While Elizabeth Warren is praising the European Union’s crackdown on Apple’s Ireland tax scheme, Jack Lew and the Obama Treasury Department are going to bat for corporate tax cheating. Warren is far too optimistic about the prospect of a successful crackdown. These folks are prepared to spend a lot of money to hide their profits from tax authorities and they are likely to find accomplices in many Irelands around the world.

It would be good to look in a different direction. I remain a big fan of my proposal for companies to turn over non-voting shares of stock to the government. In that case, what goes to the shareholders also goes to the government. Unless you cheat your shareholders, you can’t cheat the government.

I know this is probably too simple to be taken seriously in policy circles, but those who care about an efficient and effective way to collect corporate taxes should be thinking about it.

While Elizabeth Warren is praising the European Union’s crackdown on Apple’s Ireland tax scheme, Jack Lew and the Obama Treasury Department are going to bat for corporate tax cheating. Warren is far too optimistic about the prospect of a successful crackdown. These folks are prepared to spend a lot of money to hide their profits from tax authorities and they are likely to find accomplices in many Irelands around the world.

It would be good to look in a different direction. I remain a big fan of my proposal for companies to turn over non-voting shares of stock to the government. In that case, what goes to the shareholders also goes to the government. Unless you cheat your shareholders, you can’t cheat the government.

I know this is probably too simple to be taken seriously in policy circles, but those who care about an efficient and effective way to collect corporate taxes should be thinking about it.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

No one expects NYT columnists to have any knowledge of the topics on which they write, which is a very good thing for David Brooks. In his column belittling the impact of the Affordable Care Act (ACA), he never once mentioned the requirement that insurers charge everyone the same premium, regardless of their health.

Brooks focuses on the health care exchanges, which do in fact have fewer participants than expected. The main reason for the shortfall is not that fewer people are being insured, as Brooks implies, it is rather that fewer employers dropped coverage than expected. (Brooks also repeats the silly “young invincible” story, that the problem is too few young healthy people signing up. The exchanges need healthy people, and it is actually better if they are older healthy people, since older people pay higher premiums.)

Brooks argues that the exchanges are disproportionately drawing lower-income people, which makes them another low-income program, like Medicaid, rather than a universal program like Medicare. Apparently Brooks did not realize that the ACA also requires that all insurers charge patients the same premium regardless of their health condition. This was a huge change in the insurance market since it means that even people with serious health problems, like cancer survivors and people with heart conditions, can get insurance at the same price as anyone else of the same age.

Before the ACA, these people could expect to pay tens of thousands of dollars a year for insurance, if they could get it at all. As a practical matter, this meant that before the ACA most people really didn’t have insurance against serious health conditions. Often these conditions would force a worker to leave their job, which was generally the source of their insurance. Once they left their job, they would then be forced to buy insurance in the individual market where insurers could charge them a premium based on their health condition. The ACA fundamentally changed this situation, but apparently Brooks never noticed.

Note: I wanted to get folks the actual data (bonus points to anyone who can get this info to Brooks before he writes his next column on the topic). In 2012, before the key provisions of the ACA took effect, the Congressional Budget Office (CBO) projected that the uninsured population would fall to 32 million by 2015. In fact, it fell to 32 million by 2014, a year in which it was projected there would still be 38 million uninsured people. According to data from Gallup, the number of uninsured non-elderly fell to less than 28 million by the fourth quarter of 2015.

No one expects NYT columnists to have any knowledge of the topics on which they write, which is a very good thing for David Brooks. In his column belittling the impact of the Affordable Care Act (ACA), he never once mentioned the requirement that insurers charge everyone the same premium, regardless of their health.

Brooks focuses on the health care exchanges, which do in fact have fewer participants than expected. The main reason for the shortfall is not that fewer people are being insured, as Brooks implies, it is rather that fewer employers dropped coverage than expected. (Brooks also repeats the silly “young invincible” story, that the problem is too few young healthy people signing up. The exchanges need healthy people, and it is actually better if they are older healthy people, since older people pay higher premiums.)

Brooks argues that the exchanges are disproportionately drawing lower-income people, which makes them another low-income program, like Medicaid, rather than a universal program like Medicare. Apparently Brooks did not realize that the ACA also requires that all insurers charge patients the same premium regardless of their health condition. This was a huge change in the insurance market since it means that even people with serious health problems, like cancer survivors and people with heart conditions, can get insurance at the same price as anyone else of the same age.

Before the ACA, these people could expect to pay tens of thousands of dollars a year for insurance, if they could get it at all. As a practical matter, this meant that before the ACA most people really didn’t have insurance against serious health conditions. Often these conditions would force a worker to leave their job, which was generally the source of their insurance. Once they left their job, they would then be forced to buy insurance in the individual market where insurers could charge them a premium based on their health condition. The ACA fundamentally changed this situation, but apparently Brooks never noticed.

Note: I wanted to get folks the actual data (bonus points to anyone who can get this info to Brooks before he writes his next column on the topic). In 2012, before the key provisions of the ACA took effect, the Congressional Budget Office (CBO) projected that the uninsured population would fall to 32 million by 2015. In fact, it fell to 32 million by 2014, a year in which it was projected there would still be 38 million uninsured people. According to data from Gallup, the number of uninsured non-elderly fell to less than 28 million by the fourth quarter of 2015.

Read More Leer más Join the discussion Participa en la discusión

Seriously, the Post ran a major front page article in its Sunday business section telling us that “big business lost Washington.” The piece does acknowledge that business lobbies are still very effective in getting special deals for their industry, like favorable tax treatment for offshore profits and low-cost access to public lands for fossil fuel extraction, but it complains that business leaders are not openly setting the national agenda.

It’s not clear where exactly business leaders are seeing their needs go unmet. One of the most fundamental items on the national agenda is returning to full employment. Here the business community, lead by groups like the Peter Peterson funded organization “Fix the Debt,” along with the Washington Post, played a large role in pushing the government towards austerity in 2011. The result was sharply slower growth and much less job creation than would otherwise be the case.

This has been good news for many businesses, since the weak labor market led to an extraordinary leap in the profit share of national income. The cost to the rest of the country has been enormous, with millions of people needlessly being kept from working and tens of millions forced to accept much lower pay than would have been the case in a healthy labor market.

It’s more than a bit bizarre to complain that the business interests who were able to impose such enormous costs on the rest of society in order to advance their agenda have no power in Washington. Of course it is understandable that they would prefer the public not recognize their power.

Seriously, the Post ran a major front page article in its Sunday business section telling us that “big business lost Washington.” The piece does acknowledge that business lobbies are still very effective in getting special deals for their industry, like favorable tax treatment for offshore profits and low-cost access to public lands for fossil fuel extraction, but it complains that business leaders are not openly setting the national agenda.

It’s not clear where exactly business leaders are seeing their needs go unmet. One of the most fundamental items on the national agenda is returning to full employment. Here the business community, lead by groups like the Peter Peterson funded organization “Fix the Debt,” along with the Washington Post, played a large role in pushing the government towards austerity in 2011. The result was sharply slower growth and much less job creation than would otherwise be the case.

This has been good news for many businesses, since the weak labor market led to an extraordinary leap in the profit share of national income. The cost to the rest of the country has been enormous, with millions of people needlessly being kept from working and tens of millions forced to accept much lower pay than would have been the case in a healthy labor market.

It’s more than a bit bizarre to complain that the business interests who were able to impose such enormous costs on the rest of society in order to advance their agenda have no power in Washington. Of course it is understandable that they would prefer the public not recognize their power.

Read More Leer más Join the discussion Participa en la discusión

In pushing trade agreements it is fair to say anything, even if it has no relationship to the truth. Therefore it is not surprising to see Fareed Zakaria pushing the Trans-Pacific Partnership (TPP) by claiming that it will boost growth and attacking Bernie Sanders for opposing “trade policies that have lifted hundreds of millions of the world’s poorest people out of poverty.”

First, the impact on growth will be trivial. According to the International Trade Commission’s assessment, the TPP will boost the annual growth rate over the next fifteen years by less than 0.02 percentage points. And, this projection does not take account of the negative impact of the protectionist measures in the TPP, such as stronger and longer copyright and patent protection. These measures have the same impact on the protected items as tariffs of several thousand percent.

Zakaria then gets into straight out confusion when he tells readers that the TPP is a good deal for the United States because:

“Asian countries have made most of the concessions. And because their markets are more closed than the United States’, the deal’s net result will be to open them more.”

Actually in standard trade theory, most of the benefits from lowering tariffs accrue to the countries that lower them. In trade theory, it benefits their consumers. Overall, trade balances are not affected. This is why the very pro-TPP Peterson Institute shows that by far the largest gains to TPP accrue to Vietnam. It lowers its tariffs by the most under the terms of the deal.

In terms of the attack on Bernie Sanders for opposing the world’s poor, Zakaria is again confused. In the standard trade story, capital is supposed to flow from rich countries like the United States to poor countries in the developing world. That would mean rich countries run trade surpluses and poor countries run trade deficits. This allows poor countries to sustain consumption levels even as they build up their capital stock.

The world actually looked like this in the early and mid-1990s, especially for the fast-growing countries of East Asia. Malaysia, Vietnam, South Korea, and Thailand all had very large trade deficits even as their economies grew very rapidly. This reversed following the East Asian financial crisis in 1997. The terms imposed by the Clinton Treasury department through the I.M.F. forced these countries to start running large trade surpluses. As a result, the countries in the region had considerably slower growth in the subsequent two decades than they did from 1990 to 1997.

There is no reason, in principle, that these countries could have not continued to grow rapidly along the standard path of running trade deficits. It was a policy decision to force them to run trade surpluses. In other words, this is yet another gratuitous swipe at Bernie Sanders of the sort that readers have come to expect from the Washington Post.

At the end of the day, the TPP is about increasing the power of large corporations, who contribute heavily to political campaigns and offer former politicians high-paying lobbyist jobs, at the expense of the people of the region. Its proponents will say whatever they think is necessary to sell the pact, even if it has nothing to do with reality.

In pushing trade agreements it is fair to say anything, even if it has no relationship to the truth. Therefore it is not surprising to see Fareed Zakaria pushing the Trans-Pacific Partnership (TPP) by claiming that it will boost growth and attacking Bernie Sanders for opposing “trade policies that have lifted hundreds of millions of the world’s poorest people out of poverty.”

First, the impact on growth will be trivial. According to the International Trade Commission’s assessment, the TPP will boost the annual growth rate over the next fifteen years by less than 0.02 percentage points. And, this projection does not take account of the negative impact of the protectionist measures in the TPP, such as stronger and longer copyright and patent protection. These measures have the same impact on the protected items as tariffs of several thousand percent.

Zakaria then gets into straight out confusion when he tells readers that the TPP is a good deal for the United States because:

“Asian countries have made most of the concessions. And because their markets are more closed than the United States’, the deal’s net result will be to open them more.”

Actually in standard trade theory, most of the benefits from lowering tariffs accrue to the countries that lower them. In trade theory, it benefits their consumers. Overall, trade balances are not affected. This is why the very pro-TPP Peterson Institute shows that by far the largest gains to TPP accrue to Vietnam. It lowers its tariffs by the most under the terms of the deal.

In terms of the attack on Bernie Sanders for opposing the world’s poor, Zakaria is again confused. In the standard trade story, capital is supposed to flow from rich countries like the United States to poor countries in the developing world. That would mean rich countries run trade surpluses and poor countries run trade deficits. This allows poor countries to sustain consumption levels even as they build up their capital stock.

The world actually looked like this in the early and mid-1990s, especially for the fast-growing countries of East Asia. Malaysia, Vietnam, South Korea, and Thailand all had very large trade deficits even as their economies grew very rapidly. This reversed following the East Asian financial crisis in 1997. The terms imposed by the Clinton Treasury department through the I.M.F. forced these countries to start running large trade surpluses. As a result, the countries in the region had considerably slower growth in the subsequent two decades than they did from 1990 to 1997.

There is no reason, in principle, that these countries could have not continued to grow rapidly along the standard path of running trade deficits. It was a policy decision to force them to run trade surpluses. In other words, this is yet another gratuitous swipe at Bernie Sanders of the sort that readers have come to expect from the Washington Post.

At the end of the day, the TPP is about increasing the power of large corporations, who contribute heavily to political campaigns and offer former politicians high-paying lobbyist jobs, at the expense of the people of the region. Its proponents will say whatever they think is necessary to sell the pact, even if it has nothing to do with reality.

Read More Leer más Join the discussion Participa en la discusión

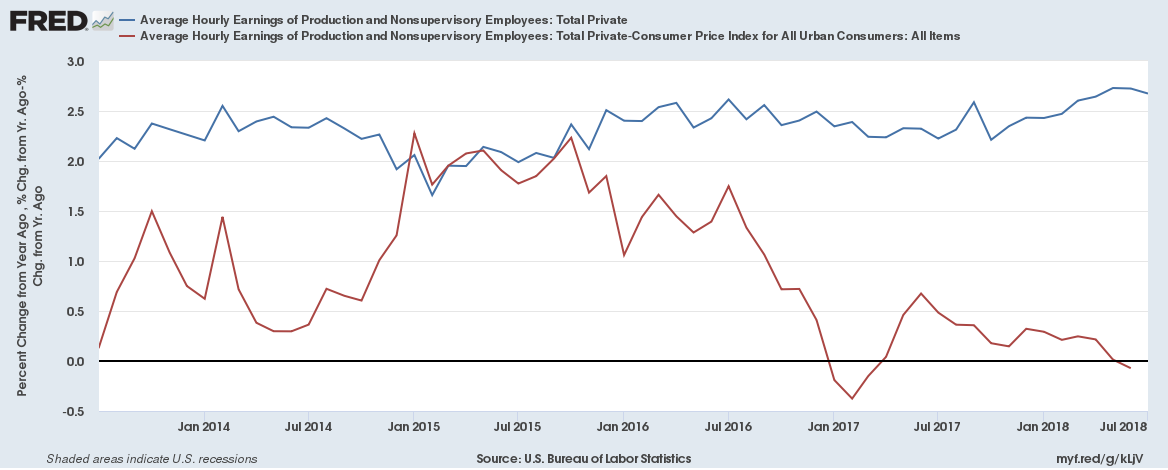

The NYT had a piece headlined “economists discuss differences that divide them,” which contrasted the views on the economy of Michael Gapen, chief United States economist at Barclays, and Stephanie Pomboy, founder of MacroMavens, an independent economics consulting firm. The first item where they presented contrasting views was on consumption patterns.

While Gapen thinks consumption will be strong the rest of the year and beyond, Pomboy is quoted as saying:

“After the bursting of the housing bubble and the Great Recession, there has been a generational shift away from spending toward saving among consumers. The great consumer credit boom of the 1980s, 1990s and 2000s is over. The savings rate has moved higher and this new impulse to save leads to a sluggish pace for growth.”

Actually, this is an area where we have data, so we don’t just have to speculate about the future. Consumption has actually been quite high in recent years as shown below.

Consumption is almost 69 percent of GDP. The only time it has been a higher share of GDP was 2011 and 2012 when the payroll tax holiday was in effect, raising disposable income. So Ms. Pomboy is clearly mistaken on this point. Consumers obviously are quite willing to spend, and in fact are spending a considerably larger share of their income than in the 1980s, 1990s, or 2000s, the exact opposite of what she claims in this piece.

The NYT had a piece headlined “economists discuss differences that divide them,” which contrasted the views on the economy of Michael Gapen, chief United States economist at Barclays, and Stephanie Pomboy, founder of MacroMavens, an independent economics consulting firm. The first item where they presented contrasting views was on consumption patterns.

While Gapen thinks consumption will be strong the rest of the year and beyond, Pomboy is quoted as saying:

“After the bursting of the housing bubble and the Great Recession, there has been a generational shift away from spending toward saving among consumers. The great consumer credit boom of the 1980s, 1990s and 2000s is over. The savings rate has moved higher and this new impulse to save leads to a sluggish pace for growth.”

Actually, this is an area where we have data, so we don’t just have to speculate about the future. Consumption has actually been quite high in recent years as shown below.

Consumption is almost 69 percent of GDP. The only time it has been a higher share of GDP was 2011 and 2012 when the payroll tax holiday was in effect, raising disposable income. So Ms. Pomboy is clearly mistaken on this point. Consumers obviously are quite willing to spend, and in fact are spending a considerably larger share of their income than in the 1980s, 1990s, or 2000s, the exact opposite of what she claims in this piece.

Read More Leer más Join the discussion Participa en la discusión

Thomas Friedman once again urged both major parties to compromise to get things done in his NYT column. He argues that compromise is the only way to get things done. To make his case he lists a number of issues where he argues compromise is necessary, leading with:

“How will we improve Obamacare?”

Friedman probably missed it (hard to get information about Washington politics at The New York Times), but the Republicans have made repeal of the Affordable Care Act (ACA) a sacred cause. They routinely demand the destruction of the ACA in their campaigns. They voted dozens of times to repeal the ACA and have celebrated any bad news that could be associated with the program. This is in addition to all the phony stories about the ACA killing jobs and forcing employers to switch to part-time workers that the Republicans have invented.

In this context, at this point doing anything to further Obamacare would amount to complete surrender on core Republican principles, not a compromise. But you would have to know something about Washington politics to be aware of this fact.

Thomas Friedman once again urged both major parties to compromise to get things done in his NYT column. He argues that compromise is the only way to get things done. To make his case he lists a number of issues where he argues compromise is necessary, leading with:

“How will we improve Obamacare?”

Friedman probably missed it (hard to get information about Washington politics at The New York Times), but the Republicans have made repeal of the Affordable Care Act (ACA) a sacred cause. They routinely demand the destruction of the ACA in their campaigns. They voted dozens of times to repeal the ACA and have celebrated any bad news that could be associated with the program. This is in addition to all the phony stories about the ACA killing jobs and forcing employers to switch to part-time workers that the Republicans have invented.

In this context, at this point doing anything to further Obamacare would amount to complete surrender on core Republican principles, not a compromise. But you would have to know something about Washington politics to be aware of this fact.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

That is what they warned, but they didn’t quite put it to readers that way. Instead the subhead warned that meeting President Obama’s goal of reducing emissions by 80 percent by 2050 would cost $5.28 trillion.

Yes folks, that sounds pretty scary. After all, $5.28 trillion over the next 34 years is bigger than a bread box, possibly much bigger.

Of course, it is unlikely that many of the WSJ’s readers have a clear idea of how big the economy will be over this 34-year period, so they are not likely to be in a good position to assess how much of a burden this would be. Since annual output will average more than $20 trillion a year (in 2016 dollars), this sum comes to about 0.9 percent of projected GDP. (This context is included near the bottom of the piece.) By comparison, the cost of the Iraq and Afghanistan wars at their peak was roughly 2.0 percent of GDP, implying that they imposed more than twice the burden on the economy as President Obama’s proposal to cut greenhouse gas emissions.

Another comparison that might be useful is the loss of potential GDP due to the austerity measures demanded by the Republican Congress and supported by many Democrats. In 2008, before the financial crisis, the Congressional Budget Office (CBO) projected that potential GDP in 2016 would 22.5 percent higher than in 2008. It now projects that potential GDP in 2016 is just 12.0 percent higher in 2016 than it was in 2008.

This decline in potential GDP is roughly ten times as large as the projected costs from meeting President Obama’s targets for greenhouse gas emissions. Even if just half of this cost was due to austerity (as opposed to a mistaken projection by CBO in 2008 or unavoidable costs of the crisis) then the cost of austerity would still be more than five times as large as the costs of meeting President Obama’s targets for greenhouse gas emissions.

And, as the piece notes, the estimates do not take account of any benefits from reduced damage to the environment. For example, we might have fewer destructive storms, flooding of coastal regions, and forest fires in drought afflicted regions.

It is also worth noting that the WSJ piece entirely focuses on the high-end estimate in the study, the low-end estimate is just over one quarter as large.

These are all reasons why readers might not take the conclusion of the piece very seriously:

“‘It’s a sad comment on the political debate. This will affect people’s children and grandchildren,’ Mr. Heal [the author of the study] said.”

That is what they warned, but they didn’t quite put it to readers that way. Instead the subhead warned that meeting President Obama’s goal of reducing emissions by 80 percent by 2050 would cost $5.28 trillion.

Yes folks, that sounds pretty scary. After all, $5.28 trillion over the next 34 years is bigger than a bread box, possibly much bigger.

Of course, it is unlikely that many of the WSJ’s readers have a clear idea of how big the economy will be over this 34-year period, so they are not likely to be in a good position to assess how much of a burden this would be. Since annual output will average more than $20 trillion a year (in 2016 dollars), this sum comes to about 0.9 percent of projected GDP. (This context is included near the bottom of the piece.) By comparison, the cost of the Iraq and Afghanistan wars at their peak was roughly 2.0 percent of GDP, implying that they imposed more than twice the burden on the economy as President Obama’s proposal to cut greenhouse gas emissions.

Another comparison that might be useful is the loss of potential GDP due to the austerity measures demanded by the Republican Congress and supported by many Democrats. In 2008, before the financial crisis, the Congressional Budget Office (CBO) projected that potential GDP in 2016 would 22.5 percent higher than in 2008. It now projects that potential GDP in 2016 is just 12.0 percent higher in 2016 than it was in 2008.

This decline in potential GDP is roughly ten times as large as the projected costs from meeting President Obama’s targets for greenhouse gas emissions. Even if just half of this cost was due to austerity (as opposed to a mistaken projection by CBO in 2008 or unavoidable costs of the crisis) then the cost of austerity would still be more than five times as large as the costs of meeting President Obama’s targets for greenhouse gas emissions.

And, as the piece notes, the estimates do not take account of any benefits from reduced damage to the environment. For example, we might have fewer destructive storms, flooding of coastal regions, and forest fires in drought afflicted regions.

It is also worth noting that the WSJ piece entirely focuses on the high-end estimate in the study, the low-end estimate is just over one quarter as large.

These are all reasons why readers might not take the conclusion of the piece very seriously:

“‘It’s a sad comment on the political debate. This will affect people’s children and grandchildren,’ Mr. Heal [the author of the study] said.”

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión