November 14, 2013

November 12, 2013, CAP and CEPR submit comments on Proposed Revisions to TANF Financial Data Collection and express general support for the proposed changes.

Office of Planning, Research and Evaluation

Administration for Children and Families

370 L’Enfant Promenade, SW

Washington, DC 20447

ATTN: AFC Reports Clearance Officer

RE: Center for American Progress/Center for Economic Policy and Research Joint Comments on Proposed Revisions to TANF Financial Data Collection

Dear Clearance Officer:

We would like to submit comments on TANF-ACF-IM-2013-03 (Proposed Revisions to TANF Financial Data Collection) and express our general support for the proposed changes. It is our belief that these changes will lead to improved information gathering and better-informed federal-level decision-making.

In Temporary Assistance for Needy Families: Potential Options to Improve Performance and Oversight (2013), the GAO “concluded that without more information that encompasses the full breadth of states’ uses of TANF funds, Congress will not be able to fully assess how funds are being used, including who is receiving services or what is being achieved.” We have shared in this concern. Congress should be fully aware of how states use TANF funds so that it can act accordingly, including by amending the TANF law to prevent or further encourage specific uses of funds. This knowledge could also impact Congressional decision-making outside of the context of TANF—for example, having a full sense of how much TANF is contributing to child welfare reunification could impact other funding decisions related to those services.

This knowledge is similarly useful to taxpayers who should know how their money is being invested. They would then have the option of expressing their support or displeasure to their representatives in Congress and to appropriate state officials.

Additionally, the proposed changes will go a long way in helping HHS, researchers, and other interested parties identify best practices. Elevated spending in certain categories flags that states may be engaging in new and/or significant programming that is worthy of further exploration.

Along with our general support for the proposed changes, we would like to offer a few specific comments recommending amendments to the current document that are consistent with the goal of improving the information available on TANF financial expenditures.

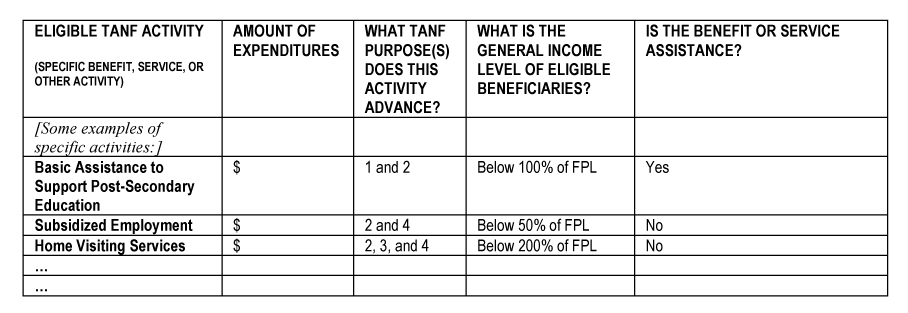

Recommendation 1:HHS should adopt a more descriptive and precise system for state reporting of TANF expenditures, to the extent allowable under current federal law and without imposing an undue burden on states. Consideration should be given to developing a reporting matrix, similar to that utilized for CDBG reporting, that clearly distinguishes between specific eligible TANF activities (used here to designate benefits, services, and other things that can use TANF funds for) and TANF purposes.[1] The level of detail for TANF-eligible-activity categories should be more granular than in the proposed ACF-196. As in CDBG, it also would be helpful for states to provide information on the general income range of beneficiaries receiving the benefit or service.

Here is a very schematic example of what the kind of approach we suggest might look like:

Rationale: While a considerable improvement on the current ACF-196, the expenditure categories and subcategories in proposed ACF-196 remain quite broad. Adopting a more descriptive and granular reporting matrix would further the goal of gaining greater insight into how states spend funds and better informing policymaking while placing little additional reporting burden on states. A matrix approach would also recognize that specific eligible TANF activities can serve multiple TANF purposes. For example, “basic assistance” is both a TANF purpose and an eligible TANF activity. However, when considered as an activity, it can serve multiple TANF purposes—for example, providing basic assistance to 2-parent families can further the TANF purpose of encouraging the formation and maintenance of two-parent families. Similarly, if basic assistance is provided to support post-secondary education (in effect, the assistance functions as supplemental student financial aid) it furthers the TANF purpose of ending the dependence of needy parents on government benefits.

Recommendation 2:The following subcategories should be added to the “Basic Assistance” category: a) Basic Assistance provided as Job Search and Unemployment Assistance; b) Basic Assistance provided as Disability/Incapacity Assistance; c) Basic Assistance provided as Supplemental Student Financial Aid; d) Basic Assistance provided as Workers Assistance; and e) Basic Assistance provided for Other Reasons.

Rationale: Although often thought of generically as “welfare”, the basic assistance provided under the Temporary Assistance program serves multiple functions, and often functions as a supplement to or extension of other programs that also promote economic opportunity and security. The public’s and policymakers’ understanding of basic assistance would be greatly enhanced if these different functions were made more transparent.

Recommendation 3:The sub-category Non-Transportation Work Supports (line 10.c) should be made a separated out/made into a main category with the following two subcategories: a) Goods Provided to Individuals to Help them Obtain or Maintain Employment; and b) Work Support Allowances and Bonus/Incentive Payments to Individuals.

Rationale: These two types of TANF-eligible-activities are quite distinct. Requiring reporting by subcategories would further the goal of gaining greater insight into how states spend funds and better informing policymaking while little, if any, additional reporting burden on states.

Recommendation 4:States should be asked to disclose how much of their funding goes to specific categories of subgrantees, including other non-TANF government agencies, non-profits, and for-profit entities.

Rationale: This addition would help track program trends that should inform administrative and Congressional decision-making. It would contribute to existing knowledge about the degree to which TANF programs are still providing direct services. This has implications for the types of federal-level technical assistance that states and localities might find useful. It may also inform future legislative activity. And finally, knowledge about the deliverers of social services (non-profit, for-profit, other governmental agencies) helps to provide researchers with a starting point into inquiries about which types of entities are best suited to provide specific services.

These comments and recommendations are being submitted jointly by the Center for American Progress and the Center for Economic and Policy Research. We appreciate your consideration. Should you have any additional questions, please feel free to contact us.

Sincerely,

| Shawn Fremstad Senior Research Associate Center for Economic and Policy Research 202-257-3786 [email protected] |

|

| Joy Moses Senior Policy Analyst Center for American Progress 202-741-6373 [email protected] |

|

1 See IDIS Matrix—CDGB Eligibility Activity Codes and National Objectives (accessed on November 12, 2013).