Morning Edition had an interesting segment reporting on a new effort to promote open source seeds. These seeds could be freely reproduced and varied, as long as any resulting seeds were also freely available.

Unfortunately this piece did not fully flesh out the economic implications of this movement. While it included the comments of the representative of a seed company, saying that it would likely avoid open source seed in order to be able to continue to sell patent protected seed, it didn’t include any discussion of the larger implications of patents in seeds.

The seed companies and many of their top executives and scientists are getting very rich from patent protected seeds. This is not technology. This is not technology. (Sorry, had to repeat this in case any economists were reading.) This is the result of a government policy that hands out monopolies to certain companies and threatens to arrest competitors.

Patent monopolies are one way to finance research into developing new seeds. It is certainly not the only way. Much of the research into agriculture is paid by universities or government agencies. The government could increases this sort of funding to replace the research done by the private sector.

This would allow all seeds to be available at the free market price. This would likely eliminate many of the large fortunes earned by selling seeds. It would also eliminate the enormous distortions associated with patent protected prices. If the patent leads to a price that is 500 hundred or 1000 percent above the free market price it leads to the same amount of economic waste as if the government were to impose a tariff of 500 or 1000 percent on imports of the seed.

Publiclly funded research would also likely lead to more effective development of new seeds since making all research findings public could be a requirement for getting public funding. Under a system supported by patent monopolies companies only make available the information needed to get a patent. In fact, they have a strong financial incentive to misrepresent and conceal research findings in order to promote their product and inhibit competitors.

Since science advances much more rapidly in a context of open research it would have been worth including this point in the discussion. It also is important to point out that, insofar as patent protected products are a source of great wealth and a factor in inequality, it is the outcome of government policy, not technology.

Morning Edition had an interesting segment reporting on a new effort to promote open source seeds. These seeds could be freely reproduced and varied, as long as any resulting seeds were also freely available.

Unfortunately this piece did not fully flesh out the economic implications of this movement. While it included the comments of the representative of a seed company, saying that it would likely avoid open source seed in order to be able to continue to sell patent protected seed, it didn’t include any discussion of the larger implications of patents in seeds.

The seed companies and many of their top executives and scientists are getting very rich from patent protected seeds. This is not technology. This is not technology. (Sorry, had to repeat this in case any economists were reading.) This is the result of a government policy that hands out monopolies to certain companies and threatens to arrest competitors.

Patent monopolies are one way to finance research into developing new seeds. It is certainly not the only way. Much of the research into agriculture is paid by universities or government agencies. The government could increases this sort of funding to replace the research done by the private sector.

This would allow all seeds to be available at the free market price. This would likely eliminate many of the large fortunes earned by selling seeds. It would also eliminate the enormous distortions associated with patent protected prices. If the patent leads to a price that is 500 hundred or 1000 percent above the free market price it leads to the same amount of economic waste as if the government were to impose a tariff of 500 or 1000 percent on imports of the seed.

Publiclly funded research would also likely lead to more effective development of new seeds since making all research findings public could be a requirement for getting public funding. Under a system supported by patent monopolies companies only make available the information needed to get a patent. In fact, they have a strong financial incentive to misrepresent and conceal research findings in order to promote their product and inhibit competitors.

Since science advances much more rapidly in a context of open research it would have been worth including this point in the discussion. It also is important to point out that, insofar as patent protected products are a source of great wealth and a factor in inequality, it is the outcome of government policy, not technology.

Read More Leer más Join the discussion Participa en la discusión

The NYT headlined a piece on the dismal state of Russia’s economy, “Russia economy worsens even before sanctions hit.” The piece goes on to describe an economy in decline telling readers about Russians moving abroad and storing cash in safe deposit boxes and foreign currencies. It reports:

“Russia’s $2 trillion economy was suffering from stagflation, that toxic mix of stagnant growth and high inflation typically accompanied by a spike in unemployment. In Russia, joblessness remains low, but only because years of population decline have produced a shrunken, inadequate labor force.”

The data from the I.M.F. tell a somewhat different picture. While growth has slowed in the last two years, per capita income has more than doubled in the country since Vladimir Putin took office in 1998. The NYT may not like Russia’s “shrunken inadequate labor force,” but members of this shrunken, inadequate labor force probably care more about the unemployment rate than the NYT’s condemnations.

The I.M.F. projects an inflation rate of 6.2 percent for both this year and next. This is high for members of the 2.0 percent inflation cult that occupies central banks in the west and top economics departments, but folks familiar with economic data know that many countries have had long stretches of healthy growth with higher inflation rates. While the piece did find people who were unhappy about this inflation rate, people with better memories would recall that Russia had double-digit inflation as recently as 2008.

While the private equity investor who is one of the main sources for the piece predicts that Russia will default on its debt, it’s difficult to see the basis for this assertion in the data. The I.M.F. reports that it has a deficit of less than 1.0 percent of GDP and its debt-to-GDP ratio have been on a downward course. It has a current account surplus. Furthermore, the I.M.F. shows that investment is almost 24 percent of GDP. This compares to less than 20 percent in the United States.

In short, the data for Russia reported by the I.M.F. would be consistent with the 80 percent approval rating for Putin that the article mentions, even if the economic picture painted by the NYT is not.

The NYT headlined a piece on the dismal state of Russia’s economy, “Russia economy worsens even before sanctions hit.” The piece goes on to describe an economy in decline telling readers about Russians moving abroad and storing cash in safe deposit boxes and foreign currencies. It reports:

“Russia’s $2 trillion economy was suffering from stagflation, that toxic mix of stagnant growth and high inflation typically accompanied by a spike in unemployment. In Russia, joblessness remains low, but only because years of population decline have produced a shrunken, inadequate labor force.”

The data from the I.M.F. tell a somewhat different picture. While growth has slowed in the last two years, per capita income has more than doubled in the country since Vladimir Putin took office in 1998. The NYT may not like Russia’s “shrunken inadequate labor force,” but members of this shrunken, inadequate labor force probably care more about the unemployment rate than the NYT’s condemnations.

The I.M.F. projects an inflation rate of 6.2 percent for both this year and next. This is high for members of the 2.0 percent inflation cult that occupies central banks in the west and top economics departments, but folks familiar with economic data know that many countries have had long stretches of healthy growth with higher inflation rates. While the piece did find people who were unhappy about this inflation rate, people with better memories would recall that Russia had double-digit inflation as recently as 2008.

While the private equity investor who is one of the main sources for the piece predicts that Russia will default on its debt, it’s difficult to see the basis for this assertion in the data. The I.M.F. reports that it has a deficit of less than 1.0 percent of GDP and its debt-to-GDP ratio have been on a downward course. It has a current account surplus. Furthermore, the I.M.F. shows that investment is almost 24 percent of GDP. This compares to less than 20 percent in the United States.

In short, the data for Russia reported by the I.M.F. would be consistent with the 80 percent approval rating for Putin that the article mentions, even if the economic picture painted by the NYT is not.

Read More Leer más Join the discussion Participa en la discusión

In an article reporting on a speech by Federal Reserve Board Chair Janet Yellen, the Post told readers:

“One of the puzzles currently confounding economists is why inflation has remained so low even as the recovery has picked up steam. The Fed set a 2 percent inflation target but its preferred measure of price changes shows inflation is about half that.”

Actually economists are not at all confounded by why inflation has remained low. The predominant view of inflation is that the change in the rate of inflation depends on the level of unemployment. Since nearly all economists believe the unemployment rate is still above its trend level, they expect inflation to be falling, not rising. In fact the bigger mystery from the standpoint of standard economic models is why the rate of inflation has not fallen more. (The answer is that wages and prices tend to be sticky going downward.)

Anyhow, the confounding is only at the Washington Post. The low inflation rate is not something economists have trouble explaining.

In an article reporting on a speech by Federal Reserve Board Chair Janet Yellen, the Post told readers:

“One of the puzzles currently confounding economists is why inflation has remained so low even as the recovery has picked up steam. The Fed set a 2 percent inflation target but its preferred measure of price changes shows inflation is about half that.”

Actually economists are not at all confounded by why inflation has remained low. The predominant view of inflation is that the change in the rate of inflation depends on the level of unemployment. Since nearly all economists believe the unemployment rate is still above its trend level, they expect inflation to be falling, not rising. In fact the bigger mystery from the standpoint of standard economic models is why the rate of inflation has not fallen more. (The answer is that wages and prices tend to be sticky going downward.)

Anyhow, the confounding is only at the Washington Post. The low inflation rate is not something economists have trouble explaining.

Read More Leer más Join the discussion Participa en la discusión

The Huffington Post really deserves to be called on the carpet for this piece. It implies there is a debate going on between Paul Krugman and Joe Scarborough over whether the Obama administration is tampering with Census data to make the Affordable Care Act look good.

There is no debate because Scarborough has no clue what he is taking about. He knows nothing about how the Census Bureau collects data and what is involved in changing questions as it is now doing. He is literally making a completely baseless accusation. He doesn’t even pretend to have a shred of evidence to support his claim that the Obama administration is tampering with the data.

If he knew anything about the way Census worked, he would know it would be incredibly difficult for the Obama administration to alter its processes. There would almost certainly be people willing to talk if this were the case. Furthermore, any competent analyst would be able to recognize doctored data using other data sets.

Anyhow, Scarborough is not taking part in a debate, he is name calling. This is like someone running out on the baseball field and yelling at the stupid players because it would be much quicker to go from second base to home by running over the pitcher’s mound. If Scarborough wants to have a serious debate with Paul Krugman or anyone else about the data coming from Census Bureau he will first have to learn a bit about the subject matter. Until then, he deserves nothing but ridicule from any serious news outlet.

The Huffington Post really deserves to be called on the carpet for this piece. It implies there is a debate going on between Paul Krugman and Joe Scarborough over whether the Obama administration is tampering with Census data to make the Affordable Care Act look good.

There is no debate because Scarborough has no clue what he is taking about. He knows nothing about how the Census Bureau collects data and what is involved in changing questions as it is now doing. He is literally making a completely baseless accusation. He doesn’t even pretend to have a shred of evidence to support his claim that the Obama administration is tampering with the data.

If he knew anything about the way Census worked, he would know it would be incredibly difficult for the Obama administration to alter its processes. There would almost certainly be people willing to talk if this were the case. Furthermore, any competent analyst would be able to recognize doctored data using other data sets.

Anyhow, Scarborough is not taking part in a debate, he is name calling. This is like someone running out on the baseball field and yelling at the stupid players because it would be much quicker to go from second base to home by running over the pitcher’s mound. If Scarborough wants to have a serious debate with Paul Krugman or anyone else about the data coming from Census Bureau he will first have to learn a bit about the subject matter. Until then, he deserves nothing but ridicule from any serious news outlet.

Read More Leer más Join the discussion Participa en la discusión

How rich would Bill Gates be if anyone in the world could make a computer with the latest version of Windows without even sending him a thank you note? Think about this question as you read Eduardo Porter’s piece on how technology might be shifting income towards capital making society ever more unequal.

Porter is of course right, we have seen a large shift in income from labor to capital across the world over the last three decades. However it is difficult to see how this could be seen as technologically determined when so much of this shift was clearly attributable to patent rents and other laws that certainly were not determined by technology. If current patterns of growth are increasing inequality it is because we have designed a legal and institutional system to bring about this outcome. There is nothing natural about this pattern of development. (in addition to the Bill Gates example, imagine what would happen to Walmart’s profits if it executives faced criminal penalties for violations of labor laws.)

How rich would Bill Gates be if anyone in the world could make a computer with the latest version of Windows without even sending him a thank you note? Think about this question as you read Eduardo Porter’s piece on how technology might be shifting income towards capital making society ever more unequal.

Porter is of course right, we have seen a large shift in income from labor to capital across the world over the last three decades. However it is difficult to see how this could be seen as technologically determined when so much of this shift was clearly attributable to patent rents and other laws that certainly were not determined by technology. If current patterns of growth are increasing inequality it is because we have designed a legal and institutional system to bring about this outcome. There is nothing natural about this pattern of development. (in addition to the Bill Gates example, imagine what would happen to Walmart’s profits if it executives faced criminal penalties for violations of labor laws.)

Read More Leer más Join the discussion Participa en la discusión

Last month the WSJ ran a column by Ed Lazear, a Stanford economics professor and former chief economist to President Bush, which noted the decline in the length of the average workweek between the fall and the most recent data from February. The piece noted that if labor demand was measured in hours, we had lost the equivalent of 100,000 jobs over the prior six months. He discussed possible causes for this decline and highlighted the incentives created by the Affordable Care Act.

While some of us at the time questioned the plausibility of this story and noted the likely effect of the weather on reducing workweeks in January and February, we got the question resolved when the March data was released this month. The entire decline in average hours was reversed. The question is whether the WSJ will allow Mr. Lazear a follow-up piece to point out that his earlier concerns about the Affordable Care Act leading to a reduction in the length of the average workweek had apparently been wrong.

Source: Bureau of Labor Statistics.

Last month the WSJ ran a column by Ed Lazear, a Stanford economics professor and former chief economist to President Bush, which noted the decline in the length of the average workweek between the fall and the most recent data from February. The piece noted that if labor demand was measured in hours, we had lost the equivalent of 100,000 jobs over the prior six months. He discussed possible causes for this decline and highlighted the incentives created by the Affordable Care Act.

While some of us at the time questioned the plausibility of this story and noted the likely effect of the weather on reducing workweeks in January and February, we got the question resolved when the March data was released this month. The entire decline in average hours was reversed. The question is whether the WSJ will allow Mr. Lazear a follow-up piece to point out that his earlier concerns about the Affordable Care Act leading to a reduction in the length of the average workweek had apparently been wrong.

Source: Bureau of Labor Statistics.

Read More Leer más Join the discussion Participa en la discusión

Hey, who isn’t? His column today raises the possibility that because the long-term unemployed are effectively excluded from the labor market, they don’t exert downward pressure on the inflation rate. This means that we should only focus on the short-term unemployment rate, which is already near its average rate over the last two decades.

There are many reasons for not accepting this view. For example, if the number of short-term unemployed dwindled, it is likely that employers would start to look to the longer term unemployed as a source of labor. However even if we accepted the story outlined in Samuelson’s piece, it is difficult to see how anyone could be concerned about the rate of unemployment falling to a level that is inconsistent with stable inflation.

According to the Congressional Budget Office the terms of a trade-off between the acceleration of inflation and unemployment have changed in recent years. In their most recent analysis, they estimated that being a full percentage point below the non-accelerating inflation rate of unemployment (NAIRU) for a full year will lead to a 0.3 percentage point increase in the inflation rate.

This means that if the NAIRU is actually 6.0 percent and the Fed were to flub things and let the unemployment rate fall to 5.0 percent for a full year, then the core consumption expenditure deflator (the Fed’s main measure of inflation) would rise from 1.3 percent to 1.6 percent. Pretty scary stuff.

In short, it’s pretty hard to see the downside risk in this picture. The Fed targets a 2.0 percent rate of inflation, there are arguably reasons we should be looking to an even higher rate (@ 3-4 percent). If we accept the NAIRU story in its entirety and assume that we are already getting close to it, we will still have many years before the inflation rate would rise to a pace that provides a real basis for concern.

Hey, who isn’t? His column today raises the possibility that because the long-term unemployed are effectively excluded from the labor market, they don’t exert downward pressure on the inflation rate. This means that we should only focus on the short-term unemployment rate, which is already near its average rate over the last two decades.

There are many reasons for not accepting this view. For example, if the number of short-term unemployed dwindled, it is likely that employers would start to look to the longer term unemployed as a source of labor. However even if we accepted the story outlined in Samuelson’s piece, it is difficult to see how anyone could be concerned about the rate of unemployment falling to a level that is inconsistent with stable inflation.

According to the Congressional Budget Office the terms of a trade-off between the acceleration of inflation and unemployment have changed in recent years. In their most recent analysis, they estimated that being a full percentage point below the non-accelerating inflation rate of unemployment (NAIRU) for a full year will lead to a 0.3 percentage point increase in the inflation rate.

This means that if the NAIRU is actually 6.0 percent and the Fed were to flub things and let the unemployment rate fall to 5.0 percent for a full year, then the core consumption expenditure deflator (the Fed’s main measure of inflation) would rise from 1.3 percent to 1.6 percent. Pretty scary stuff.

In short, it’s pretty hard to see the downside risk in this picture. The Fed targets a 2.0 percent rate of inflation, there are arguably reasons we should be looking to an even higher rate (@ 3-4 percent). If we accept the NAIRU story in its entirety and assume that we are already getting close to it, we will still have many years before the inflation rate would rise to a pace that provides a real basis for concern.

Read More Leer más Join the discussion Participa en la discusión

The NYT is continuing its parody of news reporting with a piece that discusses the budget proposals of France’s Prime Minister, Manuel Valls. It told readers:

“On Tuesday, Mr. Valls offered the most detailed summary yet of how the government intends to meet its promise to enact Really Big Number in spending cuts by 2017. He called for Really Big Number in cuts to the central government bureaucracy, Really Big Number to the national health care system and Really Big Number to local governments — an element at which many legislators on the right booed loudly, having just won control of a number of local governments. He did not specify how the remaining Really Big Number in cuts would be made.”

Okay that is not exactly what the piece said. Here’s the actual paragraph:

“On Tuesday, Mr. Valls offered the most detailed summary yet of how the government intends to meet its promise to enact $69 billion in spending cuts by 2017. He called for $26 billion in cuts to the central government bureaucracy, $13.8 billion to the national health care system and $13.8 billion to local governments — an element at which many legislators on the right booed loudly, having just won control of a number of local governments. He did not specify how the remaining $15.4 billion in cuts would be made.”

Did this provide any more information than the “Really Big Number” paragraph? The piece provides no information on how much is currently spent on these programs, nor is it even clear whether these cuts refer to a single year’s spending (presumably 2017), or some aggregate over 2015-2017. The NYT surely has some readers who are sufficiently familiar with France’s budget to make sense of the numbers in this article, but to the other 99.9 percent of readers, these numbers provided no information whatsoever.

The NYT is continuing its parody of news reporting with a piece that discusses the budget proposals of France’s Prime Minister, Manuel Valls. It told readers:

“On Tuesday, Mr. Valls offered the most detailed summary yet of how the government intends to meet its promise to enact Really Big Number in spending cuts by 2017. He called for Really Big Number in cuts to the central government bureaucracy, Really Big Number to the national health care system and Really Big Number to local governments — an element at which many legislators on the right booed loudly, having just won control of a number of local governments. He did not specify how the remaining Really Big Number in cuts would be made.”

Okay that is not exactly what the piece said. Here’s the actual paragraph:

“On Tuesday, Mr. Valls offered the most detailed summary yet of how the government intends to meet its promise to enact $69 billion in spending cuts by 2017. He called for $26 billion in cuts to the central government bureaucracy, $13.8 billion to the national health care system and $13.8 billion to local governments — an element at which many legislators on the right booed loudly, having just won control of a number of local governments. He did not specify how the remaining $15.4 billion in cuts would be made.”

Did this provide any more information than the “Really Big Number” paragraph? The piece provides no information on how much is currently spent on these programs, nor is it even clear whether these cuts refer to a single year’s spending (presumably 2017), or some aggregate over 2015-2017. The NYT surely has some readers who are sufficiently familiar with France’s budget to make sense of the numbers in this article, but to the other 99.9 percent of readers, these numbers provided no information whatsoever.

Read More Leer más Join the discussion Participa en la discusión

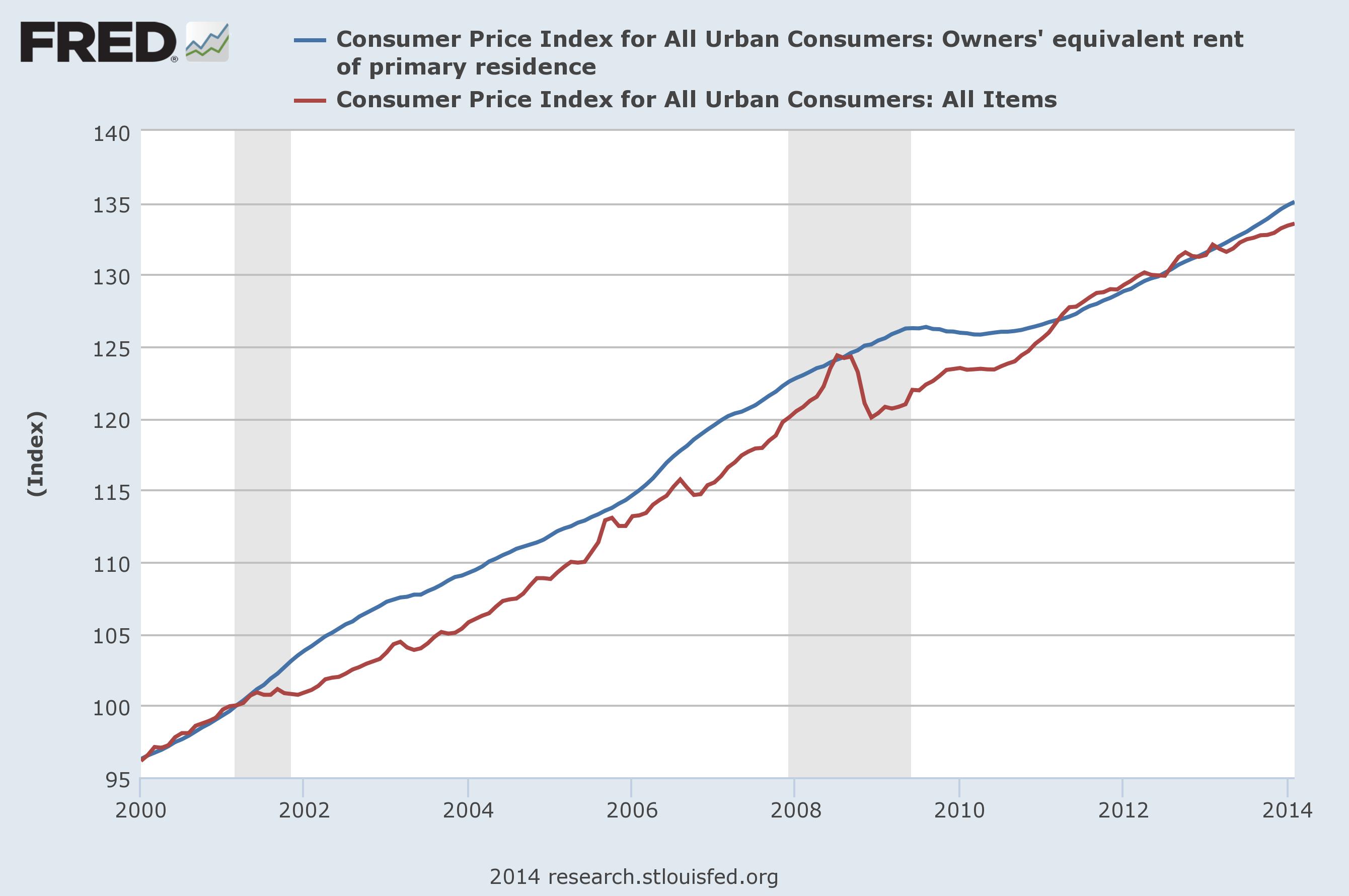

The NYT had an interesting piece on how a rapidly growing number of people are finding rents unaffordable (defined as more than 30 percent of gross income. There are two reasons that rents can rise in price. The first is that the same units cost more money. The second reason is that the mix of rental units change so that the the typical unit costs more.

It is clear that the main cause of higher rents is the latter, as shown below.

This graph shows that the owner equivalent rent index from the Consumer Price Index (CPI) has almost exactly tracked the overall rate of inflation since the start of the century. (I used owner equivalent rent since this excludes the cost of utilities. The cost of utilities has likely outpaced inflation, but that is a somewhat different story.)

If this index from the CPI, which is effectively a quality adjusted price index, is not outpacing inflation, then it implies that the problem must be the quality is getting better. In other words, the units added to the rental housing stock (either by new construction or conversion of ownership units) are either bigger or better in some way than the average rental unit in 2000.

The other factor that could explain a rise in the ratio of the median rental price to income is a decline in real income, which we have seen to some extent in this century. In that case the problem is not really high housing prices, but low wages.

The NYT had an interesting piece on how a rapidly growing number of people are finding rents unaffordable (defined as more than 30 percent of gross income. There are two reasons that rents can rise in price. The first is that the same units cost more money. The second reason is that the mix of rental units change so that the the typical unit costs more.

It is clear that the main cause of higher rents is the latter, as shown below.

This graph shows that the owner equivalent rent index from the Consumer Price Index (CPI) has almost exactly tracked the overall rate of inflation since the start of the century. (I used owner equivalent rent since this excludes the cost of utilities. The cost of utilities has likely outpaced inflation, but that is a somewhat different story.)

If this index from the CPI, which is effectively a quality adjusted price index, is not outpacing inflation, then it implies that the problem must be the quality is getting better. In other words, the units added to the rental housing stock (either by new construction or conversion of ownership units) are either bigger or better in some way than the average rental unit in 2000.

The other factor that could explain a rise in the ratio of the median rental price to income is a decline in real income, which we have seen to some extent in this century. In that case the problem is not really high housing prices, but low wages.

Read More Leer más Join the discussion Participa en la discusión

That’s what readers of this NYT piece must have been asking. It reported:

“It [the I.M.F.] has urged Tokyo to make structural reforms to bolster its labor market, by, for instance, bringing women into the work force.”

This seems strange since the OECD reports that the employment to population ratio for prime age women in Japan (25-54) was 71.5 percent in the third quarter of 2013, the most recent data available. By comparison it was 69.4 percent in the United States.

Addendum:

From comments below and other comments I have received, I realize I need to clarify my point. From all the data I have seen and accounts I have heard, Japan continues to be a very sexist society and women almost certainly face more discrimination than in the United States. I was simply saying that their problem is not bringing women into the workforce. On that score the country has done remarkably well. The employment to population ratio for prime age women rose from 67.6 percent in 2007, before the recession, to 71.5 percent in the most recent quarter. By contrast, in the United States it fell from 72.5 percent to 69.4 percent over the same period. Based on these data , getting women into the labor force is one thing that Japan seems to be doing well.

Note: numbers were corrected to show employment to population ratios for prime age women.

That’s what readers of this NYT piece must have been asking. It reported:

“It [the I.M.F.] has urged Tokyo to make structural reforms to bolster its labor market, by, for instance, bringing women into the work force.”

This seems strange since the OECD reports that the employment to population ratio for prime age women in Japan (25-54) was 71.5 percent in the third quarter of 2013, the most recent data available. By comparison it was 69.4 percent in the United States.

Addendum:

From comments below and other comments I have received, I realize I need to clarify my point. From all the data I have seen and accounts I have heard, Japan continues to be a very sexist society and women almost certainly face more discrimination than in the United States. I was simply saying that their problem is not bringing women into the workforce. On that score the country has done remarkably well. The employment to population ratio for prime age women rose from 67.6 percent in 2007, before the recession, to 71.5 percent in the most recent quarter. By contrast, in the United States it fell from 72.5 percent to 69.4 percent over the same period. Based on these data , getting women into the labor force is one thing that Japan seems to be doing well.

Note: numbers were corrected to show employment to population ratios for prime age women.

Read More Leer más Join the discussion Participa en la discusión