge of an effort to examine government efficiency. This conflict of interest problem is especially large since Trump is committing to getting rid of most of the top civil service officials, which would presumably include the leadership of the GAO. This means that the non-partisan agency created to prevent government corruption will in effect be blocked from policing Trump and Musk’s efforts to “improve” government efficiency.

Read More Leer más Join the discussion Participa en la discusión

Peter Coy had a somewhat bizarre column in the New York Times yesterday warning us that even though we have gotten rid of most of the pandemic inflation with little rise in unemployment, “any further decline in inflation may not be as painless.” The column highlights a new paper by Gauti Eggertsson, one of the nation’s leading macroeconomists.

Whether or not Eggertsson’s theoretical analysis is correct, it is beside the point in terms of the current economy. We don’t need any further decline in inflation because we have already hit the Fed’s 2.0 percent target.

If it seems I am getting ahead of the game, you have to look at the data more closely. It’s true that the year over year rate in the Personal Consumption Expenditure deflator (PCE) stands a 2.5 percent, which is above the Fed’s 2.0 percent target, but we can look a bit around the corner here.

We know with virtual certainty that the rental indexes (rent proper and owners’ equivalent rent) will be showing much lower inflation in future months. The reason we can be certain of this fact is that the Bureau of Labor Statistics publishes a “New Tenant Rent Index” which tracks rents in units that change hands.

This index leads the overall rent indexes, since they are dominated by leases that could have been signed 1-3 years ago. These leases eventually end and are negotiated in ways that reflect current market conditions.

This New Tenant Rent Index has been showing sharply lower rental inflation. In fact over the last year it actually fell by 1.1 percent. This index is relatively new, so we can’t say with much precision how quickly the overall rental indexes will adjust to it or the extent to which they will adjust, but we can be quite certain that rental inflation will continue to slow, as it has for over a year.

Year over year rental inflation is currently 5.2 percent. Suppose it falls to 2.0 percent. Since these indexes comprise roughly 15 percent of the PCE deflation, this drop of 3.2 percentage points would lower the inflation rate by roughly 0.5 percentage points, bringing us to the Fed’s 2.0 percent inflation target.

Even if we take a much more modest scenario and say rental inflation falls to 3.0 percent, that still gets us to 2.2 percent, which is close enough to 2.0 percent that no serious person would spend a lot of time worrying about the difference.

Still not convinced? The annualized inflation rate over the last three months was 0.9 percent. The annualized inflation rate for the core index was 1.7 percent.

This inflation battle is over and won. Eggertsson’s work may have some useful insights for the next war on inflation, but it’s too late to be of any help in the last one.

Peter Coy had a somewhat bizarre column in the New York Times yesterday warning us that even though we have gotten rid of most of the pandemic inflation with little rise in unemployment, “any further decline in inflation may not be as painless.” The column highlights a new paper by Gauti Eggertsson, one of the nation’s leading macroeconomists.

Whether or not Eggertsson’s theoretical analysis is correct, it is beside the point in terms of the current economy. We don’t need any further decline in inflation because we have already hit the Fed’s 2.0 percent target.

If it seems I am getting ahead of the game, you have to look at the data more closely. It’s true that the year over year rate in the Personal Consumption Expenditure deflator (PCE) stands a 2.5 percent, which is above the Fed’s 2.0 percent target, but we can look a bit around the corner here.

We know with virtual certainty that the rental indexes (rent proper and owners’ equivalent rent) will be showing much lower inflation in future months. The reason we can be certain of this fact is that the Bureau of Labor Statistics publishes a “New Tenant Rent Index” which tracks rents in units that change hands.

This index leads the overall rent indexes, since they are dominated by leases that could have been signed 1-3 years ago. These leases eventually end and are negotiated in ways that reflect current market conditions.

This New Tenant Rent Index has been showing sharply lower rental inflation. In fact over the last year it actually fell by 1.1 percent. This index is relatively new, so we can’t say with much precision how quickly the overall rental indexes will adjust to it or the extent to which they will adjust, but we can be quite certain that rental inflation will continue to slow, as it has for over a year.

Year over year rental inflation is currently 5.2 percent. Suppose it falls to 2.0 percent. Since these indexes comprise roughly 15 percent of the PCE deflation, this drop of 3.2 percentage points would lower the inflation rate by roughly 0.5 percentage points, bringing us to the Fed’s 2.0 percent inflation target.

Even if we take a much more modest scenario and say rental inflation falls to 3.0 percent, that still gets us to 2.2 percent, which is close enough to 2.0 percent that no serious person would spend a lot of time worrying about the difference.

Still not convinced? The annualized inflation rate over the last three months was 0.9 percent. The annualized inflation rate for the core index was 1.7 percent.

This inflation battle is over and won. Eggertsson’s work may have some useful insights for the next war on inflation, but it’s too late to be of any help in the last one.

Read More Leer más Join the discussion Participa en la discusión

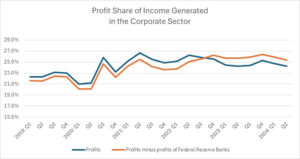

There continues to be a debate about the extent to which “price-gouging” or “greedflation” has been responsible for the rise in prices since the pandemic. We can debate the extent to which companies were able to take advantage of monopoly power during the pandemic, but whatever the cause, it is clear that the profit share of corporate income has risen from before the pandemic, as shown in the graph below.

Source: Bureau of Economic Analysis.

In the four quarters before the pandemic, the profit share averaged 22.7 percent of the net income generated in the corporate sector.[1] It rose to 26.6 percent in the second quarter of 2022, and has since fallen back somewhat to 24.3 percent in the second quarter of 2024.

This measure of profits includes the profits earned by the regional Federal Reserve Banks. Since that money is mostly refunded to the Treasury, it arguably should not be included in a measure of corporate profits.[2] In 2019 the profits share averaged 22.0 percent of net income, excluding the profits of the Federal Reserve Banks. This share peaked at 26.2 percent in the fourth quarter of 2022, it has edged down to 25.3 percent in the most recent quarter. (The regional Federal Reserve Banks are currently losing money as a result of higher interest rates, so the profit share is higher when these loses are excluded.)

By either measure the profit share in the most recent quarter is higher than before the pandemic. Using the first measure, the share has increased by 1.6 percentage points from the four quarters before the pandemic. By the measure that excludes the profits of Federal Reserve Banks, the profit share has risen by 3.3 percentage points.

We can argue whether we want to describe this shift from labor to capital as “big” or “small.” It clearly does not explain the bulk of the inflation we have seen since the pandemic. Inflation as measured by the CPI has been 20.9 percent since the start of the pandemic. That means the rise in profit shares, using the measure that excludes profits from the Federal Reserve Banks, explains a bit more than 15 percent of the inflation we saw.

On the other hand, the impact looks considerably more important if we compare it to real wage growth over this period. Real hourly wages have risen just 1.6 percent since the pandemic. If the profit shares had remained constant over the last four and a half years, wages would be roughly 3.3 percent higher than they are now, which would translate into real wages being roughly 3.3 percent higher. That would triple the amount of real wage growth we have seen over this period. (This is a crude calculation, since some items in the consumption basket, most notably rental housing, are not primarily produced by the corporate sector.)

In short, we can debate the dynamics of inflation and the shift from wages to profits in the pandemic. But the fact that there was a substantial shift is difficult to dispute.

There is one important qualification to this story. There has been an unusually large statistical discrepancy in the GDP accounts in recent quarters, rising to 2.7 percent of GDP in the second quarter of 2024 (NIPA Table 1.7.5., Line 34). The statistical discrepancy is the gap between GDP as measured on the output side and GDP as measured on the income side.

In principle, these two numbers should be equal, in the same way that if we counted people starting from the left side of the room we should end up with the same number as if we counted people starting from the right side of the room. As a practical matter, in a $27 trillion economy, they will never come out exactly the same.

As it stands, the output side measure is considerably higher than the income side measure. It may turn out that with future revisions, the output side measure is revised down, and the income side measure proves to be closer to the mark.

However, it may also turn out to be the case that the income side measure is seriously under-estimated and revised up to a level close to the output measure. In that case, the balance between profits and labor compensation could be affected by future revisions. To take an extreme case, if the full statistical discrepancy was found to be an undercount of labor income, then the reported rise in the profit share would largely disappear.

To be clear, assuming that all the gap was an undercount on the income side, and this was in turn entirely an undercounting of labor compensation, would be very extreme and unlikely. But it is important to note that the picture may look different when we get revisions to the data, both this month and in subsequent years.

In the meantime, we have to work with the data we have. And these data show there was a substantial redistribution from labor to capital in the period since the pandemic hit.

Addendum: After posting this note, I realized I should have deducted the profits of Federal Reserve Banks from the denominator. This would have raised the profit share in 2019 by 0.1 pp to 22.1 percent and lowered in the most recent quarter by 0.2 pp to 25.1 percent. That would make the rise in profit shares 3.0 percentage points instead of 3.3 percentage points.

[1] This calculation takes net operating surplus (profits, interest, and business transfers), NIPA Table 1.14, Line 24 over the sum of net operating surplus and labor compensation, NIPA Table 1.14, Line 20.

[2] The Federal Reserve Bank profits are taken from NIPA Table 6.16D, Line 11.

There continues to be a debate about the extent to which “price-gouging” or “greedflation” has been responsible for the rise in prices since the pandemic. We can debate the extent to which companies were able to take advantage of monopoly power during the pandemic, but whatever the cause, it is clear that the profit share of corporate income has risen from before the pandemic, as shown in the graph below.

Source: Bureau of Economic Analysis.

In the four quarters before the pandemic, the profit share averaged 22.7 percent of the net income generated in the corporate sector.[1] It rose to 26.6 percent in the second quarter of 2022, and has since fallen back somewhat to 24.3 percent in the second quarter of 2024.

This measure of profits includes the profits earned by the regional Federal Reserve Banks. Since that money is mostly refunded to the Treasury, it arguably should not be included in a measure of corporate profits.[2] In 2019 the profits share averaged 22.0 percent of net income, excluding the profits of the Federal Reserve Banks. This share peaked at 26.2 percent in the fourth quarter of 2022, it has edged down to 25.3 percent in the most recent quarter. (The regional Federal Reserve Banks are currently losing money as a result of higher interest rates, so the profit share is higher when these loses are excluded.)

By either measure the profit share in the most recent quarter is higher than before the pandemic. Using the first measure, the share has increased by 1.6 percentage points from the four quarters before the pandemic. By the measure that excludes the profits of Federal Reserve Banks, the profit share has risen by 3.3 percentage points.

We can argue whether we want to describe this shift from labor to capital as “big” or “small.” It clearly does not explain the bulk of the inflation we have seen since the pandemic. Inflation as measured by the CPI has been 20.9 percent since the start of the pandemic. That means the rise in profit shares, using the measure that excludes profits from the Federal Reserve Banks, explains a bit more than 15 percent of the inflation we saw.

On the other hand, the impact looks considerably more important if we compare it to real wage growth over this period. Real hourly wages have risen just 1.6 percent since the pandemic. If the profit shares had remained constant over the last four and a half years, wages would be roughly 3.3 percent higher than they are now, which would translate into real wages being roughly 3.3 percent higher. That would triple the amount of real wage growth we have seen over this period. (This is a crude calculation, since some items in the consumption basket, most notably rental housing, are not primarily produced by the corporate sector.)

In short, we can debate the dynamics of inflation and the shift from wages to profits in the pandemic. But the fact that there was a substantial shift is difficult to dispute.

There is one important qualification to this story. There has been an unusually large statistical discrepancy in the GDP accounts in recent quarters, rising to 2.7 percent of GDP in the second quarter of 2024 (NIPA Table 1.7.5., Line 34). The statistical discrepancy is the gap between GDP as measured on the output side and GDP as measured on the income side.

In principle, these two numbers should be equal, in the same way that if we counted people starting from the left side of the room we should end up with the same number as if we counted people starting from the right side of the room. As a practical matter, in a $27 trillion economy, they will never come out exactly the same.

As it stands, the output side measure is considerably higher than the income side measure. It may turn out that with future revisions, the output side measure is revised down, and the income side measure proves to be closer to the mark.

However, it may also turn out to be the case that the income side measure is seriously under-estimated and revised up to a level close to the output measure. In that case, the balance between profits and labor compensation could be affected by future revisions. To take an extreme case, if the full statistical discrepancy was found to be an undercount of labor income, then the reported rise in the profit share would largely disappear.

To be clear, assuming that all the gap was an undercount on the income side, and this was in turn entirely an undercounting of labor compensation, would be very extreme and unlikely. But it is important to note that the picture may look different when we get revisions to the data, both this month and in subsequent years.

In the meantime, we have to work with the data we have. And these data show there was a substantial redistribution from labor to capital in the period since the pandemic hit.

Addendum: After posting this note, I realized I should have deducted the profits of Federal Reserve Banks from the denominator. This would have raised the profit share in 2019 by 0.1 pp to 22.1 percent and lowered in the most recent quarter by 0.2 pp to 25.1 percent. That would make the rise in profit shares 3.0 percentage points instead of 3.3 percentage points.

[1] This calculation takes net operating surplus (profits, interest, and business transfers), NIPA Table 1.14, Line 24 over the sum of net operating surplus and labor compensation, NIPA Table 1.14, Line 20.

[2] The Federal Reserve Bank profits are taken from NIPA Table 6.16D, Line 11.

Read More Leer más Join the discussion Participa en la discusión