The failure of Silicon Valley Bank yesterday overtook the really big event of the day, the February jobs report. The 311,000 jobs were far more than I had expected. I thought the huge January number was a fluke of seasonal adjustments and unusually good winter weather. For that reason, I expected the February number to be very weak, not because I thought the labor market had crashed, but just as a correction to the high number in January.

I was wrong in a very big way. The January number was obviously real and the economy is still creating jobs at a very rapid clip.

This is somewhat concerning in that there is no way the economy can keep creating jobs at this pace without seeing some serious inflationary pressure, but this is where the other part of the good news story comes in. Wage growth slowed in February. The slower growth in February, combined with a downward revision to the January number, gave us a 3.6 percent annual rate of wage growth over the last three months.

This pace of wage growth is consistent with the Fed’s 2.0 percent inflation target. We had wage growth at this pace through much of 2018 and 2019 even as inflation was coming in slightly under the targeted rate.

I ordinarily would not be cheering slower wage growth, but the reality is that the Fed is determined to bring inflation down towards its target. If wages are growing at a pace that is faster than is consistent with its target, it will keep raising rates, and throwing people out of work, until wage growth slows.

If wage growth is now more or less in line with the 2.0 percent target, then the Fed can hold off on further rate hikes. Hopefully, it would then allow the economy to continue to grow with the unemployment rate remaining near 3.5 percent.

Of course, we do need to see real wage growth and inflation has been running faster than 3.5 percent. However, there are good reasons for believing that inflation will be slowing in the months ahead. Most importantly, we know that inflation in rents will slow sharply, as private indexes measuring rents of units coming up on the market have showed little or no inflation in recent months. The CPI rent index, which measures the rent of all units (both those that come up on the market and those with a continuing tenant) follows these indices with a lag of 6-12 months.

It is also likely that we will see further drops in many of the supply chain goods, most importantly cars, where temporary shortages sent prices soaring in the pandemic. This will help put downward pressure on inflation in goods, and also services like car repairs, where the cost of goods is a large part of the price.

And, we are also likely to see less inflation in food prices. The wholesale prices of many items, most notably eggs, has fallen sharply in the last couple of months. This should show up in lower prices in stores.

If we have a story where wages are rising at a 3.6 percent annual rate, and inflation falls to under 2.5 percent, then we would be seeing a respectable pace of real wage growth. We can hope for better, and also that we continue to see disproportionate growth at the bottom, but low unemployment and modest real wage growth is a pretty good picture.

The failure of Silicon Valley Bank yesterday overtook the really big event of the day, the February jobs report. The 311,000 jobs were far more than I had expected. I thought the huge January number was a fluke of seasonal adjustments and unusually good winter weather. For that reason, I expected the February number to be very weak, not because I thought the labor market had crashed, but just as a correction to the high number in January.

I was wrong in a very big way. The January number was obviously real and the economy is still creating jobs at a very rapid clip.

This is somewhat concerning in that there is no way the economy can keep creating jobs at this pace without seeing some serious inflationary pressure, but this is where the other part of the good news story comes in. Wage growth slowed in February. The slower growth in February, combined with a downward revision to the January number, gave us a 3.6 percent annual rate of wage growth over the last three months.

This pace of wage growth is consistent with the Fed’s 2.0 percent inflation target. We had wage growth at this pace through much of 2018 and 2019 even as inflation was coming in slightly under the targeted rate.

I ordinarily would not be cheering slower wage growth, but the reality is that the Fed is determined to bring inflation down towards its target. If wages are growing at a pace that is faster than is consistent with its target, it will keep raising rates, and throwing people out of work, until wage growth slows.

If wage growth is now more or less in line with the 2.0 percent target, then the Fed can hold off on further rate hikes. Hopefully, it would then allow the economy to continue to grow with the unemployment rate remaining near 3.5 percent.

Of course, we do need to see real wage growth and inflation has been running faster than 3.5 percent. However, there are good reasons for believing that inflation will be slowing in the months ahead. Most importantly, we know that inflation in rents will slow sharply, as private indexes measuring rents of units coming up on the market have showed little or no inflation in recent months. The CPI rent index, which measures the rent of all units (both those that come up on the market and those with a continuing tenant) follows these indices with a lag of 6-12 months.

It is also likely that we will see further drops in many of the supply chain goods, most importantly cars, where temporary shortages sent prices soaring in the pandemic. This will help put downward pressure on inflation in goods, and also services like car repairs, where the cost of goods is a large part of the price.

And, we are also likely to see less inflation in food prices. The wholesale prices of many items, most notably eggs, has fallen sharply in the last couple of months. This should show up in lower prices in stores.

If we have a story where wages are rising at a 3.6 percent annual rate, and inflation falls to under 2.5 percent, then we would be seeing a respectable pace of real wage growth. We can hope for better, and also that we continue to see disproportionate growth at the bottom, but low unemployment and modest real wage growth is a pretty good picture.

Read More Leer más Join the discussion Participa en la discusión

As regular BTP readers know, I constantly harangue news outlets to put really big numbers in context. As these outlets know, none of their readers has any idea of what spending or taxing $2 trillion over a decade means. It is a huge number and if they added or subtracted a zero at the end, it would still be a huge number and probably mean the same thing to the vast majority of their audience.

Therefore, I have always advocated putting these numbers in some context, like a percent of the budget, a percent of GDP, or per person cost. This should require all of about 15 seconds from the reporter doing the piece, and add maybe 15 words to a typical story, but for some reason, the New York Times, Washington Post, National Public Radio, and the rest seem unable to do it.

New York Times columnist Christopher Caldwell got my message but used it to lie to his readers. In a column making a reasonable complaint about presidents abusing “emergency” powers, he tells readers:

“President Biden’s plan [for student loan forgiveness] would forgive a quarter of the roughly $1.6 trillion in federal student debt held by some 43 million Americans — about $400 billion, or roughly 2 percent of gross domestic product.”

The lie in this sentence is the reference to 2 percent of GDP. The $400 billion figure is roughly 2.0 percent of this year’s GDP (actually a bit more than 1.5 percent), but the impact of the reduced loan repayments will actually be felt over the next forty years.

According to an analysis from the Congressional Budget Office (CBO), the cost of forgiveness peaks at a bit more than 0.09 percent of GDP in the years 2023-25. That is less than one-thirtieth of the size of the military budget. It falls to around 0.07 percent of GDP by 2032 and then drops further to 0.02 percent of GDP by 2042.

The peak of 0.09 percent of GDP is less than one-twentieth the figure that Mr. Caldwell gave to readers. As an accounting measure, CBO does list the full $400 billion figure in the year the forgiveness takes place, but its economic impact will be felt over the full period in which students will have lower student loan payments.

It is possible that Caldwell is not familiar with how the economic impact of loan forgiveness would be felt, but it is reasonable to expect that New York Times columnists would have some idea of what they are talking about when they write their columns. Therefore, it qualifies as a “lie” at BTP.

As regular BTP readers know, I constantly harangue news outlets to put really big numbers in context. As these outlets know, none of their readers has any idea of what spending or taxing $2 trillion over a decade means. It is a huge number and if they added or subtracted a zero at the end, it would still be a huge number and probably mean the same thing to the vast majority of their audience.

Therefore, I have always advocated putting these numbers in some context, like a percent of the budget, a percent of GDP, or per person cost. This should require all of about 15 seconds from the reporter doing the piece, and add maybe 15 words to a typical story, but for some reason, the New York Times, Washington Post, National Public Radio, and the rest seem unable to do it.

New York Times columnist Christopher Caldwell got my message but used it to lie to his readers. In a column making a reasonable complaint about presidents abusing “emergency” powers, he tells readers:

“President Biden’s plan [for student loan forgiveness] would forgive a quarter of the roughly $1.6 trillion in federal student debt held by some 43 million Americans — about $400 billion, or roughly 2 percent of gross domestic product.”

The lie in this sentence is the reference to 2 percent of GDP. The $400 billion figure is roughly 2.0 percent of this year’s GDP (actually a bit more than 1.5 percent), but the impact of the reduced loan repayments will actually be felt over the next forty years.

According to an analysis from the Congressional Budget Office (CBO), the cost of forgiveness peaks at a bit more than 0.09 percent of GDP in the years 2023-25. That is less than one-thirtieth of the size of the military budget. It falls to around 0.07 percent of GDP by 2032 and then drops further to 0.02 percent of GDP by 2042.

The peak of 0.09 percent of GDP is less than one-twentieth the figure that Mr. Caldwell gave to readers. As an accounting measure, CBO does list the full $400 billion figure in the year the forgiveness takes place, but its economic impact will be felt over the full period in which students will have lower student loan payments.

It is possible that Caldwell is not familiar with how the economic impact of loan forgiveness would be felt, but it is reasonable to expect that New York Times columnists would have some idea of what they are talking about when they write their columns. Therefore, it qualifies as a “lie” at BTP.

Read More Leer más Join the discussion Participa en la discusión

The Biden administration is getting a lot of grief over its proposal to tax share buybacks at a 4.0 percent rate. They are being denounced as economic illiterates, and worse. I’m going to side with the economic illiterates, and say Biden is very much on the mark with this proposal.

To be clear, I have written before that I don’t agree with most of the complaints directed against buybacks. It makes little difference as a practical matter whether companies pay out money to shareholders as buybacks or dividends.

The one area where there is a clear difference is the tax treatment, but even here the case is overstated. Most people who hold stock have it in 401(k)s or other retirement accounts. For those of us in this group, it doesn’t make an iota of difference whether money is paid out as dividends or buybacks.

When we withdraw money after retiring, it will be taxed as ordinary income, regardless of whether the accumulation was due to rising share prices or dividends. (The same story applies to Roth IRAs, where the payout is tax free in both cases, since the money was taxed going in.)

This point is actually worth emphasizing for a moment, since politicians (mostly Republican politicians) often lie about it. When they claim to be helping middle class stockholders by reducing the capital gains tax, this is largely a lie. Few middle-class people own much stock outside of their retirement accounts. Since lowering the capital gains tax has no impact on the tax paid on retirement accounts, cuts in the capital gains tax will affect few middle-income people.

There is the issue of taxes on stock held outside of retirement account. Share buybacks have the advantage to these shareholders that they can defer the taxes on their gains to when they choose to sell their stock, whereas the tax on dividends is paid in the year the year dividend is paid.

But even here the impact can be overstated. Most people cannot afford to hold stock forever. Maybe they will sell it a year or two down the road, and at that point they will pay the tax. (Those of us who want financial transactions taxes, in part to reduce the rate at which stocks turn over, can’t also complain about stock being held forever.)

Of course, we do have some very rich families, the Waltons have volunteered to be the poster children, who have tens of billions in stock that they literally can hold forever. For these families, having companies pay out profits as buybacks rather than dividends does make a difference.

Insofar as the Biden tax proposal encourages companies to shift more of their payouts to dividends, this is a good thing. We will effectively be raising the tax rate on the very rich.

FWIW, I don’t accept the idea that companies are foregoing good investment opportunities by buying back shares. I’m generally inclined to think that companies invest where they see profitable opportunities. I really don’t want to encourage them to throw money away on silly projects. Do we want Elon Musk to have more money to spend on his Boring Company, which has mostly dug lots of holes to nowhere?

To my view, the great virtue of Biden’s proposed tax on share buybacks is that it is a way to raise the corporate income tax, taking back part of the cut that Trump gave the corporations in 2017. For whatever reason, Biden was able to get people like senators Joe Manchin and Kyrsten Sinema, who would not go along with raising the corporate income tax, to sign on to a tax on share buybacks. I won’t try to explain their thinking, but if this is how we get to raise the corporate income tax, do it. And, if we can make it 4.0 percent rather than the current 1.0 percent, that’s even better.

I’m going to confess to an ulterior motive here. I have argued for switching the basis for the corporate income tax from profits to returns to shareholders (capital gains and dividends). The logic is that we don’t see corporate profits directly, corporate accountants tell us what their companies’ profits were. This provides enormous opportunity and incentive for tax gaming. Enormous resources are wasted in this process and we collect far less in taxes from corporations as a result.

By contrast, returns to shareholders are completely transparent. We can get the data on the increase market capitalization and annual dividend payouts from dozens of financial websites. This would make it possible to calculate the tax liability of all publicly traded companies on a single spreadsheet (that is all companies’ taxes could be calculated on the same spreadsheet). (Privately traded companies pose a problem, but we can worry about that later.)

Anyhow, I have long been a big fan of establishing facts on the ground. We can spend forever arguing over what is best in theory, but when we see something in practice, it is harder to argue over.

I am quite confident that the tax on share buybacks will be just about the most efficient tax in history, in the sense that the amount of money spent to enforce it will be trivial compared to the revenue collected. After all, if Apple spent $25 billion on share buybacks last year, it owes the government $250 million at the 1.0 percent tax rate. What is there to argue over? Is Apple going to say that all those press reports of share buybacks were lies?

This will be true for every company. They have to publicly disclose their share buybacks. Once this is done, we know how much tax they owe: full stop.

If the public sees this, then maybe we can get policy types to get a little bit interested in designing a corporate income tax that we can actually collect. And, in the process, we can put the tax gaming business out of business.

Let’s hear it for Dark Brandon!

The Biden administration is getting a lot of grief over its proposal to tax share buybacks at a 4.0 percent rate. They are being denounced as economic illiterates, and worse. I’m going to side with the economic illiterates, and say Biden is very much on the mark with this proposal.

To be clear, I have written before that I don’t agree with most of the complaints directed against buybacks. It makes little difference as a practical matter whether companies pay out money to shareholders as buybacks or dividends.

The one area where there is a clear difference is the tax treatment, but even here the case is overstated. Most people who hold stock have it in 401(k)s or other retirement accounts. For those of us in this group, it doesn’t make an iota of difference whether money is paid out as dividends or buybacks.

When we withdraw money after retiring, it will be taxed as ordinary income, regardless of whether the accumulation was due to rising share prices or dividends. (The same story applies to Roth IRAs, where the payout is tax free in both cases, since the money was taxed going in.)

This point is actually worth emphasizing for a moment, since politicians (mostly Republican politicians) often lie about it. When they claim to be helping middle class stockholders by reducing the capital gains tax, this is largely a lie. Few middle-class people own much stock outside of their retirement accounts. Since lowering the capital gains tax has no impact on the tax paid on retirement accounts, cuts in the capital gains tax will affect few middle-income people.

There is the issue of taxes on stock held outside of retirement account. Share buybacks have the advantage to these shareholders that they can defer the taxes on their gains to when they choose to sell their stock, whereas the tax on dividends is paid in the year the year dividend is paid.

But even here the impact can be overstated. Most people cannot afford to hold stock forever. Maybe they will sell it a year or two down the road, and at that point they will pay the tax. (Those of us who want financial transactions taxes, in part to reduce the rate at which stocks turn over, can’t also complain about stock being held forever.)

Of course, we do have some very rich families, the Waltons have volunteered to be the poster children, who have tens of billions in stock that they literally can hold forever. For these families, having companies pay out profits as buybacks rather than dividends does make a difference.

Insofar as the Biden tax proposal encourages companies to shift more of their payouts to dividends, this is a good thing. We will effectively be raising the tax rate on the very rich.

FWIW, I don’t accept the idea that companies are foregoing good investment opportunities by buying back shares. I’m generally inclined to think that companies invest where they see profitable opportunities. I really don’t want to encourage them to throw money away on silly projects. Do we want Elon Musk to have more money to spend on his Boring Company, which has mostly dug lots of holes to nowhere?

To my view, the great virtue of Biden’s proposed tax on share buybacks is that it is a way to raise the corporate income tax, taking back part of the cut that Trump gave the corporations in 2017. For whatever reason, Biden was able to get people like senators Joe Manchin and Kyrsten Sinema, who would not go along with raising the corporate income tax, to sign on to a tax on share buybacks. I won’t try to explain their thinking, but if this is how we get to raise the corporate income tax, do it. And, if we can make it 4.0 percent rather than the current 1.0 percent, that’s even better.

I’m going to confess to an ulterior motive here. I have argued for switching the basis for the corporate income tax from profits to returns to shareholders (capital gains and dividends). The logic is that we don’t see corporate profits directly, corporate accountants tell us what their companies’ profits were. This provides enormous opportunity and incentive for tax gaming. Enormous resources are wasted in this process and we collect far less in taxes from corporations as a result.

By contrast, returns to shareholders are completely transparent. We can get the data on the increase market capitalization and annual dividend payouts from dozens of financial websites. This would make it possible to calculate the tax liability of all publicly traded companies on a single spreadsheet (that is all companies’ taxes could be calculated on the same spreadsheet). (Privately traded companies pose a problem, but we can worry about that later.)

Anyhow, I have long been a big fan of establishing facts on the ground. We can spend forever arguing over what is best in theory, but when we see something in practice, it is harder to argue over.

I am quite confident that the tax on share buybacks will be just about the most efficient tax in history, in the sense that the amount of money spent to enforce it will be trivial compared to the revenue collected. After all, if Apple spent $25 billion on share buybacks last year, it owes the government $250 million at the 1.0 percent tax rate. What is there to argue over? Is Apple going to say that all those press reports of share buybacks were lies?

This will be true for every company. They have to publicly disclose their share buybacks. Once this is done, we know how much tax they owe: full stop.

If the public sees this, then maybe we can get policy types to get a little bit interested in designing a corporate income tax that we can actually collect. And, in the process, we can put the tax gaming business out of business.

Let’s hear it for Dark Brandon!

Read More Leer más Join the discussion Participa en la discusión

Like much of the rest of the media, NPR is determined to convince the public that the economy is terrible under President Biden, regardless of what the data show. In Real World Land, there are lots of good things about this economy.

We have the lowest unemployment rate in a half century. Real wages for workers at the bottom end of the income distribution are rising rapidly (that means wages are rising faster than prices). Workers have unprecedented freedom to quit jobs they don’t like. Tens of millions of homeowners are saving thousands of dollars a year in interest expenses as a result of refinancing their mortgages. And tens of millions of workers are saving thousands a year in commuting costs, as well as hundreds of hours in commuting time, as a result of the explosion in work from home since the pandemic.

But the media don’t want to let reality get in the way of their terrible economy story. Therefore, they highlight or invent bad things to say about the economy.

In pushing the bad economy line, they take advantage of the obvious fact that tens of millions of families are struggling in this economy, as is always true in the United States. The point here is that we have a terribly weak welfare state.

This means that even in the best economy, say the year 2000, which was the peak of the late 1990s boom, we still have tens of millions of people struggling to pay the rent, put food on the table, or pay for their kids’ child care. As a result, a reporter who wants to tell people the economy is terrible will never have any problem finding people in terrible straits to support the case.

However, the issue is that they are choosing to do this in a big way now that President Biden is office. They had even more opportunities to find people in bad straits when Donald Trump was in the White House, but they instead largely chose to tell a good economy story.

Anyhow, NPR got into the fray yesterday with a piece telling us how credit card debt is soaring. They found a family who does appear to be in very bad straits and has run up large amounts of credit card debt.

The women highlighted in the piece earns $40,000 a year and has three young children to support. Her major financial problem seems to stem from a divorce. Presumably, she had the income of a second worker to help support the family previously, and possibly also help with child care. She cities paying child care as her biggest problem. This would be a nonissue in the many countries with free or low-cost child care.

The ostensible reason for the story is the rise in credit card debt, which NPR tells us is due to the fact that households can no longer make ends meet. The family they profile is in this situation.

While many struggling families are undoubtedly turning to credit cards to cover their bills, there is another obvious explanation for the recent jump in credit card debt: mortgage refinancing has fallen through the floor.

In 2020 and 2021, there was a massive surge in mortgage refinancing as people took advantage of extraordinarily low interest rates. More than 20 million households refinanced their mortgages, often reducing their interest rate by a percentage point or more, which translated into savings of thousands of dollars a year on interest payments.

When people refinance a mortgage, it is common for them to borrow more than the outstanding amount on their prior loan in order to get money to pay for extraordinary expenses, like remodeling their home, buying a car, or possibly to just have some cash available. The jump in mortgage interest rates following the Fed’s rate hikes have eliminated this option. Under such circumstances, it is hardly surprising that people would turn to other sources of credit, like credit card debt.

This has led to a big increase in credit card debt over the last year. Is this a crisis? Here’s the relationship between credit card debt (revolving credit is overwhelmingly credit card debt) to personal income over the last half century.[1]

As can be seen, there is a jump in the ratio of credit card debt to personal income, but we are still not back to the pre-pandemic level. We are far below the ratios we saw during the housing bubble at the start of the century, and even below the level we saw in the late 1990s boom.

In short, it is hard to see a crisis here. That could change, of course. If we get the recession and jump in unemployment that many are rooting for, the ratio of credit card and other debt to income will surely rise. The media will then have cause for talking about a bad economy, but they don’t now. This is their invention, not the real world.

[1] I used personal income rather than disposable income, which is more common. The reason is that there has been a big increase in tax payments over the last year, as people were paying capital gains tax on stock they had sold at a gain. This lowers measured disposable income (income minus taxes) but does not correspond to people actually having less money, since they sold stocks at a gain.

Like much of the rest of the media, NPR is determined to convince the public that the economy is terrible under President Biden, regardless of what the data show. In Real World Land, there are lots of good things about this economy.

We have the lowest unemployment rate in a half century. Real wages for workers at the bottom end of the income distribution are rising rapidly (that means wages are rising faster than prices). Workers have unprecedented freedom to quit jobs they don’t like. Tens of millions of homeowners are saving thousands of dollars a year in interest expenses as a result of refinancing their mortgages. And tens of millions of workers are saving thousands a year in commuting costs, as well as hundreds of hours in commuting time, as a result of the explosion in work from home since the pandemic.

But the media don’t want to let reality get in the way of their terrible economy story. Therefore, they highlight or invent bad things to say about the economy.

In pushing the bad economy line, they take advantage of the obvious fact that tens of millions of families are struggling in this economy, as is always true in the United States. The point here is that we have a terribly weak welfare state.

This means that even in the best economy, say the year 2000, which was the peak of the late 1990s boom, we still have tens of millions of people struggling to pay the rent, put food on the table, or pay for their kids’ child care. As a result, a reporter who wants to tell people the economy is terrible will never have any problem finding people in terrible straits to support the case.

However, the issue is that they are choosing to do this in a big way now that President Biden is office. They had even more opportunities to find people in bad straits when Donald Trump was in the White House, but they instead largely chose to tell a good economy story.

Anyhow, NPR got into the fray yesterday with a piece telling us how credit card debt is soaring. They found a family who does appear to be in very bad straits and has run up large amounts of credit card debt.

The women highlighted in the piece earns $40,000 a year and has three young children to support. Her major financial problem seems to stem from a divorce. Presumably, she had the income of a second worker to help support the family previously, and possibly also help with child care. She cities paying child care as her biggest problem. This would be a nonissue in the many countries with free or low-cost child care.

The ostensible reason for the story is the rise in credit card debt, which NPR tells us is due to the fact that households can no longer make ends meet. The family they profile is in this situation.

While many struggling families are undoubtedly turning to credit cards to cover their bills, there is another obvious explanation for the recent jump in credit card debt: mortgage refinancing has fallen through the floor.

In 2020 and 2021, there was a massive surge in mortgage refinancing as people took advantage of extraordinarily low interest rates. More than 20 million households refinanced their mortgages, often reducing their interest rate by a percentage point or more, which translated into savings of thousands of dollars a year on interest payments.

When people refinance a mortgage, it is common for them to borrow more than the outstanding amount on their prior loan in order to get money to pay for extraordinary expenses, like remodeling their home, buying a car, or possibly to just have some cash available. The jump in mortgage interest rates following the Fed’s rate hikes have eliminated this option. Under such circumstances, it is hardly surprising that people would turn to other sources of credit, like credit card debt.

This has led to a big increase in credit card debt over the last year. Is this a crisis? Here’s the relationship between credit card debt (revolving credit is overwhelmingly credit card debt) to personal income over the last half century.[1]

As can be seen, there is a jump in the ratio of credit card debt to personal income, but we are still not back to the pre-pandemic level. We are far below the ratios we saw during the housing bubble at the start of the century, and even below the level we saw in the late 1990s boom.

In short, it is hard to see a crisis here. That could change, of course. If we get the recession and jump in unemployment that many are rooting for, the ratio of credit card and other debt to income will surely rise. The media will then have cause for talking about a bad economy, but they don’t now. This is their invention, not the real world.

[1] I used personal income rather than disposable income, which is more common. The reason is that there has been a big increase in tax payments over the last year, as people were paying capital gains tax on stock they had sold at a gain. This lowers measured disposable income (income minus taxes) but does not correspond to people actually having less money, since they sold stocks at a gain.

Read More Leer más Join the discussion Participa en la discusión

• Intellectual PropertyPropiedad IntelectualUnited StatesEE. UU.

The New York Times had a piece reporting on the conditions the Biden administration intends to impose on companies that benefit from the subsidies in the CHIPS Act, which is intended to increase domestic production of advanced semiconductors and related technologies. It noted that one of the conditions is a tax on excess profits, defined as profits in excess of some target specified by the companies getting the subsidies.

This proposed tax seems a recipe for endless legal wrangling. Companies constantly restructure, creating, eliminating, or selling subsidiaries. It will likely be extremely difficult to show that a company actually earned more than they were supposed to from a specific subsidy. In any case, we know this route will create lots of high-paying jobs for tax lawyers and accountants, which is a complete waste from the standpoint of economic efficiency.

A more productive route would be to change the terms of the intellectual property that these companies will be getting due to the subsidies. As it is now, patent monopolies extend for 20 years from the date of issuance.

A condition of getting the subsidy could be that the length of the patent is substantially shorter, say four years. This should give companies plenty of time to take advantage of technology developed through these subsidies, especially since they would enjoy an enormous first-mover advantage that would continue even after their monopolies had expired.

This shorter period should encompass other protections, most notably non-disclosure agreements. Workers who developed the technology could not be prevented from going to competitors or starting their own company for more than four years after the subsidy was received.

While there will still be disputes about what technology was actually developed with the subsidy, this route has two major advantages. First, it provides dividends to the public through lower prices rather than tax revenue. This will mean more take-up of the product. It also should foster further innovation since competitors can quickly build on important breakthroughs rather than bottling them up in a single company.

The other advantage is that the government doesn’t have to play the role of enforcer. If the issue is the patent length that should apply, a company’s competitors are likely to press the case for themselves. If they want to use a technology or hire away key employers, they would look to move forward and force the company to go to court to try to block them.

The threat of legal action can still be an effective deterrent, but with substantial profits at stake, many companies will likely be prepared to take the risk. In any case, this is likely to be a far less bureaucratic process than determining how much a company’s profits exceeded its projected levels.

The New York Times had a piece reporting on the conditions the Biden administration intends to impose on companies that benefit from the subsidies in the CHIPS Act, which is intended to increase domestic production of advanced semiconductors and related technologies. It noted that one of the conditions is a tax on excess profits, defined as profits in excess of some target specified by the companies getting the subsidies.

This proposed tax seems a recipe for endless legal wrangling. Companies constantly restructure, creating, eliminating, or selling subsidiaries. It will likely be extremely difficult to show that a company actually earned more than they were supposed to from a specific subsidy. In any case, we know this route will create lots of high-paying jobs for tax lawyers and accountants, which is a complete waste from the standpoint of economic efficiency.

A more productive route would be to change the terms of the intellectual property that these companies will be getting due to the subsidies. As it is now, patent monopolies extend for 20 years from the date of issuance.

A condition of getting the subsidy could be that the length of the patent is substantially shorter, say four years. This should give companies plenty of time to take advantage of technology developed through these subsidies, especially since they would enjoy an enormous first-mover advantage that would continue even after their monopolies had expired.

This shorter period should encompass other protections, most notably non-disclosure agreements. Workers who developed the technology could not be prevented from going to competitors or starting their own company for more than four years after the subsidy was received.

While there will still be disputes about what technology was actually developed with the subsidy, this route has two major advantages. First, it provides dividends to the public through lower prices rather than tax revenue. This will mean more take-up of the product. It also should foster further innovation since competitors can quickly build on important breakthroughs rather than bottling them up in a single company.

The other advantage is that the government doesn’t have to play the role of enforcer. If the issue is the patent length that should apply, a company’s competitors are likely to press the case for themselves. If they want to use a technology or hire away key employers, they would look to move forward and force the company to go to court to try to block them.

The threat of legal action can still be an effective deterrent, but with substantial profits at stake, many companies will likely be prepared to take the risk. In any case, this is likely to be a far less bureaucratic process than determining how much a company’s profits exceeded its projected levels.

Read More Leer más Join the discussion Participa en la discusión

Many people who should know better have been saying silly things about households running down their savings and being forced to cut back consumption. The problem with these sorts of comments is that savings in our national income accounts have little to do with how most of us think about savings in our lives. Less of the former does not necessarily mean that people will have less money to buy things.

Before going into the specifics, let me just make a point to orient people. Saving in the national income accounts is almost entirely a story of the top half of the income distribution, and largely the top 10 percent.

I recognize that there are tens of millions of people who are struggling to get by, and in many cases not getting by. These people are either not saving at all or, insofar as they are, it has a minimal impact on aggregate saving numbers. The saving rate is not about their story.

Aggregate saving is about the people who have the money and the choice of whether to spend it or not. That is not a good picture, it would be great if we had a far more equal distribution of income so that most people did have the option to save, but we don’t. In an economy where the richest 10 percent of households get more than 40 percent of income, aggregate savings is the story of what these people are doing with their money.

Saving by Burning Money

The key point in this story is the definition of savings in the national income accounts. Savings is simply disposable income (income minus taxes) that is not spent on consumption. From the standpoint of the national income accounts, it doesn’t matter what you did with the money that you didn’t spend on consumption. As long as you didn’t spend it on the consumption of a newly produced good or service, it is treated as being saved.

Savings includes all of the things people typically do with their money that we would think of as saving. So, putting money in the bank counts as saving, as does buying a government bond. Buying shares of stock or a plot of land would also count as saving. We may colloquially describe these purchases as “investment” but we are not buying a newly produced good or service, we are just trading assets (cash for shares of stock or a deed to land), so these purchases do not count as investment in the national income accounts.

People may also save in ways that they don’t think of as saving. If they cashed their paycheck and put a few hundred dollars aside to buy a television or some other appliance, but didn’t get around to doing it, then they have saved this money from the standpoint of the national income accounts.

The same would be the case if they pulled a few hundred dollars out of the bank that they intended to spend but somehow lost the money. If the money remains lost, it is saved from a national accounting standpoint.

This is even true if they deliberately destroyed the money. If someone cashes their paycheck and then burns $1,000 to protest George Santos being in Congress, this will be treated as savings in the national income accounts. They did not buy a newly produced good or service.

Capital Gains are Not Income, Therefore They Don’t Increase Savings

If saving is defined as income that is not spent on a newly produced good or service, then we also need a definition of income. Income in the national income accounts is money generated from services provided in the current year. Most obviously, this would be the wages people get from working. It would also be rent paid on land or housing. It also would include interest and dividends paid on bonds or shares of stock.

However, the capital gains on stock do not count as income. (The same applies to capital gains on houses.) The idea here is that stock prices fluctuate month to month and year to year. If we envision a situation where we had the exact same stock of capital on January 1, 2023, as we did on January 1, 2022, and the same labor force, but the value of the market was 10 percent greater (roughly $4 trillion), there would be no asset (tangible or intangible) that corresponds to this $4 trillion increase in value. Therefore, it does not count as income.

If that sounds strange, consider the opposite situation where the market falls by 10 percent over the course of a year. Would it make sense to deduct $4 trillion from national income as a result?

This is important in the current context because many people sold stock after the large pandemic run-up in the market, and have substantial capital gains as a result. Suppose that a household has a normal income of $200,000 from wages. (Yes, this is a rich household.) If they sold stock last year for $300,000, with a capital gain of $100,000, they would have lots of money in the bank.

However, from the standpoint of the national income accounts, their income is still just $200,000. If their consumption was unchanged, then their measured saving would be the same in the year they realized these capital gains as it had been before.

Actually, the situation is somewhat worse than this. They are supposed to pay capital gains tax on this money. If they pay capital gains tax at the 20 percent rate, then they will pay an additional $20,000 in income taxes as a result of their capital gains.[1] This would reduce their disposable income, which is defined as income, minus taxes.

If their consumption is unchanged, their savings would be $20,000 lower because their after-tax income is $20,000 lower. For the country as a whole, if we have a large sell-off of stock after a big run-up, we will see an increase in taxes, which will mean a lower saving rate, other things equal. We did in fact see a big jump in tax payments in 2022, which explains most but not all, of the drop in savings last year. (The saving rate rose in January, despite the big jump in consumption, due to a sharp drop in tax payments.)

The other part of the story is that households may increase their consumption based on their capital gains. If they used some of their gains to remodel their house, buy a new car, or take a vacation, this would mean they have increased their consumption and reduced their savings. Undoubtedly, this is part of the story of the decline in savings reported for 2022.

This is not sustainable in the sense that we would not expect households will have large amounts of capital gains to draw on every year. But this is not a story of households drawing down their savings in any meaningful sense. If the household with the $100,000 gain, spent on extra $20,000 on one-time expenditures, after paying an extra $20,000 in capital gains taxes, their reported savings would be $40,000 lower than in the prior year, but they would still have $260,000 in the bank from selling their stock. This is to a large extent the story of the decline in the saving rate that we saw in 2022.

Dividends and Share Buybacks: An Inconsistency in the National Income Accounts

While households cannot anticipate large capital gains every year, corporate share buybacks is one case where this view would be wrong. The basic story is that share buybacks are a way for companies to give out money to shareholders as an alternative to paying dividends. Buybacks are desirable from the standpoint of shareholders since the money paid out is not immediately subject to taxes, as is the case with dividends. Shareholders will only pay taxes when they sell the stock at a gain.

This situation leads to an inconsistency in the national income accounts. Suppose corporations pay out $200 billion in dividends to shareholders. This money counts as income for shareholders and as an expense for the companies, which reduces their profits and corporate savings.

However, if they instead pay out this $200 billion by buying back shares, this money is not treated as income for shareholders. That is true even if the shareholders immediately sell their stock and take advantage of the higher prices resulting from the buybacks. From the companies’ standpoint, this $200 billion in buybacks does not count as an expense and reduce their profits. Instead, it is treated as though they purchased an asset (their own stock), just as if they had bought land or shares in another company.

This matters when we look at household saving rates since companies can in fact indefinitely pay out the money that would otherwise go to dividends, in the form of share buybacks. For consistency, we really should count this money as part of household income. This would raise disposable income and therefore increase savings.

The Whole Picture

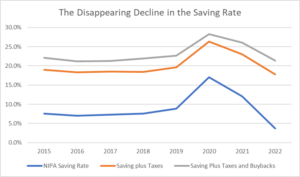

The figure below shows the reported saving rate from the national income accounts from 2015 to 2023. It also shows the ratio of saving, plus taxes, to total income in the years since 2015. While the Trump tax cut did change this relationship in 2017 and 2018, since 2019 we have had no major changes to the tax code. That means that changes in the relationship between tax collections and income were driven mostly by changes in household income, most notably capital gains income. (There were timing issues associated with the pandemic, but using annual data eliminates most of this effect.)

The third line uses a measure of savings if we count share buybacks as part of personal income. This adds dollar to dollar to savings, since its inclusion does not affect consumption. It also raises income (the denominator), since we have to add share buybacks to the measure of personal income in the National Accounts.

Source: BEA, S&P, and author’s calculations.

As can be seen, including personal taxes (Table 2.1, Line 6) eliminates most of the drop in saving reported for 2023. While the official saving rate shows a drop of 3.6 percentage points from the average for the four years prior to the pandemic to 2023 (7.3 percent to 3.7 percent), using the combined taxes plus savings measure the drop is just 0.7 percentage points (18.6 percent to 17.9 percent). Calculating a saving rate that includes share buybacks as income, there is a drop of just 0.3 percentage points (21.7 percent to 21.4 percent).

In short, if we use measures of saving that are more consistent with both what households actually see, and economic logic, there is very little to the idea that the saving rate is falling through the floor. The plunging saving rate is almost entirely an illusion caused by the failure to think about the issue clearly.

[1] Much of these gains would in fact be taxed at a rate lower than 20 percent for a family earning $200k.

Many people who should know better have been saying silly things about households running down their savings and being forced to cut back consumption. The problem with these sorts of comments is that savings in our national income accounts have little to do with how most of us think about savings in our lives. Less of the former does not necessarily mean that people will have less money to buy things.

Before going into the specifics, let me just make a point to orient people. Saving in the national income accounts is almost entirely a story of the top half of the income distribution, and largely the top 10 percent.

I recognize that there are tens of millions of people who are struggling to get by, and in many cases not getting by. These people are either not saving at all or, insofar as they are, it has a minimal impact on aggregate saving numbers. The saving rate is not about their story.

Aggregate saving is about the people who have the money and the choice of whether to spend it or not. That is not a good picture, it would be great if we had a far more equal distribution of income so that most people did have the option to save, but we don’t. In an economy where the richest 10 percent of households get more than 40 percent of income, aggregate savings is the story of what these people are doing with their money.

Saving by Burning Money

The key point in this story is the definition of savings in the national income accounts. Savings is simply disposable income (income minus taxes) that is not spent on consumption. From the standpoint of the national income accounts, it doesn’t matter what you did with the money that you didn’t spend on consumption. As long as you didn’t spend it on the consumption of a newly produced good or service, it is treated as being saved.

Savings includes all of the things people typically do with their money that we would think of as saving. So, putting money in the bank counts as saving, as does buying a government bond. Buying shares of stock or a plot of land would also count as saving. We may colloquially describe these purchases as “investment” but we are not buying a newly produced good or service, we are just trading assets (cash for shares of stock or a deed to land), so these purchases do not count as investment in the national income accounts.

People may also save in ways that they don’t think of as saving. If they cashed their paycheck and put a few hundred dollars aside to buy a television or some other appliance, but didn’t get around to doing it, then they have saved this money from the standpoint of the national income accounts.

The same would be the case if they pulled a few hundred dollars out of the bank that they intended to spend but somehow lost the money. If the money remains lost, it is saved from a national accounting standpoint.

This is even true if they deliberately destroyed the money. If someone cashes their paycheck and then burns $1,000 to protest George Santos being in Congress, this will be treated as savings in the national income accounts. They did not buy a newly produced good or service.

Capital Gains are Not Income, Therefore They Don’t Increase Savings

If saving is defined as income that is not spent on a newly produced good or service, then we also need a definition of income. Income in the national income accounts is money generated from services provided in the current year. Most obviously, this would be the wages people get from working. It would also be rent paid on land or housing. It also would include interest and dividends paid on bonds or shares of stock.

However, the capital gains on stock do not count as income. (The same applies to capital gains on houses.) The idea here is that stock prices fluctuate month to month and year to year. If we envision a situation where we had the exact same stock of capital on January 1, 2023, as we did on January 1, 2022, and the same labor force, but the value of the market was 10 percent greater (roughly $4 trillion), there would be no asset (tangible or intangible) that corresponds to this $4 trillion increase in value. Therefore, it does not count as income.

If that sounds strange, consider the opposite situation where the market falls by 10 percent over the course of a year. Would it make sense to deduct $4 trillion from national income as a result?

This is important in the current context because many people sold stock after the large pandemic run-up in the market, and have substantial capital gains as a result. Suppose that a household has a normal income of $200,000 from wages. (Yes, this is a rich household.) If they sold stock last year for $300,000, with a capital gain of $100,000, they would have lots of money in the bank.

However, from the standpoint of the national income accounts, their income is still just $200,000. If their consumption was unchanged, then their measured saving would be the same in the year they realized these capital gains as it had been before.

Actually, the situation is somewhat worse than this. They are supposed to pay capital gains tax on this money. If they pay capital gains tax at the 20 percent rate, then they will pay an additional $20,000 in income taxes as a result of their capital gains.[1] This would reduce their disposable income, which is defined as income, minus taxes.

If their consumption is unchanged, their savings would be $20,000 lower because their after-tax income is $20,000 lower. For the country as a whole, if we have a large sell-off of stock after a big run-up, we will see an increase in taxes, which will mean a lower saving rate, other things equal. We did in fact see a big jump in tax payments in 2022, which explains most but not all, of the drop in savings last year. (The saving rate rose in January, despite the big jump in consumption, due to a sharp drop in tax payments.)

The other part of the story is that households may increase their consumption based on their capital gains. If they used some of their gains to remodel their house, buy a new car, or take a vacation, this would mean they have increased their consumption and reduced their savings. Undoubtedly, this is part of the story of the decline in savings reported for 2022.

This is not sustainable in the sense that we would not expect households will have large amounts of capital gains to draw on every year. But this is not a story of households drawing down their savings in any meaningful sense. If the household with the $100,000 gain, spent on extra $20,000 on one-time expenditures, after paying an extra $20,000 in capital gains taxes, their reported savings would be $40,000 lower than in the prior year, but they would still have $260,000 in the bank from selling their stock. This is to a large extent the story of the decline in the saving rate that we saw in 2022.

Dividends and Share Buybacks: An Inconsistency in the National Income Accounts

While households cannot anticipate large capital gains every year, corporate share buybacks is one case where this view would be wrong. The basic story is that share buybacks are a way for companies to give out money to shareholders as an alternative to paying dividends. Buybacks are desirable from the standpoint of shareholders since the money paid out is not immediately subject to taxes, as is the case with dividends. Shareholders will only pay taxes when they sell the stock at a gain.

This situation leads to an inconsistency in the national income accounts. Suppose corporations pay out $200 billion in dividends to shareholders. This money counts as income for shareholders and as an expense for the companies, which reduces their profits and corporate savings.

However, if they instead pay out this $200 billion by buying back shares, this money is not treated as income for shareholders. That is true even if the shareholders immediately sell their stock and take advantage of the higher prices resulting from the buybacks. From the companies’ standpoint, this $200 billion in buybacks does not count as an expense and reduce their profits. Instead, it is treated as though they purchased an asset (their own stock), just as if they had bought land or shares in another company.

This matters when we look at household saving rates since companies can in fact indefinitely pay out the money that would otherwise go to dividends, in the form of share buybacks. For consistency, we really should count this money as part of household income. This would raise disposable income and therefore increase savings.

The Whole Picture

The figure below shows the reported saving rate from the national income accounts from 2015 to 2023. It also shows the ratio of saving, plus taxes, to total income in the years since 2015. While the Trump tax cut did change this relationship in 2017 and 2018, since 2019 we have had no major changes to the tax code. That means that changes in the relationship between tax collections and income were driven mostly by changes in household income, most notably capital gains income. (There were timing issues associated with the pandemic, but using annual data eliminates most of this effect.)

The third line uses a measure of savings if we count share buybacks as part of personal income. This adds dollar to dollar to savings, since its inclusion does not affect consumption. It also raises income (the denominator), since we have to add share buybacks to the measure of personal income in the National Accounts.

Source: BEA, S&P, and author’s calculations.

As can be seen, including personal taxes (Table 2.1, Line 6) eliminates most of the drop in saving reported for 2023. While the official saving rate shows a drop of 3.6 percentage points from the average for the four years prior to the pandemic to 2023 (7.3 percent to 3.7 percent), using the combined taxes plus savings measure the drop is just 0.7 percentage points (18.6 percent to 17.9 percent). Calculating a saving rate that includes share buybacks as income, there is a drop of just 0.3 percentage points (21.7 percent to 21.4 percent).

In short, if we use measures of saving that are more consistent with both what households actually see, and economic logic, there is very little to the idea that the saving rate is falling through the floor. The plunging saving rate is almost entirely an illusion caused by the failure to think about the issue clearly.

[1] Much of these gains would in fact be taxed at a rate lower than 20 percent for a family earning $200k.

Read More Leer más Join the discussion Participa en la discusión

The January data on consumer expenditures released yesterday had many people freaking out. The story is that the Fed is going to have to get out the big guns to really shoot inflation down.

For those of us hoping that inflation would come down, without a big jump in unemployment, the report was definitely bad news. It showed strong growth in consumption, and more troubling, a 0.6 monthly increase in both the overall Personal Consumption Expenditure Deflator (PCE) and the core.

Many of us had expected a modest uptick from December’s 0.4 percent core, but the 0.2 percentage point jump was definitely disconcerting. So, the story in yesterday’s data was definitely bad news from the standpoint of moderating inflation, but we have to remember the fourteenth commandment, never make too much of a single month’s data.[1]

How Bad Is It?

First, on the demand side, the answer is pretty straightforward. As I noted when the January retail sales were released, the January jump was making up for declines reported in November and December. A 1.8 percent single month’s jump in consumption expenditures (1.1 percent real) sure looks like a big deal. But, if we take the increase over the last three months it is not much to get excited about.

The annual growth rate in nominal sales from October to January was 6.0 percent. If we take my preferred measure, comparing the last three months (November, December, and January) with the prior three months (August, September, and October), the nominal growth rate was just 4.2 percent. The corresponding growth rates in real consumption expenditures are 1.9 percent for October through January and 0.6 percent for the average of the last three months compared with the prior three months. It would be difficult to argue that these growth rates are unsustainable.

There is a question as to why we saw this quirky pattern, with very weak numbers in November and December, followed by an extraordinarily strong number in January. Part of the story is likely problems with seasonal adjustments. If people move their holiday purchases forward, say into October, then the seasonal adjustments would make November and December look weaker than they really are. This would also imply some automatic bounce back in the January data since the December sales had been understated.

It is also possible that January really was very strong, as we had better than normal weather in much of the country. That could have led people to do more shopping and buy more items than they would have if we had seen a typical January with snow storms and cold weather in the Midwest and Northeast. (That could also help explain the big jump in employment reported for the month.)

In either case, there is little basis in the January data for thinking that consumption is increasing at an unsustainable pace. If we see strong growth again in February, then we would have to reassess this view, but the January data taken in the context of prior months does not provide much reason for thinking that consumption is growing especially fast.

What About Prices?

If the reported surge in consumption can be easily dismissed, that is not true with the price data reported for January. Inflation looked to be clearly slowing through the fall, then we saw a 0.4 percent rise in the core rate in the PCE in December, followed by this 0.6 percent jump. That gave us a 4.7 percent annualized increase over the last three months and a slightly better 4.1 percent rate taking the average of the last three months compared with the prior three months. This is still down considerably from the peaks hit in the first half of 2022, but the downward trend is far less clear.

The reversal is partly due to new seasonal adjustment factors which now show higher inflation rates for the fall months than what had previously been reported. This makes inflation in recent months look worse, but does have the offsetting benefit that the seasonal adjustments will tend to lower inflation more in the months ahead. Still, if we are mistaken about the downward trend, seasonal adjustments will not give us one.

Comparing the 0.6 percent increase in the core in January with the relatively modest 0.2 percent rise in November, there are large differences in most components. For simplicity, we can divide the core into three main areas, rent, core goods, and services.

The Certain Decline in Rental Inflation

The story with rent is the simplest. The rent proper component rose 0.74 percent in January, down slightly from its 0.77 percent rise in November. Owners’ equivalent rent edged up very slightly from a 0.66 percent increase in November to a 0.67 percent increase in January. Clearly, this is not the story of the more rapid inflation in January.

This rate of rental inflation would be a cause for concern, but we know that it will soon turn sharply lower, based on the much lower rate of rental inflation shown in private indexes of marketed units. Later this year, we will likely be seeing rates of rental inflation that are comparable to or lower than their pre-pandemic pace.

Furthermore, pandemic supply chain problems slowed the construction of new units. There are now more units, especially in apartment buildings, under construction than when the Fed began raising rates last March. As these units get completed, it should put further downward pressure on rents.

For these reasons, we can be confident that rent will not be a major contributor to inflation later this year. That is a big deal since it accounts for most of the 40 percent of the core CPI and just under 17 percent of the core PCE deflator. If rent is not pushing inflation higher, and quite possibly pulling it lower, the picture will look considerably better in future months.

The Prospect for Price Declines in Non-Core Goods

The situation with services and core goods is more complex. Prices of the latter were pushed higher in 2021 and the first half of 2022 due to supply chain issues. This was the story of ships backed up at docks, unable to offload their cargo. There was also was a semi-conductor shortage due to a fire at a major factory in Japan, which led to a serious shortage of cars and trucks, sending their prices soaring.

Prices for many of these items had been falling in the summer and fall, but have stabilized or even edged higher in the last couple of months. This raises the question of whether prices have now adjusted to a new post-pandemic normal, or whether we should expect further price declines in the months ahead.

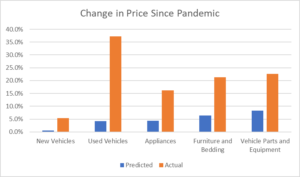

A way to gauge this is to compare pre-pandemic price trends, with where prices are today, adjusting for excess wage growth. I define the latter as the wage growth since the pandemic that exceeds the pace of wage growth for the prior five years.

The average hourly wage increased at a 5.1 percent annual rate in the three years from January 2020 to January 2023, compared to a pre-pandemic trend of 2.8 percent. As a result, wages were 6.9 percent higher last month, on average, than if they had continued at their pre-pandemic pace. The pre-pandemic trend for prices is defined as the rate of price growth in the five years prior to the pandemic.

The figure below shows current price levels for new and used vehicles, appliances, furniture, and vehicle parts. It compares the current price level, using the CPI, with the price level if the pre-pandemic trend had persisted, adding in 6.9 percent to account for the excess wage growth since the start of the pandemic.

Source: Bureau of Labor Statistics and author’s calculations.

As can be seen, in all of these categories the actual price change has far exceeded the one predicted by extrapolating from trends and excess wage growth. (This pattern does not hold for all commodities. For apparel the actual price change since the pandemic was 5.4 percent, compared to the 5.1 percent increase that would be predicted by this formula.) For four of the five categories, the gap is more than 10 percentage points and in the case of used vehicles, it is more than 30 percentage points.

The predicted values are obviously based on a very crude calculation. However, when we are through all the pandemic and Ukraine war-related supply chain issues, we should expect to see the pattern for prices to return to something like their pre-pandemic trend path unless the pandemic permanently altered conditions of production or competition.

The large remaining gap between actual prices and predicted prices suggests that we should still expect substantial future declines in many areas where they were sharp rises in prices during the pandemic. The timing will vary depending on specific conditions in each industry. For example, auto manufacturers are still reporting that shortages of chips and other parts are impeding production. These shortages are much less severe now than last year, but it is not clear when production will be able to return to normal levels.

In other cases, production is likely to close to normal but it is a question of how long it takes for inventories to build up and then place downward pressure on prices. This has already happened in the case of televisions. After rising by 13.2 percent between August 2020 and August 2021, television prices have since fallen back by almost 20 percent and are now well below the pre-pandemic level. With the ratio of non-car inventories to sales now at or above pre-pandemic levels, we should expect further price declines in many commodities in the not-distant future.

Non-Rent Services

Federal Reserve Board Chair Jerome Powell has indicated that he is closely watching the trend in non-core services. These are areas like health care services, transportation services, and restaurants. The story here in the January data is clearly not good.

The price of health care services in the PCE rose 0.26 percent in January, after rising by 0.12 percent in December and just 0.07 percent in November. The price for transportation services rose by 1.05 percent in January, and the index for restaurants rose by 0.64 percent. There is a similar story with most other non-rent services.

However, there are two important reasons not to be too scared by these numbers. The first is that the price increases in services are at least partially driven by increases in goods prices. In the case of transportation, higher fuel prices are a big factor in airline prices. Also, the pandemic-related surge in the price of vehicle parts is a big factor in the price of car repair services. In the same vein, soaring food prices are a big factor in restaurant prices.

If these prices stabilize, and likely turn downward in many cases, the lower costs will be reflected in service prices. That doesn’t mean we may not see a problem of the excessive inflation in non-rent services, but we should recognize that at least part of the inflation we are seeing at present is due to increases in goods prices that will not continue.

The other, more important, issue is that inflation in services should ultimately be consistent with the pace of wage growth we are seeing. This simply means that we should not expect the capital share to either rise or fall indefinitely. And, since we saw a big shift from wages to profits in the pandemic, it would be reasonable to expect some period where the wage share increases at the expense of profits.

The rate of wage growth has fallen considerably over the course of 2022. The Employment Cost Index (ECI) rose at less than a 4.0 percent annual rate in the 4th quarter, down from a 5.8 percent rate in the first quarter. The annual rate of growth in the average hourly earnings (AHE) series for the three months that ended in January was 4.6 percent, down from a peak in this measure of 6.4 percent in January of 2022.

Monthly, and even quarterly data, are erratic, but it is clear that the direction of change is downward. In spite of the low unemployment rate and the high reported rate of job openings, wage growth has been slowing. There is no guarantee this slowing will continue, but there is no doubt about the direction of change over the last year.

The other point is that these rates of wage growth would suggest a slower pace of inflation in services going forward. While the pace of productivity growth is another big question mark, given past patterns, we should assume that inflation in services will be 1.0 to 1.5 percentage points less than the rate of wage growth. This would give us inflation in services of between 2.5 percent and 3.0 percent, based on the ECI, and 3.1 percent and 3.6 percent based on the AHE.

Are We Getting to the Fed’s Target?

Taking these stories together, we may still be looking at inflation somewhat above 2.0 percent through 2023, but it is likely that we will be getting close. If the rate of rental inflation falls to between 2.0-3.0 percent (slightly below the pre-pandemic pace), we see a period of falling non-core goods prices, and we have inflation in non-housing services of nearly 3.0 percent, we would be looking at an overall inflation rate of less than 3.0 percent. Whether we get close enough to 2.0 for the Fed to decide that it has done its job will depend on both the actual inflation rate and how the Fed interprets its 2.0 percent target.

I recognize that I have been consistently optimistic about the inflation picture since the early days of the pandemic recovery, so it is worth questioning my assumptions here. Perhaps the big pandemic price rises in goods will stick, implying a lasting shift to profits in this area. It is also possible that we will be in for a stretch of extraordinarily weak productivity growth in services, which would also mean more inflation. It could also be the case that wage growth will begin to accelerate again.

These are all real possibilities, which along with other factors could lead inflation to come in considerably higher than my calculations here. But, there is at least a plausible scenario that suggests that we will be close to the Fed’s inflation target by the end of 2023, without a big rise in unemployment.

It is indisputable that we have already seen a sharp slowing of inflation and wage growth even as unemployment has fallen to a fifty-year low. It is hard to see how we can rule out the possibility that this trend will continue.

[1] I am happy to say that the Wednesday release of 3rd quarter data from the Quarterly Census on Employment and Wages (QCEW), coupled with yesterday’s release from the Commerce Department, restored my confidence in the establishment survey. Noting the huge gap between job growth as reported in the establishment survey and employment growth in the household survey, I actually considered the possibility that the household survey was closer to the mark. However, the 3rd quarter QCEW hugely outpaced the reported job growth in the establishment survey for the quarter, putting the combined 2nd and 3rd quarter numbers for the two series within spitting distance of each other. The receipts on social insurance taxes reported in yesterday’s release, which come from the Treasury Department, fit closely with the big jump in employment reported in the establishment survey for January. With these important independent data sources looking pretty close to the establishment data, we can be comfortable that it is giving us a reasonably good picture of the labor market.

The January data on consumer expenditures released yesterday had many people freaking out. The story is that the Fed is going to have to get out the big guns to really shoot inflation down.

For those of us hoping that inflation would come down, without a big jump in unemployment, the report was definitely bad news. It showed strong growth in consumption, and more troubling, a 0.6 monthly increase in both the overall Personal Consumption Expenditure Deflator (PCE) and the core.

Many of us had expected a modest uptick from December’s 0.4 percent core, but the 0.2 percentage point jump was definitely disconcerting. So, the story in yesterday’s data was definitely bad news from the standpoint of moderating inflation, but we have to remember the fourteenth commandment, never make too much of a single month’s data.[1]

How Bad Is It?

First, on the demand side, the answer is pretty straightforward. As I noted when the January retail sales were released, the January jump was making up for declines reported in November and December. A 1.8 percent single month’s jump in consumption expenditures (1.1 percent real) sure looks like a big deal. But, if we take the increase over the last three months it is not much to get excited about.

The annual growth rate in nominal sales from October to January was 6.0 percent. If we take my preferred measure, comparing the last three months (November, December, and January) with the prior three months (August, September, and October), the nominal growth rate was just 4.2 percent. The corresponding growth rates in real consumption expenditures are 1.9 percent for October through January and 0.6 percent for the average of the last three months compared with the prior three months. It would be difficult to argue that these growth rates are unsustainable.

There is a question as to why we saw this quirky pattern, with very weak numbers in November and December, followed by an extraordinarily strong number in January. Part of the story is likely problems with seasonal adjustments. If people move their holiday purchases forward, say into October, then the seasonal adjustments would make November and December look weaker than they really are. This would also imply some automatic bounce back in the January data since the December sales had been understated.

It is also possible that January really was very strong, as we had better than normal weather in much of the country. That could have led people to do more shopping and buy more items than they would have if we had seen a typical January with snow storms and cold weather in the Midwest and Northeast. (That could also help explain the big jump in employment reported for the month.)

In either case, there is little basis in the January data for thinking that consumption is increasing at an unsustainable pace. If we see strong growth again in February, then we would have to reassess this view, but the January data taken in the context of prior months does not provide much reason for thinking that consumption is growing especially fast.

What About Prices?