November 03, 2016

by Dean Baker and Lara Merling

It’s no secret that many folks, including many on the Fed, want to see higher interest rates. There are a variety of arguments put forward, including the story of huge but invisible bubbles that could burst and sink the economy just like the housing bubble did in 2008.

But the argument that deserves the most credibility is the conventional one that a low rate of unemployment is creating an overtight labor market. This leads to more wage growth, which will get passed along in more rapid inflation, which will soon force the Fed’s hand. At some point the Fed will have to raise rates to keep inflation from getting out of control or we will be back in an era of excessive inflation. By this logic it is better to get out front and do it now.

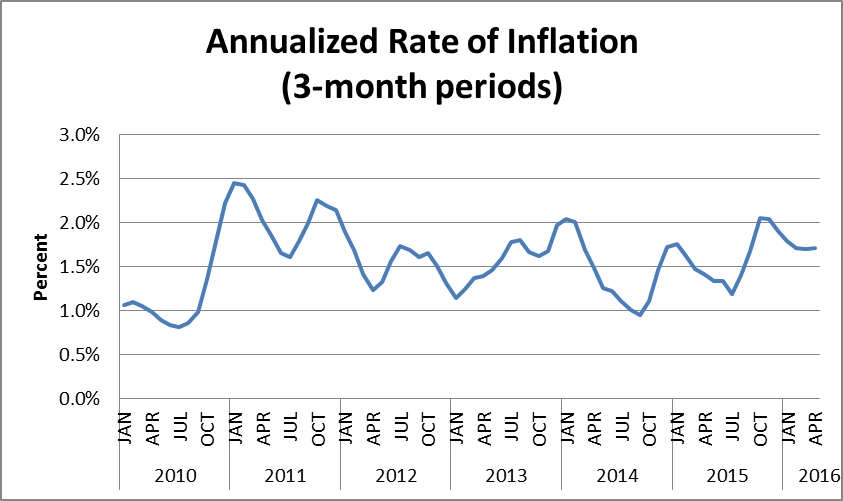

In this story, we should at least be seeing the beginnings of an acceleration of inflation, but we don’t. The figure below shows the core personal consumption expenditure deflator which provides the basis for the Fed’s 2.0 percent (average) inflation target.

Source: Bureau of Economic Analysis and author’s calculations.

The figure shows the annualized rate of inflation using average price levels from the most recent three-month period compared with average price levels from the prior three month period. It’s pretty hard to see any evidence of an upward trend in these data. The core rate had approached 2.5 percent in early 2011. It had minor fluctuations, but eventually bottomed out at 1.0 percent in the fall of 2014. It has moved modestly higher in the last two years, peaking at 2.0 percent at the end of 2015, but since then has crept down to 1.7 percent.

Of course, it is always possible that we will see the picture change and inflation will suddenly start to accelerate, but the point is that it has not yet done so. Furthermore, none of the standard models show that inflation suddenly jumps upward. If it does start to increase it would likely be a long and gradual process. For this reason, it is difficult to see the urgency in the drive to raise interest rates.

Comments